Download

1 / 25

250 likes | 364 Views

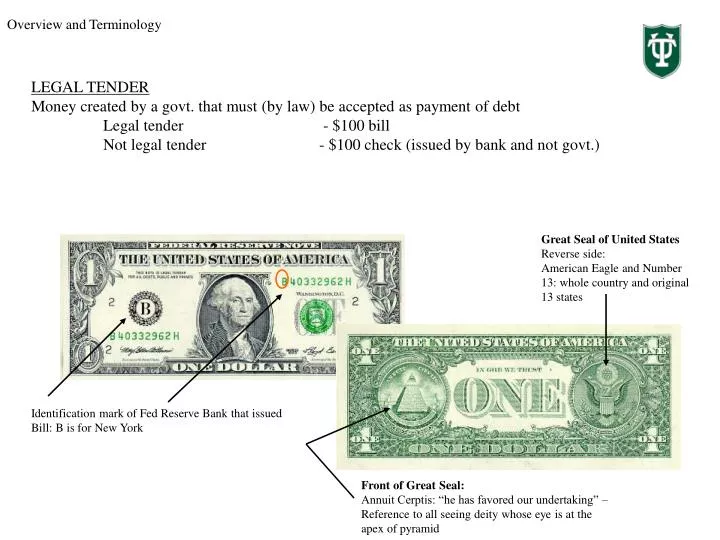

Overview and Terminology. LEGAL TENDER Money created by a govt. that must (by law) be accepted as payment of debt Legal tender - $100 bill Not legal tender - $100 check (issued by bank and not govt.). Great Seal of United States Reverse side:

E N D

Overview and Terminology LEGAL TENDER Money created by a govt. that must (by law) be accepted as payment of debt Legal tender - $100 bill Not legal tender - $100 check (issued by bank and not govt.) Great Seal of United States Reverse side: American Eagle and Number 13: whole country and original 13 states Identification mark of Fed Reserve Bank that issued Bill: B is for New York Front of Great Seal: Annuit Cerptis: “he has favored our undertaking” – Reference to all seeing deity whose eye is at the apex of pyramid

Overview and Terminology • GOLD STANDARD: 1876 until 1913 (World War I) • Relative value of currencies was measured against precious metals like gold or silver • Each country set the rate at which its currency could be converted to gold • Must maintain adequate reserves of gold (Fort Nox) for redemption • Gold standard implied a fixed exchange rate • Implicitly limited the rate at which any individual country could expand its money supply (had to have adequate gold on hand) • Worked very well until 1913 when WWI interrupted free movement of gold for reserves • 1879-1971: U.S. stopped redeeming its paper currency with gold. . • Example: • US$ gold rate was $20.67/oz, • British pound was pegged at £4.2474/oz • US$/£ rate calculation is $20.67/£4.2472 = $4.8665/£

WWI to 1971 • 1945-1973: Fixed Exchange Rates • Dollar main reserve currency held by central banks-key to web of exchange rate value • US running persistent + growing deficits – heavy outflow of dollars required to finance deficit + meet growing demand for dollars from business/investors • Lack of confidence of US to meet its commitment to convert dollars to gold forced President Nixon to suspend official purchases or sales of gold on Aug. 15, 1971 • Exchange rates of most leading countries were allowed to float in relation to the US dollar • By the end of 1971, most of the major trading currencies had appreciated vis-à-vis the US dollar; i.e. the dollar depreciated • A year and a half later, the dollar came under attack again and lost 10% of its value • By early 1973 a fixed rate system no longer seemed feasible and the dollar, along with the other major currencies was allowed to float • By June 1973, the dollar had lost another 10% in value

1971 forward 1971: gold standard abandoned 1971 + : currencies ‘FLOAT’ influenced by : supply and demand greater demand for nation’s product = greater demand for currency greater demand for nation’s stocks/bonds = greater demand for currency low inflation rate stable government and governmental policies government intervention regarding currency management governmental intervention to defend value of its currency agreements to lower interest rates deliberate devaluation of a currency (make exports more competitive) Govt. Intervention: Group of 5 effort to depreciate the dollar by 35% in 10 months: Sept 1985 – selling billions of dollars to drive down the value of dollar.

