Download

1 / 7

80 likes | 208 Views

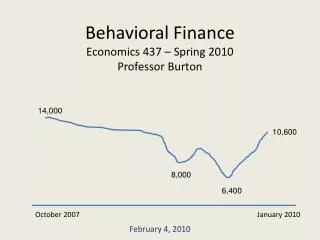

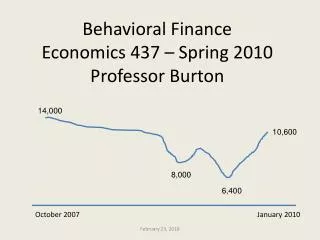

Behavioral Finance Economics 437 – Spring 2009 Professor Burton. March 2008 January 2009. Significance of Shleifer Etal Article.

E N D

Behavioral FinanceEconomics 437 – Spring 2009Professor Burton March 2008 January 2009 January 27, 2009

Significance of Shleifer Etal Article • Two assets were identical according to finance theory: both had certain dividend, r each period • One asset fungible into consumption good; that fixes the prices at 1 (using the consumption good as the money unit) • Noise trader is same as arbitrage trader except he is too optimistic (pessimistic) randomly about the future price of the risky asset January 27, 2009

So, what has Shleifer captured • Noise traders can make more money than arbitrageurs • Limits to arbitrage: arbitrageurs worried that overpricing (underpricing might get worse) • No fundamental difference between the assets January 27, 2009

Abreu – BrunnermeierBubbles and CrashesEconometrica, 2003 • What happens when a price starts growing faster than the “correct” price? Actual price Correct price time January 27, 2009

What Happens in Abreu-Brunnermeier? • Price diverges from “correct” price (no one knows why) • Then, sequentially, arbitrageurs gradually realize the price is above the “correct” price • But they keep buying (because others don’t know yet) • Only when a fraction, κ, of all traders realize the price is wrong does the bubble burst. January 27, 2009

Why would the smart guys buy stock when they know it is overpriced? • Because they might be money managers who are compared to the averages. • They might rationally anticipate the “greater fool” who hasn’t yet figured out what they know. January 27, 2009

The End January 27, 2009