Download

1 / 11

110 likes | 191 Views

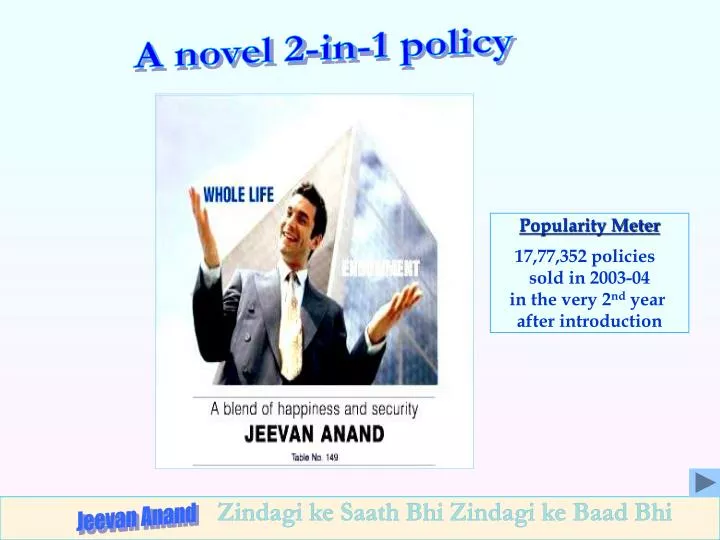

A novel 2-in-1 policy. Popularity Meter 17,77,352 policies sold in 2003-04 in the very 2 nd year after introduction. Attractions. Combines benefits of Endowment and Whole Life Policy. Intro. features. Financial protection against death throughout the lifetime with the

E N D

A novel 2-in-1 policy Popularity Meter 17,77,352 policies sold in 2003-04 in the very 2nd year after introduction

Attractions Combines benefits of Endowment and Whole Life Policy Intro features Financial protection against death throughout the lifetime with the provision for payment of lumpsum at the end of the term in case of survival benefits illustrations

Attractions Enjoy your savings in your lifetime & also provide financial security for family Intro features Exclusive Limit for Free Accident Cover upto Rs. 5 lakhs benefits illustrations Only plan of its kind

features For how many years is premium payable ? You can choose premium payment terms between 5 and 57 years Who can avail of this plan? Male lives and female lives having their own income aged between 18 years (completed) and 65 years (near birthday) Intro features For what sums is insurance available under this plan ? Minimum Rs. 1 lakh. Maximum : no limit, but depends upon income At what frequency can premium be paid? Yearly, Half-Yearly, Quarterly, SSS benefits illustrations

optional features Critical Illness Rider : Eligibility (A)Minimum entry age : 18 yrs (completed) (B) Maximum entry age : 50 yrs (nearer birthday) (C) Maximum maturity age : 60 years (D) Minimum Sum Assured for the Critical illness Rider : Rs.50,000/= (E) Minimum Sum Assured of the Main plan on which the Critical illness Rider can be given: Rs.50,000 (F) Maximum Sum Assured : An amount equal to the Basic Sum for the Critical Illness Rider Assured, subject to a maximum of Rs.5,00,000. (G) Term : 10 to 35 years under regular premium 5 to 35 years under Single premium and 15, 20 & 25 years under limited premium paying term policies. This rider is allowed only if the maturity age under main policy is not greater than 60 years. The policy term and premium paying term of the rider should match with the policy term and premium paying term under the main policy. Intro features benefits illustrations

optional features Critical Illness Rider : Benefits • Critical Illness Sum Assured is payable on life assured surviving for a period of 28 days from date of occurrence of any of the following critical illnesses- • Heart Attack (Myocardial Infarction) • Stroke (Cerebro-vascular Accident) • Cancer • Kidney Failure • Major Organ transplant • Paralysis • 3rd Degree Burns • Blindness • Coronary Artery By-pass Surgery • Heart Valve Replacement or Repair • Aorta Graft Surgery • Premium Waiver Benefit: • A policyholder has option to avail of a premium waiver benefit whereby premiums falling due on or after the date of diagnosis of critical illness are waived till maturity date of the main plan or earlier death of the life assured. Intro features benefits illustrations

Sample Premium Chart Annual Premium Rs. Intro features benefits illustrations

When are benefits payable? Survival Benefit : When the policyholder survives till date of maturity and policy is in force, Full sum assured + vested bonuses + final additional bonus, if any, is payable. Risk cover continues after maturity, without need to pay premium Risk Cover : On death during premium payment period, Full sum assured + vested bonuses + final additional bonus, if any, is payable. On death after premium paying period, Full sum assured is payable. Intro features benefits illustrations

Illustrations Age at entry: 35 years Premium paying term: 25 years Mode of premium payment: Yearly Sum Assured: Rs.1,00,000/- Annual Premium: Rs.4,535 /- Intro features benefits illustrations

Illustrations Age at entry: 35 years Premium paying term: 25 years Mode of premium payment: Yearly Sum Assured: Rs.1,00,000/- Annual Premium: Rs.4,535 /- Intro features benefits illustrations

Illustrations: Assumptions and Disclaimer The illustration is applicable to a non-smoker male/female standard (from medical, life style and occupation point of view) life. The non-guaranteed benefits in the illustrations are calculated so that they are consistent with the Projected Investment Rate of Return assumption of 6% p.a.(Scenario 1) and 10% p.a. (Scenario 2) respectively. In other words, in preparing this benefit illustration, it is assumed that the Projected Investment Rate of Return that LICI will be able to earn throughout the term of the policy will be 6% p.a. or 10% p.a., as the case may be. The Projected Investment Rate of Return is not guaranteed. The main objective of the illustration is that the client is able to appreciate the features of the product and the flow of benefits in different circumstances with some level of quantification. Future bonus will depend on future profits and as such is not guaranteed. However, once bonus is declared in any year and added to the policy, the bonus so added is guaranteed. Intro features benefits illustrations