Download

1 / 19

190 likes | 353 Views

SCAN GLOBALLY, REINVENT LOCALLY: INNOVATING FINANCIAL MARKETS. Global Leadership Forum Kuala Lumpur September 6, 2005. Joseph E. Stiglitz Columbia University New York. INNOVATION AND FINANCE: KEYS TO SUCCESS IN A DYNAMIC MARKET ECONOMY. Need to scan globally To look for best practices

E N D

SCAN GLOBALLY, REINVENT LOCALLY:INNOVATING FINANCIAL MARKETS Global Leadership Forum Kuala Lumpur September 6, 2005 Joseph E. Stiglitz Columbia University New York

INNOVATION AND FINANCE: KEYS TO SUCCESS IN A DYNAMIC MARKET ECONOMY • Need to scan globally • To look for best practices • To look for failures • To see the circumstances in which different policies, institutions have worked well or failed • To assess what has best prospects of working • Reinvent locally • After determining the strengths and problems, challenges and opportunities of the local economy • “One size fits all” policies have failed

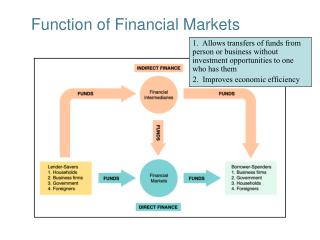

ROLE OF FINANCE AND FINANCIAL MARKETS • Allocates scarce capital - Brain of economy - Without access to capital, new enterprises cannot be created and old enterprises cannot grow • Monitors that it is used well • Redistributes risk - All investment is risky, and - Firms, individuals risk averse - Risk discourages investment - Innovative mechanisms for risk sharing can help promote investment, development and growth by lowering risk premium

FINANCIAL DYSFUNCTION AND RISKS OF LIBERALIZATION • Poorly designed, managed financial systems can impede growth • Macro instability • Lack of access to capital • Access only at high cost • While liberalization and innovation are intended to improve the functioning of capital markets • Overall risk is increased • Capital is less well allocated • Certain groups no longer have access to capital • Cost of capital actually increases

EXAMPLE: RISKS OF FINANCIAL INNOVATION • Some of innovations in financial markets, including those for divesting risk also increase opportunity for risk taking • Derivatives • Have been abused, especially in under-regulated markets • To avoid taxes • Led to conflicts of interest • Evident in the U.S. during the “Roaring 90s” • Leading to • Misallocated and over investment • More macro instability, huge underperformance of economy • Lower growth

IMPLICATIONS • Signifies the importance of good financial market regulations • Cannot separate out “micro-” and “macro-” regulations • Prudential regulations have important macroeconomic effects

EXAMPLE: CAPITAL MARKET LIBERALIZATION • Was supposed to increase growth and stability • Actually led to more instability • And not to increased growth - Consistent with economic theory based on imperfect (asymmetric) information - Even IMF now recognizes this - IMF models assumed perfect information • Failed to understand modern advances in economic theory • Their models were internally incoherent— they talked about problems of lack of transparency and bankruptcy, but their models did not incorporate these phenomena

EXAMPLE: PROBLEMS WITH ACCESS TO FINANCE • Long history of concern that unrestricted markets may lead some groups in the society to be underserved • Predicted consequence of the theories of financial markets based on asymmetric information • Explains the historical U.S. policy of limiting inter-state banking • Lending (CRA) and branch requirements in the U.S, India have proven to be effective

SOUTH EAST ASIA IN THE GLOBAL CONTEXT • Peculiarities of global financial market • Risk of exchange rate and interest rate fluctuations born by developing countries • Though “theory” predicts it should be borne by those more able to bear risk • The richest country in the world borrowing huge amounts from poorer countries • Though “theory” predicts flows of capital should move in the opposite direction • Asia, especially South East Asia, is the major source of global savings • And yet the dollar continues to be viewed as the reserve currency • And much of Asian savings is “mediated” by Western capital markets

PUZZLES AND PARADOXES: THE GLOBAL ECONOMY • Risk premia very low • Yet high levels of risk, uncertainty—exchange rate volatility, oil prices, global imbalances • Low ‘risk premia’ sometimes attributed to global savings “glut” • Yet huge U.S. deficits, which look like they will be getting larger • Soaring oil prices • Yet investments in alternative energies, conservation have not increased much

