Download

1 / 35

360 likes | 533 Views

What Is A Traditional IRA?. A “Traditional IRA” is a tax-deferred savings vehicle A limited tax-deductible contribution may be made up to $5,000 (2009-2011) Additional catch-up contributions of $1,000 (2006 forward) are permitted for individuals over age 50. What Is A Traditional IRA?.

E N D

What Is A Traditional IRA? • A “Traditional IRA” is a tax-deferred savings vehicle • A limited tax-deductible contribution may be made up to $5,000 (2009-2011) • Additional catch-up contributions of $1,000 (2006 forward) are permitted for individuals over age 50

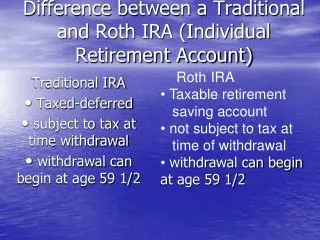

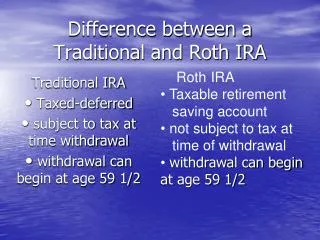

What Is A Traditional IRA? • An individual or spouse actively participating in a qualified plan or tax-sheltered annuity: • May make an IRA contribution up to the lesser of the $5,000 dollar limit (in 2009-2011, including the total of all IRA contributions combined) or 100% of compensation • The amount a taxpayer can deduct is determined based on AGI and filing status • Mandatory distributions are required beginning at age 70½ • Penalties, in addition to income taxes, are imposed for early nonqualified withdrawals

What Are The AGI Threshold Contribution Phase-Out Limits? AGI Threshold Tax Year Single Joint Separate 2010 $56,000 $89,000 $0 2011 $56,000 $90,000 $0 Note: For non-active participants with an active spouse, the deduction begins to phase out when AGI is > $90,000 (2011) For a taxpayer who exceeds the threshold, the maximum deduction is reduced by the following formula: Maximum annual contribution x AGI – AGI Threshold $10,000

Example Traditional IRA • Jill participates in a qualified plan and her husband, Jack does not participate in his employer’s plan • They file a joint return in 2011 showing AGI of $125,000 • Jack can make a deductible contribution to his IRA of $5,000 (Couple’s AGI is under $169,000) • Same facts, but Jill and Jack’s AGI is $200,000 • Neither Jack nor Jill can make a deductible contribution, since their AGI exceeds $179,000

Example Traditional IRA (cont’d) • Note: An individual may make a deductible contribution to a spousal IRA for a spouse with less taxable compensation than the individual • In 2011, $5,000 could be contributed to one IRA and another $5,000 to a spousal IRA

What Is A Rollover? • Individuals receiving certain distributions from a qualified plan (pension, profit-sharing, stock bonus or annuity plan) or a tax-deferred annuity are allowed to “roll over” the distribution within 60 days to an IRA without incurring income tax on the distribution • No rollover is permitted for benefits attributable to nondeductible employee contributions made by the employee to the qualified plan prior to 2002

What Is A Rollover? • Taxable distributions from a qualified retirement plan, TSA, or Section 457 governmental plan can be rolled over, without incurring income tax, to an IRA or any of the above listed plans • A mandatory withholding of 20% applies if the participant receives a distribution instead of electing a direct (trustee-to-trustee) transfer • A spouse of a deceased IRA holder may roll over a distribution (received after the spouse’s death) to an IRA

What Is A Roth IRA? • Annual contributions may be made up to the lesser of $5,000 (2009-2011) or 100% of compensation • indexed for inflation in $500 increments for years after 2010 • Catch-up contributions of $1,000 (2011) are permitted for individuals over age 50 • Contributions are not deductible, but withdrawals may be entirely income tax free • Contributions may be made after age 70½

What Is A Roth IRA? • If AGI exceeds certain limits, a contribution to a Roth IRA cannot be made for that year • Single phase-out limit $107,000 - $122,000 • Married filing joint limit $169,000 - $179,000 • Married filing separate limit $0 - $10,000 • Rules on allowable Roth IRA contributions apply regardless of taxpayer’s active participation in a qualified plan • Distributions are not required to begin until after death • For certain clients a rollover (“conversion”) of a Traditional IRA to a Roth IRA may be desirable

