Download

1 / 8

80 likes | 263 Views

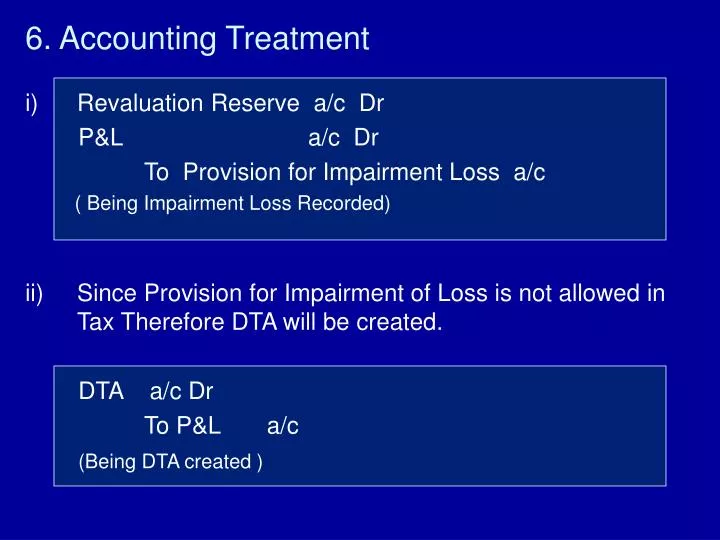

6. Accounting Treatment. Revaluation Reserve a/c Dr P&L a/c Dr To Provision for Impairment Loss a/c ( Being Impairment Loss Recorded)

E N D

6. Accounting Treatment • Revaluation Reserve a/c Dr P&L a/c Dr To Provision for Impairment Loss a/c ( Being Impairment Loss Recorded) • Since Provision for Impairment of Loss is not allowed in Tax Therefore DTA will be created. DTA a/c Dr To P&L a/c (Being DTA created )

iii. Presentation in Balance Sheet : Fixed Asset ---------- Add: Accumulated Dep ---------- Less: Provision / Impairment Loss ---------- ******** iv. Depreciation for subsequent period will reduce due to Impairment loss SLM = ( Carrying Amount – I/Loss ) – Sale Value Remaining life WDV ( Rate of Dep. If not given) = 1 - Scrap Value1/Life Revised CA

7. Treatment of Goodwill ( Same for Corporate Asset) Case A :Where Goodwill is allocable in reasonable ratio ; Apply Bottom Up Approach ( BU Approach). Step 1 : Calculate Carrying Amount of Asset in Cash Generating Unit (CGU) . Step 2 : Allocate Goodwill among CGU in reasonable ratio. Step 3 : Compare total CA ( Step 1 + Step 2) with RA of CGU, to get Impairment Loss if any. Step 4 : Attribute Impairment Los among assets : • First to Goodwill allocated to CGU • Balance Impairment loss to various assets including corporate assets, in ratio of Carrying Amount.

Case B :Goodwill not allocable. Apply BU approach and TD Approach. Step 1: Calculate revised carrying amt of all assets in all CGUs including allocated Goodwill. Step 2: Consolidate all revised Carrying Amount and Carrying Amount of unallocable Goodwill. Step 3: Compare value of Step 2 with Recoverable Amount of entity as whole. Impairment Loss will be attributed to: • Unallocated GW and Balance to • Unallocated Corporate Assets in ratio of Carrying Amount.

8. Reversal of Impairment Loss Whenever reversal of Impairment Loss is to calculated, there should be impairment loss recognized earlier. Reversal can not be more than earlier Impairment Loss. Calculation of Reversal : Lower of the limit Limit A = Impairment Loss - Dep. Advantage Recognised Earlier Availed Limit B = Recoverable Amount - Carrying Amount Impairment Loss of Goodwill will never be reversed.

9. Whenever NSP becomes negative than, Entity should make provision for expected cost of disposal. In such cases NSP will be considered as Zero. Impairment Loss will be calculated as usual.

At each B/s, all entities should check for any indicators for reversal. Following can be indicators : External Indicator : • MP of assets hace increased. • Rate of Interest have declined. • Favorable Market Price. • ------- Internal Indicators : • ------- • Best Economic Performance • Entity have made plans of Restructuring.

11. Disclosure Requirements : • Impairment Loss Recognized in P&L A/c. • Impairment Loss Recognized in Revaluation Reserve. • Impairment Loss Reversed Recognized in P&L A/c. • Impairment Loss Reversed Recognized in Revaluation Reserve. • Segment affected due to impairment. • Indicators due to which AS 28 was applied. • Basis of NSP • Value in use details for example Discount Rate, period of Cash flows.