Download

1 / 15

150 likes | 274 Views

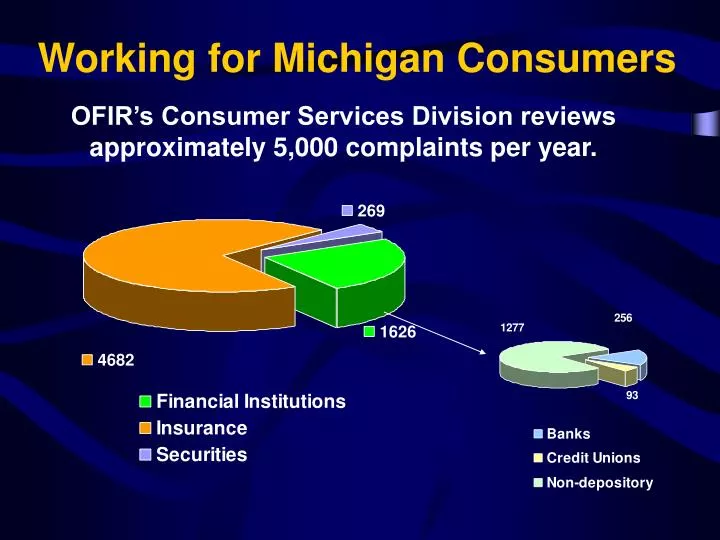

Working for Michigan Consumers. OFIR’s Consumer Services Division reviews approximately 5,000 complaints per year. . OFIR provides consumer assistance, conducts investigations and takes enforcement actions for the benefit of Michigan consumers.

E N D

Working for Michigan Consumers OFIR’s Consumer Services Division reviews approximately 5,000 complaints per year.

OFIR provides consumer assistance, conducts investigations and takes enforcement actions for the benefit of Michigan consumers. Last year OFIR staff helped consumers recover $8,573,297! OFIR is working for you!

PURCHASING OR REFINANCING A HOME – WHAT CAN OFIR DO TO HELP? • Call OFIR or visit OFIR’ s website at www.mi.gov/ofir to see if: • The lender and its agents are licensed • The lender is in good standing • The lender is not the subject of disciplinary actions

Top Mortgage Complaints • Fraud • Mortgage Processing Delays • Foreclosure • Misrepresentation in Terms of the Loan or Fees Charged • Fees charged (excessive or not refunded) • Escrow Account Issues • Payment Issues • Predatory Practices • Loans Not Funded at Closing • Inflated Appraisal Value • Pre-payment Penalty Charged

HAVING PROBLEMS WITH A MORTGAGE LENDER, BROKER OR SERVICER – WHAT CAN OFIR DO? • First contact the lender in writing and try to resolve the problem • If not able to reach a resolution, then file a written complaint with OFIR and submit it with all necessary documentation. • OFIR will contact the lender and request a response within 21 days. • OFIR will try to have the lender to voluntarily correct a situation when warranted. • If violations of the laws are allegedly found, the matter will be referred to enforcement for appropriate administrative or criminal action.

HAS YOR MORTGAGE PAYMENT INCREASED BECAUSE YOU HAVE AN ADJUSTABLE RATE MORTGAGE (ARM)? • You may want to convert your mortgage to a fixed-rate product. Contact your Lender. • Before you do so determine that the payment will be affordable to you for the duration of the loan.

LATE IN YOUR MORTGAGE PAYMENTS – BUT NOT YET IN FORECLOSURE - WHAT CAN OFIR DO? • First contact the lender in writing to inform them of the situation and how you plan to correct it • File a complaint as an appeal to OFIR for assistance. Be sure to tell us the circumstances as to why your payments are late. • If late because of ARM, OFIR will act as link between you and the lender to see if you qualify for options such as refinancing to a fixed rate, permanent loan modification etc. . . • If late because of short term loss of employment/income, or short term medical condition OFIR will see if the lender will defer the late payments or grant a forbearance, etc. . .

LATE IN YOUR MORTGAGE PAYMENTS – BUT NOT YET IN FORECLOSURE - WHAT CAN OFIR DO? (Cont’d 1) • Review your options in “Facing Foreclosure…” from our website www.mi.gov/ofir • Options include: Forbearance agreement (repayment agreement), loan modification, payment deferral, loan restructuring – these options can be both temporary and permanent. • Determine which option best suits your situation. • Submit a written complaint to OFIR explaining the circumstances and the resolution that you seek.

LATE IN YOUR MORTGAGE PAYMENTS – BUT NOT YET IN FORECLOSURE - WHAT CAN OFIR DO? (Cont’d 2) • OFIR cannot write the complaint on your behalf. • You must, therefore, write the complaint as an appeal to OFIR for assistance with reinstatement of mortgage. • OFIR will then contact the mortgage lender or mortgage servicer to determine what options that lender or servicer is willing to grant, given your circumstances.

MISSED A MORTGAGE PAYMENT… WHAT’S NEXT? • Contact your lender ASAP and explain to them why your payment will be late. Follow-up with a letter. • Respond to all mail from your lender. • Follow options that the lender gives you.

FACING FORECLOSURE? WHAT CAN OFIR DO? • OFIR will try to be a link between you and the lender but YOU need to do the following: • 1. Open the lines of Communication. Talk to your lender! • 2. Be truthful and explain your situation • 3. Your lender wants you to stay in your home and continue making the payments

FACING FORECLOSURE? WHAT CAN OFIR DO? (Cont’d) . OFIR will try to have the lender assist you in keeping your home. . Keep in mind, however, that any decision reached by the lender will depend on their determination of your willingness and your ability to pay and the willingness of the investors in your mortgage to reach a solution other than foreclosure

THE FORECLOSURE PROCESS IN MICHIGAN • If you are late in your payment you face foreclosure. Generally, a lender will not start foreclosure process until you are at least 90 days late. • Once a week and for the next 4 weeks (30days) the lender will publish a notice in a local newspaper. During that time you can cure the default by paying all past due payments – sell the house – make a “short sale”. • Sheriff’s sale is handled by the court and the house is sold to the highest bidder usually the lender. From that time on you may occupy the house for up to 6 months and make no payments – redeem the house by paying the full amount of the sheriff’s sale – sell the house for at least the amount of the sheriff’s sale.

Don’t fall victim to a sophisticated financial scam carried out by a skillful con artist. If something doesn’t sound right or if it sounds too good to be true, call OFIR. DOUBT means DON’T until you ASK OFIR! CONSUMERS BEWARE!!

Connecting with OFIR • By toll-free phone 1-877-999-6442 • Lansing local phone 1-517-373-0220 • On the Internet www.michigan.gov/ofir • In person • By mail Ottawa Building, 3rd floor 611 W. Ottawa St. Lansing, MI 48933 OFIR PO Box 30220 Lansing, MI 48909-7720