What Is An ESA? • The Coverdell Education Savings Account or Education IRA permits a non-deductible contribution of up to $2,000 (2011) to pay qualified education expenses • Qualified education expenses now include both elementary and secondary school expenses • ESA contributions must be designated as such and made in cash, on or before the beneficiary reaches age 18 • Contributions can be made up until April 15 of the following year, by the due date for the filing of the contributor’s income tax return

What Is An ESA? • There is an excise tax for excess contributions • Income tax will be imposed on that portion of distributions exceeding qualified education expenses • There is a 10% premature distribution penalty • AGI phase-out limits on contributions • Single contributor $95,000 - $110,000 • Married Filing Joint $190,000 - $220,000

When Is Use Of A Traditional IRA Appropriate? Situation 1: • When a married client or their spouse • is covered by a qualified plan, and • does not make in excess of the AGI phase-out limits, and • makes income in excess of what is needed to maintain their current standard of living • It is preferable to make non-tax deductible contributions to a Roth rather than a Traditional IRA

When Is Use Of A Traditional IRA Appropriate? Situation 2: • Where neither the client nor spouse is covered under a qualified plan, but both work Situation 3: • Where the client • Is not covered under a plan • Has earned income • Is married, and • Spouse has no income from employment

When Is Use Of A Traditional IRA Appropriate? Situation 4: • Client is an employer without a qualified plan and would like to establish a plan covering only him or herself

When Is Use Of A Rollover IRA Appropriate? • An individual has received a distribution from a • Qualified plan • TSA, or • Section 457 government plan, and • Seeks to avoid current taxation on all or a part of the distribution

When Is Use Of A Roth IRA Appropriate? • Where the client would not otherwise qualify for a deduction for contributing to a Traditional IRA • Where a client anticipates a reduced need to access IRA funds during retirement and wants funds to continue to grow tax-free • Client anticipates being in a high marginal tax bracket following retirement

What Are The Requirements? • An individual is permitted to set aside retirement savings in a • Variable premium annuity contract • Fixed rate annuity contract, or • A trusteed or custodial account with a bank, credit union, savings and loan, brokerage firm, or other financial institution • An individual may split total contributions into more than one IRA • 3 parties can make contributions to a Traditional IRA • Employee • Employee’s employer • Employee’s union

What Are The Requirements? • Anyone can contribute to an ESA • Annual contributions must be made in cash • Contributions of other property are only permissible in the case of rollovers • Plan must be established and contributions made • Within the taxable year for which a deduction is allowed, or • Before the due date for filing the individual’s tax returns for that taxable year (by April 15th of the following year for most taxpayers)

What Are The Requirements? • Traditional IRAs must begin to pay a participant’s benefit by April 1st of the year following the year in which the participant turns 70½ • RBD – required beginning date • ESA’s must be distributed within 30 days after the date on which the designated beneficiary attains age 30 • Earnings on such distributed balances may be includable in income and subject to the 10% penalty tax • Any amount remaining in the ESA at the end of the 30-day period will be deemed to be distributed

What Are The Requirements? • Alternatives for a Traditional IRA if the owner dies before beginning distributions: • Payments are made over the life expectancy of the designated beneficiary, or • If there is no designated beneficiary, payments must be paid out within five years of the IRA owner’s death • If the designated beneficiary is the IRA owner’s spouse, the spouse may • roll over the balance to the spouse’s own IRA, or • elect to treat the decedent’s IRA as the spouse’s own, or • take distributions over the spouse’s life expectancy beginning the later of • The end of the calendar year immediately following the calendar year in which the owner died, or • The end of the calendar year in which the owner would have attained age 70½