Fed Reserve System • FEDERAL RESERVE SYSTEM- founded in 1913 • Guardian of the Nation’s money • 12 separate distinct banks, 25 regional branches • System run by 7-member Board of Governors (appointed by President, confirmed by Congress) • Open Market Committee- responsible for guiding day to day money decisions • discount rate

Euro and Monetary Unification • The euro, €, was launched on Jan. 4, 1999 • Effects for countries using the euro currency include • Cheaper transaction costs, • Currency risks and costs related to exchange rate uncertainty are reduced, • All consumers and businesses, both inside and outside of the euro zone enjoy price transparency and increased price-based competition

Euro and Monetary Unification Convergence criteria called for countries’ monetary and fiscal policies to be integrated and coordinated • Nominal inflation should be no more than 1.5% above average for the three members of the EU with lowest inflation rates during previous year • Long-term interest rates should be no more than 2% above average for the three members of the EU with lowest interest rates • Fiscal deficit should be no more than 3% of GDP • Government debt should be no more than 60% of GDP European Central Bank (ECB) was established to promote price stability within the EU

Emerging Market Country High capital mobility is forcing emerging market nations to choose between two extremes Emerging Markets and Currency Regime Choices • Currency Board or Dollarization • Currency Board fixes the value of the local currency or basket; Dollarization replaces currency with the US dollar • Independent monetary policy is lost; political influence on monetary policy is eliminated • Seignorage, the benefits accruing to a government from the ability to print its own money, is lost • Free-Floating Regime • Currency value is free to float up and down with international market forces • Independent monetary policy and free movement of capital allowed, but at the loss of stability • Increased volatility may be more than what a small financial market can withstand

Overview and Terminology Foreign Exchange Markets • The FOREX market provides the physical and institutional structure through which the money of one country is exchanged for that of another country • A foreign exchange transaction is an agreement between a buyer and a seller that a fixed amount of one currency will be delivered for some other currency at a specified rate

Geographics • Geographically, the FOREX market spans the globe with prices moving and currencies trading on a 24 hour basis • Major exchanges are located in Singapore, Hong Kong and Tokyo in the East • Then it moves to Bahrain, and London for the European area • And on to New York, San Francisco and Sydney

Tokyo opens Asia closing 10 AM In Tokyo Europe opening Americas open London closing Afternoon in America 6 pm In NY Lunch In Tokyo Geographics Measuring FOREX Market Activity: Average Electronic Conversations Per Hour Greenwich Mean Time

Market Size Global Foreign Exchange Market Turnover (daily averages in April, billions of US dollars) Source: Bank for International Settlements, “Central Bank Survey of Foreign Exchange and Derivatives Market Activity in April 2001,” October 2001, www.bis.org.

Market Size Geographic Distribution of Foreign Exchange Market Turnover (daily averages in April, billions of US dollars) Source: Bank for International Settlements, “Central Bank Survey of Foreign Exchange and Derivatives Market Activity in April 2001,” October 2001, www.bis.org.

Market Size Currency Distribution of Global Foreign Exchange Market Turnover (percentage shares of average daily turnover in April) Source: Bank for International Settlements, “Central Bank Survey of Foreign Exchange and Derivatives Market Activity in April 2001,” October 2001, www.bis.org.

