Download

1 / 22

220 likes | 226 Views

This article explains the concept of market equilibrium where supply meets demand, determining prices and quantities. It discusses excess demand, shortage, excess supply, surplus, and factors affecting demand and supply shifts. It also covers outcomes of simultaneous changes in supply and demand, as well as shortages, surpluses, price ceilings, price floors, and the importance of stable prices in economic activities.

E N D

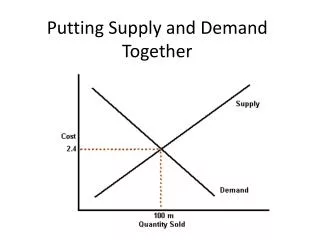

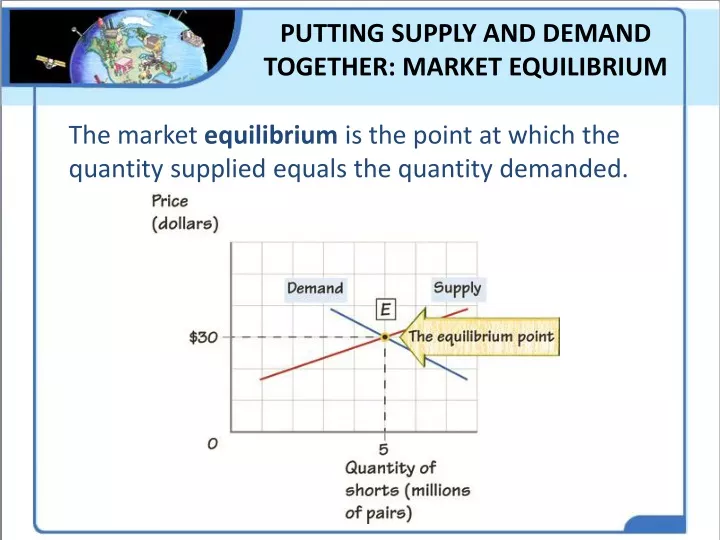

PUTTING SUPPLY AND DEMAND TOGETHER: MARKET EQUILIBRIUM The market equilibrium is the point at which the quantity supplied equals the quantity demanded.

PUTTING SUPPLY AND DEMAND TOGETHER: MARKET EQUILIBRIUM The equilibrium price is the price that equates the quantity supplied and the quantity demanded. The equilibrium quantity is the quantity that is supplied and demanded at the equilibrium price.

PUTTING SUPPLY AND DEMAND TOGETHER: MARKET EQUILIBRIUM When the quantity demanded is larger than the quantity supplied, the difference between them is called excess demand. This creates a SHORTAGE.

PUTTING SUPPLY AND DEMAND TOGETHER: MARKET EQUILIBRIUM When the quantity supplied is larger than the quantity demanded, the difference between them is called excess supply. This creates a SURPLUS.

CHANGES IN DEMAND An increase in demand = increase in PRICE and QUANTITY.

CHANGES IN DEMAND A decrease in demand = decrease in PRICE and QUANTITY.

A DECREASE IN SUPPLY A decrease in supply = increase in PRICE and a decrease in QUANTITY.

AN INCREASE IN SUPPLY An increase in supply = decrease in PRICE and an increase in QUANTITY.

CHANGES IN BOTH SUPPLY AND DEMAND If supply and demand decrease by the same amount, price will be unchanged and the quantity will decrease.

CHANGES IN BOTH SUPPLY AND DEMAND If supply decreases less than demand, price will decrease and quantity will decrease.

CHANGES IN BOTH SUPPLY AND DEMAND If supply decreases more than demand, price will increase and quantity will decrease.

CHANGES IN BOTH SUPPLY AND DEMAND If supply increases and demand decreases, the price will decrease and the quantity will not change.

SHIFTS IN DEMAND AND SUPPLY AND UNCERTAIN OUTCOMES When both demand and supply curves shift to the left, to the right or in opposite directions, there will be uncertainty in knowing the change on the market equilibrium. This table shows these changes.

SHORTAGES AND SURPLUSES A shortage exists when an excess demand for a product persists for a significant period of time. A SHORTAGE will cause price to INCREASE.

SHORTAGES AND SURPLUSES A surplus exists when an excess supply persists for a significant period of time. A SURPLUS will cause price to DECREASE.

PRICE CEILINGS A price ceiling is a government- imposed limit on the highest price firms can charge in a market. A price ceiling will cause a SHORTAGE.

PRICE FLOORS A price floor is a government- imposed limit below which prices cannot fall. Price floors tend to cause a SURPLUS.

STICKY PRICES Sticky prices are prices that move to their equilibrium values very slowly.

THE IMPORTANCE OF PRICES Rationing Rationing and the achievement of goals Finding the best level of production Keeping costs low Achieving consumer satisfaction

What Prices Accomplish • Prices guide the economy to the best level of production • Prices help keep costs low • Prices help achieve consumer satisfaction • Prices help prevent shortages