Download

1 / 13

130 likes | 241 Views

Lecture 5 The Market Equilibrium. ■ Market demand and supply ■ Reconciling suppliers and demanders ■ Equilibrium. Market demand and supply Going from the individual to the market. ■ We combine the demands of individuals by adding them horizontally

E N D

Lecture 5The Market Equilibrium ■ Market demand and supply ■ Reconciling suppliers and demanders ■ Equilibrium

Market demand and supplyGoing from the individual to the market ■ We combine the demands of individuals by adding them horizontally ■ We also combine the supplies of firms by adding them horizontally ■ The results are market demand and supply curves

Adding up demand curves At each price, sum the individual quantities demanded to get market quantity demanded P P P Dm = Da + Db + = P1 P1 P1 Da Db P2 P2 P2 Q1 Q2 Q1 Q2 Q1 Q2

Adding up supply curves At each price, sum the individual quantities supplied to get market quantity supplied P P P Sb Sm = Sa + Sb Sa P1 P1 P1 + = P2 P2 P2 Q1 Q2 Q1 Q2 Q1 Q2

Competition ■ Demanders compete with each other ►Their efforts tend to push price up, enriching suppliers ■ Suppliers compete with each other ► Their efforts tend to push price down, enriching demanders ■ Demanders do NOT compete with suppliers, even thought it sometimes seems that way! ► What about bargaining? Each party tries to convince the other of the powerful competition faced from alternatives

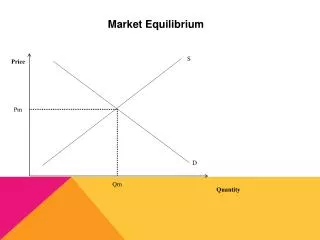

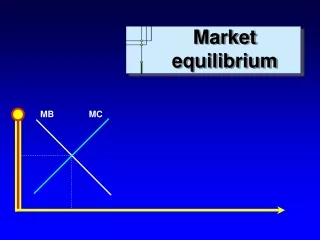

Equilibrium:The result of competition is mutually beneficial cooperation. At “equilibrium” no one has an incentive to change behavior: $ S P* D Q/time period Q*

Adjustments to equilibrium ■ Price above P* ► Quantity supplied exceeds quantity demanded: excess supply, or “surplus” ► Frustrated suppliers compete for business, lowering prices (“buyers’ market”) ► Price falls until market clears ■ Price below P* ► Quantity demanded exceeds quantity supplied: excess demand, or “shortage” ► Frustrated demanders compete for product, raising prices (“sellers’ market”) ► Price rises until market clears

Adjustment processWhat if the price is NOT right? ■Competition pushes price toward equilibrium P S Excess supply P high P low D Excess demand Q/time

One more time…The result of competition is mutually beneficial cooperation • In equilibrium, price and quantity will persist, until and unless there is a change in ceteris paribus conditions… P S P* D Q* Q/time

Question on Market Equilibrium • Suppose Toyota currently sells 100,000 cars each year in Hawaii. Does that mean there are 100,000 demanders of Toyotas in Hawaii?

Question on Market Equilibrium • Suppose the government of Hawaii imposes a 100% sales tax on new Toyotas. What will happen to price and quantity of Toyotas sold in Hawaii?

Questions • How do each of these events influence the equilibrium (i) price of airline tickets and (ii) quantity of airline trips taken 1. Rise in price of jet fuel 2. Depression in the economy 3. Threat of war 4. Government regulations making air travel safer

Questions True/false/uncertain: • An increase in the sales tax on a good will be paid for by consumers of the good. • It is important to producers of tires whether a tax on tires is paid by them or paid by consumers.