Download

1 / 28

280 likes | 434 Views

Taxes on Labor Supply. Chapter 21. 21.1 Taxation and Labor Supply—Theory. 21.2 Taxation and Labor Supply—Evidence. 21.3 Tax Policy to Promote Labor Supply: The Earned Income Tax Credit. 21.4 The Tax Treatment of Child Care and Its Impact on Labor Supply. 21.5 Conclusion.

E N D

Taxes on Labor Supply Chapter 21 • 21.1 Taxation and Labor Supply—Theory • 21.2 Taxation and Labor Supply—Evidence • 21.3 Tax Policy to Promote Labor Supply: The Earned Income Tax Credit • 21.4 The Tax Treatment of Child Care and Its Impact on Labor Supply • 21.5 Conclusion

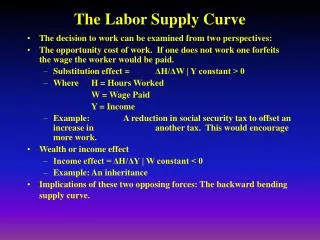

21 . 1 • Basic Theory • Taxation and Labor Supply—Theory • The slope of Ava’s budget constraint is now the after-tax wage.

21 . 1 For understanding the intuition of the income effect on labor supply it is sometimes helpful to think about an individual’s income target, his or her goal of earning a fixed amount of income. • Basic Theory • Substitution and Income Effects on Labor Supply • Taxation and Labor Supply—Theory • The decrease in the price of leisure will induce a substitution effect toward more leisure and less work. • A reduction in income will have an incomeeffect that causes her to buy fewer of all normal goods, including leisure. • Because the substitution and income effects on labor supply pull in opposite directions, we cannot predict clearly whether labor supply rises or falls in response to the tax.

21 . 1 • Basic Theory • Substitution and Income Effects on Labor Supply • Taxation and Labor Supply—Theory

21 . 1 • Limitations of the Theory: Constraints on Hours Worked and Overtime Pay Rules • Taxation and Labor Supply—Theory • Production complementarities are features of the production process that make it important to have many workers on the job at the same time. • overtime pay rules Workers in most jobs must legally be paid one and a half times their regular hourly pay if they work more than 40 hours per week.

21 . 2 • primary earners Family members who are the main source of labor income for a household. • Taxation and Labor Supply—Evidence • secondary earners Workers in the family other than the primary earners.

E M P I R I C A L E V I D E N C E • ESTIMATING THE ELASTICITY OF LABOR SUPPLY • Three approaches have been used to estimate the elasticity of labor supply with respect to the after-tax wage: • Cross-Sectional Linear Regression Evidence: These studies estimate regressions of labor supply as a function of the after-tax wage and other control variables. • Experimental Evidence: Another approach suggested for assessing the causal impact of taxation on labor supply is a randomized experiment. In fact, one of the most significant social experiments in the United States was a randomized evaluation of a negative income tax (NIT) system. • Quasi-Experimental Evidence: Perhaps the best known of these studies is Nada Eissa’s studies of the impact of the Tax Reform Act of 1986 (TRA 86) on labor supply. Eissa noted that this major tax reform lowered the tax rates on the very-highest-income taxpayers much more than it lowered rates on those who were moderately high-income.

21 . 2 • Limitations of Existing Studies • Taxation and Labor Supply—Evidence • One important issue raised by this literature is the blurring of lines between primary and secondary earners. • Another important limitation of this literature has been its focus on only a subset of the possible measures of labor supply, labor force participation, and hours of work.

21 . 3 • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit • Earned Income Tax Credit (EITC) A federal income tax policy that subsidizes the wages of low income earners. • The EITC subsidizes the wages of low-income earners to accomplish two goals: • Redistribution of resources to lower-income groups. • Increases in the amount of labor supplied by these groups.

21 . 3 • Background on the EITC • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit • To be eligible for the EITC, a family must have annual earnings greater than zero and below about $34,000, if supporting one child, or $36,000 if supporting more than one child. A family with no children must have earnings greater than zero and below about $12,000. For childless families, the EITC is significantly smaller.

21 . 3 • Background on the EITC • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit

21 . 3 • Impact of EITC on Labor Supply: Theory • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit

21 . 3 • Impact of EITC on Labor Supply: Theory • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit • This figure illustrates the impact of the EITC on four distinct groups: • 1. People not in the labor force at all. • 2. People already in the labor force who earn less than $11,340. • 3. People already in the labor force and earning between $11,340 and $14,810. • 4. People already in the labor force earning between $14,810 and $36,348.

21 . 3 • Impact of EITC on Labor Supply: Evidence • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit

21 . 3 • Impact of EITC on Labor Supply: Evidence • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit • The literature assessing the effect of the EITC has reached several clear conclusions: • Effects on Labor Force Participation • There is a strong consensus across these studies that the EITC has played an important role in increasing the share of single mothers who work. • Effects on Hours of Work • The 1986 expansion in the EITC would have been expected to increase labor force participation, but it might also have reduced hours worked by those already in the labor force. • Impact on Married Couples • Although the EITC appears to have positive effects for the labor supply of single mothers, it might have negative impacts on a married couple’s labor supply decisions.