Functions • The FOREX market is the mechanism by which participants transfer: • purchasing power between countries • obtains or provides credit for international trade • minimizes exposure to exchange rate risk • FOREX: each party wants to transact in its own currency • FOREX market provides credit (letters of credit) • FOREX market provides ‘hedging’ facilities

Market Participants • The FOREX market consists of two tiers • Interbank • Client or retail market • Five broad categories of participants operate within these two tiers • Bank and non bank foreign exchange dealers • Individuals and firms conducting commercial or investment transactions • Speculators and arbitragers • Central banks and treasuries • Foreign exchange brokers

Bank and Non-Bank Dealers • These participants profit from buying currencies at a bid price and then reselling them at an offer or ask price • Competition among dealers • Narrows the spread between the bid and offer rate • Promotes the market’s efficiency • Dealers on behalf of large international banks often act as market makers, often willing to stand in and buy or sell these currencies without having a counterpart with which to unload the “inventory” • They trade amongst other banks and dealers in order to keep their inventory levels at manageable levels • Currency trading is profitable and often contributes between 10% - 20% of a banks’ average net income • Small- to medium-sized banks rarely act as market makers yet still participate in the interbank market

Individuals/Firms Conducting Commercial/Investment Transactions • Importers, exporters, portfolio investors, MNEs, tourists and others use the FOREX market to facilitate execution of commercial or investment transactions • Some of these participants use the market to hedge foreign exchange rate risk

Speculators and Arbitragers • Speculators and arbitragers seek to profit from trading in the market itself • They operate for their own interest, without need or obligation to serve clients or ensure a continuous market • Speculators seek all their profit from exchange rate changes • Arbitragers try to profit from simultaneous differences in exchange rates in different markets • A large proportion of speculation and arbitrage is conducted on behalf of major banks by traders employed by those banks

Central Banks and Treasuries • Acquire/spend their country’s currency reserves • Influence the price at which their own currency trades • Support the value of their currency • Motive is not to profit but rather influence the foreign exchange value of their currency in a manner that will benefit their interests

Foreign Exchange Brokers • Foreign exchange brokers are agents who facilitate trading between dealers without themselves becoming principals in the transaction • For this service they charge a small commission • They maintain instant access to hundreds of dealers worldwide via open lines and at times may maintain such lines with several banks, with separate lines for differing currencies, spot and forward rates

Spot Transactions A spot transaction in the interbank market is the purchase of foreign exchange, with delivery and payment between banks to take place, normally, on the second following business day • The settlement date is often referred to as the value date • This is the date when most dollar transactions are settled through the computerized Clearing House Interbank Payment Systems (CHIPS) in New York

MONEY: Currency Cross Rates • Foreign Exchange Quotes: • Direct: quote is the price of a foreign currency unit in terms of the home currency (dollar denominator) • Indirect: quote is the price of a unit of home currency measured in the foreign currency. • Indirect = USD/EUR = 0.79 is the same as .79 Euro will buy $1 dollar • Direct = EUR/USD = 1.26 is the same as $1.26 buys 1 euro (this is how the markets quotes the Euro (how many dollars to buy 1 Euro). This is NOT a FRACTION but as “Euros in dollar prices”. • Convention: • quote’s definition depends on country of reference • NY bankers established European Terms Convention, which uses the US Dollar as the common denominator. • Traders in US, Switzerland, etc would quote CHF as 1.4866 / $1 dollar. (1.4866 Swisse to buy $1) INDIRECT • Exceptions: British Pound Sterling, Australia, New Zealand and Euro-quoted DIRECT Indirect Direct

Quoting Foreign Exchange (FX)-Spot Pricing • 10/29/02: Live FX Spot Market as Offered by IFX LONDON • Notice the conventions: • Euro quoted as direct (EUR/USD) • Swiss Franc quoted as indirect (USD/CHF) • Pound Sterling quoted as direct (GBP/USD) The Spot Market: Conventions

Spot Transaction Trading: Retail Trading • SPOT EXCHANGE RATE MARKET • FX trading is normally undertaken on the basis of margin trading (‘gearing’). • Small deposit needed to control a much larger position in market-possible because one buys one currency and simultaneously sell another • Margins are set by dealer • To swing $1,000,000, one must deposit $20,000 in account – margins are 2% Commercial Banks normally trade in $1M lots IFX allows trading in partial lots Notice, trade is .2 lots (margin is 2 x $2,000= $4K)