Download

1 / 5

50 likes | 186 Views

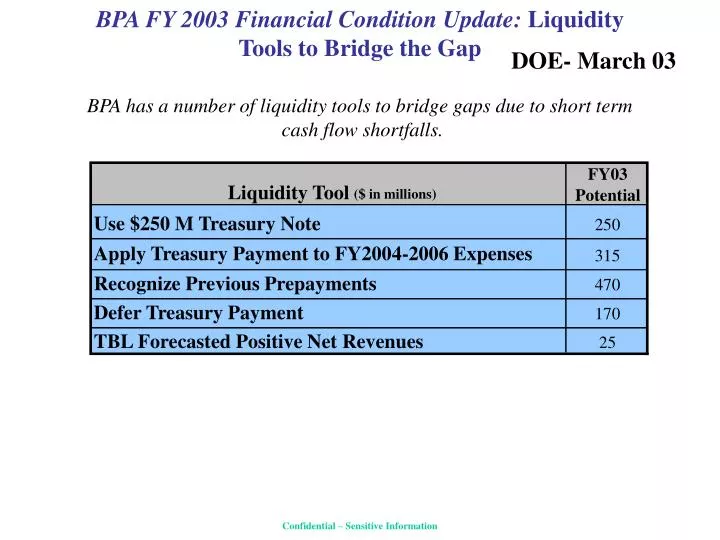

BPA FY 2003 Financial Condition Update: Liquidity Tools to Bridge the Gap. FY03 . Liquidity Tool . Potential. ($ in millions). Use $250 M Treasury Note. 250. Apply Treasury Payment to FY2004-2006 Expenses. 315. Recognize Previous Prepayments. 470. Defer Treasury Payment. 170.

E N D

BPA FY 2003 Financial Condition Update: Liquidity Tools to Bridge the Gap FY03 Liquidity Tool Potential ($ in millions) Use $250 M Treasury Note 250 Apply Treasury Payment to FY2004-2006 Expenses 315 Recognize Previous Prepayments 470 Defer Treasury Payment 170 TBL Forecasted Positive Net Revenues 25 DOE- March 03 BPA has a number of liquidity tools to bridge gaps due to short term cash flow shortfalls. Confidential – Sensitive Information

Current Issues With Treasury DOE-Dec.02 • Roger Kodat and Paula Farrell are tentatively planning a visit to BPA in January • Advance Amortization Recognition: BPA continues its discussions with Treasury, focused on conditions which cause 1% interest penalty to be imposed. The Transmission Act says, in part, “. . .if the Administrator fails to repay by the end of any fiscal year all of the amounts projected immediately prior to such year to be repaid to the Treasury by the end of such year . . .if such failure is due to reasons other than (A) a decrease in power sale revenues due to fluctuating streamflows or (B) other reasons beyond the control of the Administrator, the Secretary of the Treasury may increase the interest rate applicable to the outstanding bonds issued by the Administrator during such fiscal year. . . . The Secretary of the Treasury shall take into account amounts that the Administrator has repaid in advance of any repayment criteria in determining whether to increase such rate.”(See Appendix for complete language.) Treasury is discussing the possibility oftheir attorneys giving us some general guidelines on the 1% penalty in terms of what documentation they would expect from us if we missed a payment, what things they would consider beyond the control of the Administrator, etc.

Advance Amortization Recognition DOE-Sep.02 Language from BPA FY 2002 Budget, page 8 – "In recent years, BPA has made amortization payments in excess of those scheduled in its FERC-approved rate filings, resulting in a balance of advance repayment., This balance will allow BPA to reduce amortization below scheduled amounts if, in a future year, decreased revenues or increased cost cause a serious cash flow deficit. The Advance Amortization Recognition balance will assist BPA on a cumulative basis to remain current or ahead or current on its repayment. The balance will allow BPA to use overpayments in prior years to offset reduced future payments. This recognizes an underlying concept behind the power marketing administrations' repayment policy and BPA's organic legislation--that hydro systems are dependent on extremely variable stream flows for revenues, with the potential for more than the planned annual amortization payment in good water years and less in bad water years."

Accelerated Repayment Recognition Treasury-July.02 • Today’s Goal • To open discussion among the agencies in order to avoid confusion later regarding the concept, purposes and mechanics of accelerated repayment recognition balances. • The Concept • BPA would create an accelerated repayment recognition balance when Federal appropriations or bonds are repaid ahead of the repayment schedule established in rate filings, e.g. BPA makes more principal payments in a year than scheduled when rates are set. BPA would use this acceleration balance when it lacks the revenues and financial reserves needed to make its Treasury principal payment as a result of risk factors beyond its control (e.g. high market prices, poor hydro conditions, increased costs). Recognition of this balance regards BPA as having remained current on its status of repayment, since on a cummulative basis repayment is on or ahead of schedule • The recognition would • allow BPA to exercise the repayment flexibility in its statutes and policy, while keeping BPA’s cumulative repayment current or ahead of schedule • allow BPA to exercise prudent debt management by avoiding holding large cash balances when results are good, while creating an additional financial “reserve” that could be utilized to delay amortization payments in a serious cashflow deficit

Accelerated Repayment Recognition -Potential Design Treasury-July.02 • HowAcceleration BalanceAccrues • BPA would receive recognition for any accelerated repayment of Federal debt: when BPA repays more principal in a year than was scheduled in its FERC-approved rate filings (timely repayment of the Federal investment is a key criterion to be demonstrated for rate approval) • The recognition would not reduce BPA’s total repayment obligations (not debt relief or debt write-down) • The acceleration balance would not accrue when BPA retires debt associated with the book value of sold assets or prepaid revenues (e.g., customer delivery facility sales, Intertie capacity ownership, etc.) • Decisions to accelerate repayment would remain at BPA’s discretion Use of the Acceleration Balance • The acceleration balance would be accessed when all or part of an annual amortization payment otherwise could not be made • Access of the acceleration balance would only pertain to the principal portion of BPA’s Treasury payments • Potential Sources of Funds for Repayment Acceleration • Debt management program in conjunction with Energy Northwest • Designed to reduce long-term interest expense and replenish Treasury borrowing authority with no net increase in BPA’s costs through at least FY 2012 • BPA is committed to applying the proceeds from this program to accelerate repayment of higher-cost Federal bonds and appropriations • Depending on interest rates and other factors when transactions under the program are completed, proceeds could amount to as much as $500 million by 2012 • From reserves in excess of BPA’s TPP goals (88 percent over 5-year period) • Status of Repayment • As of the end of FY 2000, BPA has accelerated $100.2 million, largely using proceeds from ENW debt transactions (occurring in FYs 1998-2000)