What Are The Requirements? • Alternatives for a Traditional IRA if the owner dies on or after the required beginning date: • Payments are made over the life expectancy of the designated beneficiary, or • If there is no designated beneficiary, payments are made over the remaining life expectancy of the IRA owner immediately before death • If the sole designated beneficiary is the IRA owner’s spouse, the spouse may • roll over the balance to the spouse’s own IRA, or • elect to treat the decedent’s IRA as the spouse’s own, or • take distributions over the spouse’s remaining life expectancy beginning with the calendar year immediately following the calendar year in which the owner died

What Are The Requirements? • Roth IRAs generally follow the same rules as Traditional IRAs for owners dying before the required beginning date • Roth IRAs do not have a lifetime required beginning date • ESAs must be distributed within 30 days of the death of the beneficiary • If the ESA is distributed to the designated beneficiary’s surviving spouse or a family member, it will be treated as if the spouse or family member is the designated beneficiary as long as they are under the age of 30 • Any balance remaining in the ESA at the end of the 30-day period following the designated beneficiary’s death will be deemed distributed

How Is It Done? • Banks and insurance companies provide prototype plans • IRS provides prototype trusteed and custodial plans • Once an IRA is established, contributions need to be made

How Is It Done? Examples of tax savings: • Individual in a 15% tax bracket would save $750 per year with a $5,000 annual deductible contribution • A partner in a partnership who did not wish to include other employees in a plan could save $1,250 per year in taxes by making a $5,000 annual deductible IRA contribution, assuming a 25% tax bracket

Tax Implications • Money contributed to a Traditional IRA is currently deductible from gross income up to the specified limits • Earnings accumulate on a tax-deferred basis • Generally, individual needs to be 59½ to receive distributions without a 10% premature distribution penalty (unless an exception to the penalty applies)

Tax Implications • Exceptions to the 10% penalty include: • Withdrawals due to death or disability • Withdrawals in the form of a series of substantially equal periodic payments • Distributions up to $10,000 for a “qualified first-time homebuyer distribution” • Withdrawals used to pay qualified higher education expenses

Tax Implications • Distributions from a Traditional IRA are taxed to the client at ordinary income tax rates • A “qualified distribution” from a Roth IRA is not taxable if distribution is made: • after the five year waiting period • in the event of death or disability • for first-time homebuyer expenses • at or after age 59½

Tax Implications • Non-qualified distributions from a Roth are includable in income only to the extent that the withdrawal (plus earlier withdrawals) exceeds the total of contributions made to the Roth IRA • There is no required beginning distribution date at age 70½ for a Roth IRA • However, traditional IRA minimum distribution rules apply to the beneficiary of a Roth following the death of the IRA owner

Issues In Community Property States • Division of an interest in an IRA should be less difficult than division of a qualified plan, since all benefits in an IRA are vested and nonforfeitable • ERISA provides that the transfer of the spouse’s entire interest in an IRA to a former spouse under a divorce decree is not a taxable distribution Caution: Transfers of partial interests may cause the “premature distribution” tax and ordinary income tax to be imposed

Active Participant defined Individual is an active participant if covered by a(n): • qualified pension, profit sharing or stock bonus plan, • qualified annuity plan • SEP • government sponsored plan, or • employee only contributory plan exempt from tax under IRC Section 501(c)(18)

Simplified Employee Pensions • IRA-based plan established by an employer that receives contributions by employer based on predetermined formula • Contribution limit is lesser of 25% of compensation or $49,000 (in 2011) • Compensation limit is $245,000 (2011) • Elective deferrals to preexisting plans (SARSEPs) still allowed

Simplified Employee Pensions • Employer must contribute for every employee 21 or older who earned $550 or more (2011) in 3 of the last 5 years • May not discriminate in favor of HCEs • Limited integration is permitted • 100% vesting for all employees required • Plan must be in writing, must spell out how contributions will be allocated • SEP participants are active participants for IRA deduction purposes

SIMPLE IRAs • Available to employers with 100 or fewer employees earning $5,000 or less • May not sponsor another plan • Salary deferrals up to $11,500 permitted in 2011 • Catch-up contributions permitted up to $2,500 in 2011

SIMPLE IRAs Contribution formula requirement: must be one of following: • Match contribution: dollar for dollar up to 3% of compensation, or • Nonelective contribution: 2% of compensation for all eligible employees earning at least $5,000