Download

1 / 36

360 likes | 381 Views

Lecture 6: Market Structures (Monopolistic Competition and Oligopoly). Mon o polis t i c Co m peti t ion. Monopolis t i c co m peti t io n i s a model i n whi c h ma n y fi r ms sell similar but not identica l p r oducts. Example s : books bottled w ater clothi n g fast f ood night clubs.

E N D

Lecture 6: Market Structures (Monopolistic Competition and Oligopoly)

MonopolisticCompetition Monopolisticcompetitionis amodelin which many firmssellsimilarbutnot identical products. • Examples: • books • bottledwater • clothing • fastfood • night clubs • Characteristics: • Many sellers • Productdifferentiation • Freeentry andexit • Non-price competition

MonopolisticCompetition Short-run equilibrium of the firmunder monopolistic competition P MC • Short run: • Under monopolistic competition, firm behaviour is very similar to monopoly • Firms profit maximise, MC=MR • If P > ATC, they make an economic profit ATC P Economic Profit ATC D MR Q Q

MonopolisticCompetition 1.Ifprofitsintheshortrun: Newfirmsentermarket, P MC taking some demand away from existing firms, prices and profits fall ATC P Economic Profit ATC D MR Q Q

MonopolisticCompetition 1. If profits in the short run: New firms enter market, taking some demand away from existing firms, prices and profits fall Long run: entry drives economic profit to zero P MC ATC P P’=ATC’ 2.If losses in the short run: Some firms exit the market, remaining firms enjoy higher demand and prices Long run: exit drives economic profit to zero ATC D D’ MR’ Q’ Q Q

Long-run equilibrium of the firmunder monopolistic competition LRMC LRAC ARL=DL MRL £ New firms entering the industry reduce demand for each individual firm. Price falls to PL. PL O QL Q

Monopolistic CompetitionandWelfare • Monopolistically competitive markets do not have all the desirable welfare properties of perfectly competitive markets; • Because P > MC, the market quantity is below the socially efficient quantity; • Yet, not easy for policymakers to fix this problem: Firms earn zero profits, so cannot require them to reduce prices; • The inefficiencies of monopolistic competition are subtle and hard to measure. No easy way for policymakers to improve the market outcome

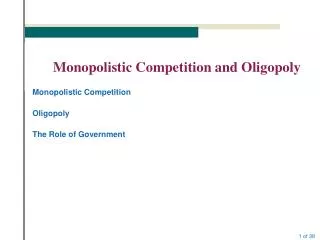

AdvertisingandBrandNames • Inmonopolisticallycompetitiveindustries,productdifferentiationandmark-uppricingleadnaturallytotheuseofadvertisingandbrandnames • Economistsdisagreeaboutthesocialvalueofadvertisingandbrandnames

AdvertisingandBrandNames • Critics believe: • Society is wasting resources it devotes to advertising; • Firms advertise to manipulate people’s tastes; • Advertising impedes competition – it creates the perception that products are more differentiated than they really are, allowing higher mark-ups. Defendersbelieve: • It provides useful information to buyers; • Informed buyers can more easily find and exploit price differences; • Thus, advertising promotes competition and reduces market power.

Long run equilibrium of the firm under perfect and monopolistic competition P2 DLunder perfect competition £ Higher price and lower output (excess capacity) under monopolistic competition LRAC P1 DLunder monopolistic competition O Q1 Q2 Q

Oligopoly Key features of oligopoly barriers to entry interdependence of firms Competition versus collusion Collusive oligopoly: cartels equilibrium of the industry allocating and enforcing quotas

Profit-maximising Cartel Industry MC £ Industry profit maximised at Q1 and P1 P1 Members must agree to restrict total output to Q1. Industry D = AR Industry MR Q1 O Q

QIn which of the following circumstances would a cartel be most likely to work? The coffee market, where the product is standardised and there are many coffee growers. The market for copper, where there are very few producers and the product is standardised. The car industry, where there are few producers but there is great product differentiation. The fast-food market, where there are many producers but the demand for fast food is inelastic.

