Download

1 / 45

450 likes | 472 Views

Presentation by Sergio Ugarte, former Vice Minister of Energy of Peru, explores energy policy challenges in South America and the need for regional integration to drive sustainable development through efficient interconnections and a unified energy market. The presentation highlights the current energy landscape, existing gas pipelines, and the potential economic benefits of fully integrated power markets.

E N D

BARRIERS TO ENERGY DEVELOPMENT IN SOUTH AMERICA Presentation by Sergio Ugarte, Northeastern University, Former Vice Minister of Energy Of Peru South America: Promoting Regional Integration CLAI, George Washington University - OAS March - 2002

Energy Sector PoliciesRegional Objectives • To transform South America into a developed Region, with standards of living which reflect the wealth of the land and the potential of its population

Energy Policy: The Value of Energy • A necessary condition, although not enough for social and economic development • Factor in competitiveness for the cost of goods and services • Impact onBalance of Payments

Sustainable Development Trilogy ENERGY ECONOMY ENVIRONMENT

Strategic: Economic: Social: Reduce the regulatory, thecnical and institutional restrictions that limit the development of efficient interconnections Design of a Regional Energy Market Improve overall efficiency to final user Design features of a Regional Transmission and Exchange System Enormous differences: in order to understand the Region, dispersions are just as important as median values. Energy Policies: The Challenges

The sufficient and economic energy supply is part of the Region Security.

Current Situation: • Until the 80’s, strong influence and participation of the state. • Last decade marked by profound reforms in almost all the region (decentralization, deregulation and privatization) • Mature and well established energy sectors, independent regulatory institutions, mostly privately power companies. • Interconnections are happening…but slowly

Current Situation (continuation): Two well differentiated sub-regions in South America: • Southern Sub-Region (Argentina, Bolivia, Brazil, Chile, Paraguay and Uruguay) with increased degree of integration. • Northern Sub-Region (Ecuador, Colombia, Peru and Venezuela), that must perfect their interconnection agreements. Peru and Bolivia are the natural hub for the whole regional integration. Their alliance and partnership is needed.

Current Situation (continuation): • Balance between energy sources • Power generation: 80% from hydro sources • Hydropower complementarity throughout the region. • Expectance in new natural gas fields in the region • Gas supply is rigid, due to the existence of oligopolies or natural monopolies and its demand is not yet well developed. • Gas infrastructure is modest in the region.

Hydropower complementarity adds enormous value to the interconnections

Potential of the Region • Potential to enlarge economies if power market were fully integrated. • Economic benefits of huge magnitudes by inter-fuel substitution and complementary characteristics of isolated systems as compared with the integrated system.

What do we lack? • Interconnection infrastructure facilities are weak where existent. • International trade agreements are not consistent, limiting severely the market integration. • Lack of incentives for interconnection expansion during initial stages. • Unclear regulatory definitions of firm transmission capacities. • Regulatory and institutional barriers that discriminate against international exchanges with regard to the national market

How do we revert the situation? • First, it is not just a technical problem, it is mainly political. • Market itself and improved regulations is NOT enough to break inertia of an almost a non-growth situation. • States MUST help to build the new infrastructure. Private sector cannot meet acceptable discount rates for some needed interconnections. • FIRM POLITICAL WILL FOR INTEGRATION IS NEEDED

This political decision means: • Acceptance that even under “critical conditions” energy supply could depend form generation abroad. • Leave border conflicts behind. • Allow international exchanges. • Guaranteeing non-discrimination and reciprocity in dealing with demand and supply from other countries. • Promoting efficiency in the use of resources. • Allowing open access to national transmission systems.

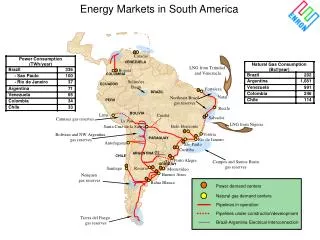

Developing a network scheme in South America Interconnections = Transport No difference between concepts of transport systems for goods, energy or communications

Problems to be addressed: • Define properly firm transmission concepts. • Establish short-term gas market in each regional hub (Sao Pablo – Buenos Aires). • Organize a spot market for mandatory sales of surpluses and deficits • Promotion of an interruptible gas market • Remove asymmetries in gas and power regulatory systems. • Higher regulatory risks for investors in an integrated regional power and gas scheme. • Integrated regulation for all businesses that converge with the use of same infrastructure.