PUZZLES AND PARADOXES: THE U.S. ECONOMY • Short term interest rates have continually increased in the last two years • Yet long term interest rates have fallen • Interest rate decreases have failed to stimulate business investment • Though it did lead to real estate boom (bubble) • U.S. Consumption level remains strong • Yet real wages stagnate • Huge turnaround in the U.S. fiscal position - from 2% surplus to 4% deficit • Less stimulation to U.S. economy than one would have expected

CHANGES ARE IN THE WIND: END OF DOLLAR AS A RESERVE CURRENCY • Dollar losing the status of reserve currency • Already evident in changes in private holdings and some Central Bank portfolios • Exchange rate instability means that dollar is no longer good store of value – what matters to countries is a ‘reserve of wealth’ • Instability likely to continue • As U.S. fiscal and trade deficits continue to increase • U.S. fiscal deficits may further increase with • Permanent tax cuts • Social security reforms (probably dead) • Other tax reforms • Costs of war in Iraq • Borrowing not being used to finance investment • What countries need to do is to manage their wealth • Which entails risk diversification

INNOVATIVE RESPONSES • Reforms in the global reserve system • Problems are inherent in current system • But reforms will be difficult given the resistance from U.S., even though it would be in best interests of U.S. • Current system not only leads to instability • But there is a huge opportunity cost in holding dollar reserves • Exchange rate and interest rate volatility is likely to remain large • Need to recognize huge costs associated with freely flexible exchange rates • Though as Argentine experience showed, there can be huge costs associated with excessively rigid exchange rates as well • Need to have regulatory frameworks that recognize this, mitigate consequences • Need to find innovative ways of transferring, absorbing risk better within Asia, managing Asian financial markets • Asian Monetary Fund • Chang Mai Initiative

MANAGINGS THE RISKS OF HIGH ENERGY PRICES • Why have high energy prices so far failed to elicit supply response? • Long lags • Uncertainty about whether prices will remain high: low costs of production in Saudi Arabia • What is needed is more conservation • But, unfortunately, largest energy consumer (US) just passed energy bill which did little for conservation • ‘Drain America First’ policy leaves the U.S. more vulnerable to supply disruptions • And free market economics has left Europe more vulnerable to gas interruptions from Russia • While financial markets themselves provide only limited “insurance” against these risks

MANAGING THE RISKS OF HIGH ENERGY PRICES • The ‘best’ way of managing risk is to own energy-based assets • Global market place makes this possible • Even countries with high energy dependence can thus mitigate risk • But this means a different approach to managing nation’s “reserves”, national asset management • Has consequences both for distribution of income within and among countries and for macro-stability

MANAGING ONE’S OWN WEALTH Lessons of the “Class of ’97” • Control does matter • Decisions about moving money into and out of country can have huge consequences for entire country, not just capital markets • Asia, especially South East Asia, pays huge costs for “cycling” money through the U.S. • Differences between rate paid by US (e.g. Treasury Bill) and rate paid to US (lending rate) • Huge costs of reserves • Lack of control

MANAGING ONE’S OWN WEALTH • Strengthening Asian financial markets would thus increase income, growth and stability • May require development of new financial instruments • Paying in a new unit of account • Based on a weighted average of currencies • Backed by governments • Perhaps through creation of new Asian Monetary Fund

SOUTH EAST ASIA: BETWEEN TWO GIANTS • Fast changing global economy • With correspondingly fast changes in comparative advantages • Dynamic and static comparative advantage • Even with globalization, borders do matter • One of the reasons why investors are attracted to China • But lying between two giants – China and India - gives South East Asia some distinct advantages • “Cross Roads” • And entrepreneurial intermediary • Knowledge of both economies • Access to both economies • Dual role, both competitor and complement

SOUTHEAST ASIA: BETWEEN TWO GIANTS • This will require countries of South East Asia to reassess their dynamic comparative advantages • Niche markets • High innovation • Enhancing intermediary roles • Innovative financial markets will play a key role in redeployment of resources • And will enable South East Asian countries to sustain the remarkable growth rates of the last three decades