E M P I R I C A L E V I D E N C E • THE EFFECT OF THE EITC ON SINGLE MOTHER LABOR SUPPLY • Studies of the effect of the EITC on the single mother labor supply typically exploit quasi-experimental changes in the nature of the EITC over time. • Eissa and Leibman studied the impact of the EITC policy change by comparing the labor supply of single women with children (the treatment group, which was affected by this policy change) to the labor supply of single women without children (the control group). • The researchers found a large effect of the EITC expansions on the labor supply of single mothers: they estimate such women were 1.4 to 3.7 percentage points more likely to work as a result of this program.

21 . 3 • Summary of the Evidence • Tax Policy to Promote Labor Supply: The Earned Income Tax Credit • Overall, the United States’ experience with the EITC seems fairly successful. • It is a powerful redistributive device that now delivers more cash to low-income families than any other welfare program. • It has done so without reducing overall labor supply, the problem with standard cash welfare.

EITC Reform • While the EITC has been a major success story, there are significant flaws in its design: • For example, there is only a very small EITC for childless workers, with a maximum of only $412 per year. • Another flaw is that families receive no additional EITC transfer as family size grows beyond two children. • Another major objection to the current form of the EITC is that it penalizes many single parents who subsequently marry because the credit is based on the income of the tax filing unit. • Not all marriages are, however, penalized by the EITC. • Take the case of a single mother with two children and no income. If she marries a man whose annual income is $12,000, then together they qualify for the maximum credit of $4,536, even though on her own she would not receive any credit.

21 . 4 • The Tax Treatment of Child Care and Its Impact on Labor Supply • child care Care provided for children by someone other than the parents of those children.

21 . 4 Here, we refer to tax wedges across input markets, where tax wedges are the difference between the returns to the input (labor supply) in the different markets. • The Tax Treatment of Child Care • The Tax Treatment of Child Care and Its Impact on Labor Supply • broadest definition of tax wedges Any difference between pre- and post-tax returns to an activity caused by taxes.

E M P I R I C A L E V I D E N C E • THE EFFECT OF CHILD CARE COSTS ON MATERNAL LABOR SUPPLY • The barrier to secondary earner participation in the labor market posed by child care costs has led to studies of the responsiveness of labor supply to child care costs. • Berger and Black (1992) looked at women on welfare who applied for a limited pool of child care subsidies. • Gelbach (2002) pursued an alternative innovative strategy: he took advantage of kindergarten birthday cutoffs. • Baker et al. (2005) considered a third approach. • In the late 1990s, the Canadian province of Quebec passed a law providing universal access to child care for all families in the province for only $5/day, reflecting a subsidy of about 85% off the market price for child care at the time. • They pursued a quasi-experimental difference-indifference analysis of the labor supply of married women before and after this policy change in Quebec, relative to the rest of Canada.

21 . 4 • Options for Resolving Tax Wedges • The Tax Treatment of Child Care and Its Impact on Labor Supply • A general point about tax wedges between taxed and untaxed activities is that such tax wedges distort behavior by encouraging people to undertake the untaxed activities and cause deadweight loss. • Public finance economists often say that such tax wedges create an uneven playing field across economic activities, where individuals are treated differently because of the choices they make.

21 . 4 • Options for Resolving Tax Wedges • The Tax Treatment of Child Care and Its Impact on Labor Supply • Imputing Home Earnings • One way that policy makers could level the playing field would be to tax at-home work just as we tax work in the market. • imputing home earnings Assigning a dollar value to the earnings from work at home.

21 . 4 • Options for Resolving Tax Wedges • The Tax Treatment of Child Care and Its Impact on Labor Supply • Deductible Child Care Costs • The other alternative is to make market child care costs deductible. Suppose now that work at home is not taxed but that the government allows each family to deduct the cost of child care from its taxable income. • Thus, there are two ways to even a playing field: • By taxing all activities equally, or • By subsidizing all activities equally.

21 . 4 • Comparing the Options • The Tax Treatment of Child Care and Its Impact on Labor Supply • While both these solutions level the playing field, their effects on the tax base are not identical: allowing a deduction for child care costs has lowered the tax base. • Thus, we are faced with three choices, all of which have drawbacks: • We can continue to have an uneven playing field, which lowers social efficiency by deterring mothers from market work. • We can even the playing field by taxing home work, which makes the most economic sense but is an administrative nightmare. • We can level the playing field by offering subsidies to market work, which reduces the overall efficiency of the tax system.

21 . 5 • If higher taxes lead people to change their behavior to supply less labor, these changes can offset the gains from tax increases and there might be a natural limit to the revenue that can be raised by income taxation. • Most studies show that tax rates have little impact on the labor supply of primary earners but a more substantial impact on secondary earners. • We reviewed one of the major tax policies to promote labor supply, the Earned Income Tax Credit (EITC), and discussed evidence showing that the EITC has raised the labor supply for low-income earners. • Finally, we discussed the appropriate tax treatment of child care. • Conclusion