Problems to be addressed (cont) National regulations compatible with regional integration Coordination between national transmission planning and the development of interconnections Legal fairness and protection Assurances of fair assignment of revenues between national investors and regional ones. Elimination of market price regulations which may distort the signals of efficient prices. Creation of suitable regional institutions Homologizing the performance criteria of every national system

We cannot pretend “Bueno, Bonito y Barato” (Good, Nice and Cheap) CALIFORNIA’S DISASTER. LESSONS:

Camisea DEVELOPMENT OF GAS MARKET IN PERU: THE CAMISEA PROJECT COLOMBIA ECUADOR UPSTREAM • Camisea Gas Fields • Cryogenic Separation plant in Camisea • Fractioning of condensates on the coast PERU BRASIL TRANSPORT & DISTRIBUTION Acre Cryogenic Plant GAS • Gas Pipeline: Camisea - City Gate in Lima • Liquids Pipeline - Camisea- Coast • Gas distribution network in Lima and Callao Lima EXPORT OF CONDENSATES BOLIVIA LPG LIQUIDS Liquid Fractioning LEGEND Titicaca Lake GAS PIPELINE EXPORT OF LPG LIQUIDS PIPELINE CHILE

32 28 24 20 16 12 8 4 Why natural gas massification?Reasons: Fuel Prices Lima – Commercial Clients / Small Industry January 2001 30 16 14 13 US$ / 106 BTU IGV 0.7 DBP 0.7 5 T&DAP 1.8 Gas 1.8 Electricity Diesel LPG Kerosene Natural Gas

Talara Aguaytía Piura Nerve center “Concentrator” Camisea Chiclayo Huancayo Oroya Trujillo Ayacucho Chimbote Lima Cuzco Apurimac Ica Marcona All the stages Arequipa Puno Moquegua Ilo Tacna LONG TERM VISION OF GAS FOR PERÚ

Energy Policy: The Resources Camisea 13 TCF Gas = 1,870 TWh Mantaro (840 MW) 6.5 TWh/yr 325 TWh in 50 yrs = 5.8

Energy Policy:The Resources Hydroelectric Potential 60 GW = 360 TWh/yr 18,000 TWh in 50 yrs Camisea 13 TCFGas = 1,870 TWh of Electrical Energy =10

Machu Picchu Cachimayo Dolores Pata Quencoro Abancay Combapata Tintaya Azangaro Charc.IV Juliaca Charc.VI Charc.V Puno Socabaya Chilina Botiflaca Cerro Verde Aricota 1 Ref.Ilo CT.Ilo Toquepala Aricota 2 Ilo Locumba Tomasiri Tacna La Yarada Colombia Ecuador Machala Zarumilla Zorritos Talara Sullana Arenal Piura Oeste Chachapoyas Moyobamba Paita C.H. Carhuaquero Tarapoto Chiclayo Oeste Brasil Cajamarca Guadalupe Bellavista Tocache Trujillo Norte M. Aguila Aguaytía Aucayacu Pucallpa C. Del Pato Tingo María Caraz Carhuaz Huánuco Chimbote Huaraz Der. Antamina Ticapampa Paragsha II Iñapari Yaupi Cahua Paramonga Carhuamayo Oroya Matucana Zapallal Pachachaca Callahuanca Ventanilla Huampaní Huayucachi Chavarría Pomacocha Huinco Santa Rosa Océano Pacífico Mantaro Moyopampa Puerto Maldonado San Juan Restitución Huanta Huancavelica Quillabamba Bolivia Ayacucho Independencia Andahuaylas Ica San Gaban Cotaruse Marcona San Nicolás Línea de 220 kV Línea de 138 kV Línea de 66 kV Moquegua Chile

NATIONAL GRIDS / ECUADOR - PERU - YEAR 2003 Coming Up : Peru-Ecuador connection

Are we clear in our vision of Regional Interconnection? • Interconnections are NOT “Passage ways”. They are Axis for Progress • They converge different network businesses: Gas, power and telecommunications. • The evolution of the regulation must take real advantage of this reality and it is not. • Meaning of Progress 70’s = Access to energy90’s = Access to InternetBut we are in the 21st Century now!

Convergence: • Power • Gas - Telecommunications NATIONAL AND CORPORATE STRATEGIC PERSPECTIVE

DIVERSIFICATION OF TRANSMISSION AND DISTRIBUTION BUSINESSCompetitiveness and mass marketing of the telecommunications business by use of the power transmission and distribution infrastructureState’s Role:To promote awareness of the value and potential of the transmission and distribution infratsructure and its contribution to the diversification of business

Convergence Power - Telecommunications GENERALIZED USEOF OPTICAL FIBERS USE OF TRANSMISSION AND DISTRIBUTION SYSTEMS (INFRASTRUCTURE AND RIGHTS-OF -WAY) DIGITALIZATION OF TELECOMMUNICATIONS PARTICIPATION OF POWER SECTOR IN TELECOMMUNICATIONS Europe: End of ‘ 80s Latin America: Recent experience

New Tariff System SYSTEMS GAS POWER NETWORKS