Oligopoly Tacit collusion price leadership: dominant firm

AR = Dmarket AR = Dleader MRleader Price Leader Aiming To Maximise Profits For a Given Market Share £ Assume constant market share for leader O Q

l t PL QL QT Price Leader Aiming To Maximise Profits For a Given Market Share £ MC AR = Dmarket Leader maximises profit at QLand thus sets price of PL. AR = Dleader MRleader O Q

Oligopoly Factors favouring collusion few firms open with each other similar production methods and average costs similar products dominant firm significant entry barriers stable market no government measures to curb collusion

Oligopoly The breakdown of collusion factors to consider in deciding whether to break an agreement how likely are rivals to retaliate? who would win a price war? importance of considering rivals’ reactions

Oligopoly Non-collusive oligopoly: assumptions about rivals’ behaviour rivals produce fixed quantity: Cournot model

The Cournot model of duopoly: Firm A’s demand Firm A believes that firm B will produce QB1. DA1 DM QB1 Costs and revenue O Quantity

Oligopoly Non-collusive oligopoly: assumptions about rivals’ behaviour rivals produce fixed quantity: Cournot model firms choose best output for remainder of the market

Cournot model: Firm A’s profit-maximising position MCA PA1 QA1 Firm A’s profit-maximising output and price are QA1 and PA. Costs and revenue DA1 DM MRA1 O QB1 Quantity

The Cournot model of duopoly Firm A’s reaction function for each assumed output of B RA x QB1 QA1 £ MCA Firm B’s output PA1 DM DA1 MRA1 O QA1 O QB1 Firm A’s output Quantity (b) The two firms’ reaction functions (a) Firm A’s profit-maximising position

The Cournot model of duopoly e QBe RB QAe Equilibrium at point e, where the two reaction functions cross £ RA MCA Firm B’s output PA1 x QB1 DM DA1 MRA1 QA1 O QA1 O QB1 Firm A’s output Quantity (b) The two firms’ reaction functions (a) Firm A’s profit-maximising position

Oligopoly Non-collusive oligopoly: assumptions about rivals’ behaviour rivals produce fixed quantity: Cournot model firms choose best output for remainder of the market • profit will be less than under a cartel • but more than under perfect competition • rivals set a particular price: Bertrand model • the firm will undercut the rival • this will probably trigger a price war until all supernormal profits are eliminated

Oligopoly • Oligopoly: a market structure in which only a few sellers offer similar or identical products • Strategic behaviour in oligopoly: A firm’s decisions about P or Q can affect other firms and cause them to react. The firm will consider these reactions when making decisions • Game theory: the study of how people behave in strategic situations

QWhich one of the following statements is NOT applicable to the Bertrand model Firms choose price in response to the prices set by rivals. Firms make only a small amount of supernormal profit. In practice, firms have an incentive to collude. Firms are likely to engage in price-cutting behaviour. Nash equilibrium (in the absence of collusion) is where price is equal to average cost.

Oligopoly Non-collusive oligopoly: assumptions about rivals’ behaviour (cont.) Nash equilibrium when everyone makes a decision based on the alternatives rivals could adopt Nash equilibrium worse for the individual firms than the collusive equilibrium The kinked demand curve model assumptions of the model

Kinked demand for a firm under oligopoly Current price and quantity give one point on demand curve. P1 Q1 £ Q O

Kinked demand for a firm under oligopoly £ Assumption 1 If the firm raises its price, rivals will not. Assumption 2 If the firm reduces its price, rivals will feel forced to lower theirs too. D P1 D Q O Q1

QIn the kinked demand curve model, this kink is due to the firm’s belief that its competitors: will set a price at the kink of the demand curve. will match any price increase it makes, but will not match a price reduction. will not match a price increase but will match any price reduction. will match all price increases and reductions. will match neither price increases nor reductions.

Oligopoly Non-collusive oligopoly: assumptions about rivals’ behaviour (cont.) Nash equilibrium when everyone makes a decision based on the alternatives rivals could adopt Nash equilibrium worse for the individual firms than the collusive equilibrium The kinked demand curve model assumptions of the model stable prices

Stable price under conditions of a kinked demand curve MC2 MC1 a b MR £ MR is discontinuous between a and b. If MC is anywhere between MC1 and MC2, profit is maximised at Q1. P1 D = AR Q O Q1

Oligopoly Non-collusive oligopoly: assumptions about rivals’ behaviour (cont.) Nash equilibrium when everyone makes a decision based on the alternatives rivals could adopt Nash equilibrium worse for the individual firms than the collusive equilibrium The kinked demand curve model assumptions of the model stable prices limitations of the model

Oligopoly Oligopoly and the consumer advantages incentive to develop new and better products greater choice for consumers than under monopoly disadvantages less scope for economies of scale than under monopoly more extensive advertising and other costly marketing difficulties in drawing general conclusions

The end… (kind of!) Any Questions?