Download

1 / 12

130 likes | 382 Views

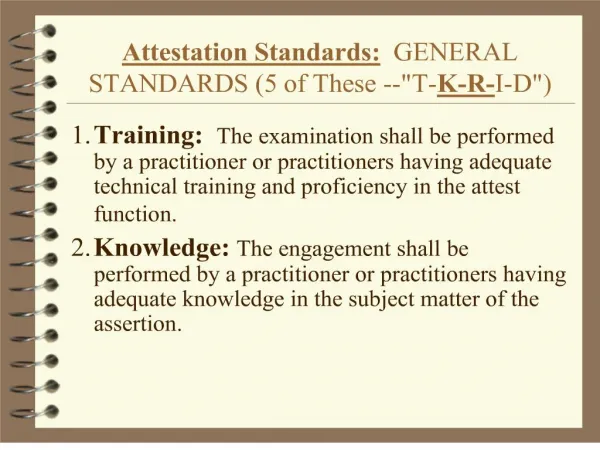

Statements on Standards for Attestation Engagements. Clarifying the Attestation Standards. Commonly known as attestation standards Apply to engagements that address subject matter other than historical financial statements , e.g : an entity’s compliance with laws or regulations

E N D

Clarifying the Attestation Standards • Commonly known as attestation standards • Apply to engagements that address subject matter other than historical financial statements, e.g: • an entity’s compliance with laws or regulations • the effectiveness of an entity’s controls over the privacy of information • a financial forecast • Address examination, review and agreed-upon procedures (AUP) engagements

Clarifying the Attestation Standards • 4 “general” AT sections that provide a framework for developing an attestation engagement • AT 20, Defining Professional Requirements in Statements on Standards for Attestation Engagements • AT 50, SSAE Hierarchy • AT 101, Attest Engagements (which addresses examination and review engagements) • AT 201, Agreed-Upon Procedures Engagements

Clarifying the Attestation Standards • Currently: 6 “topic-specific” AT sections for reporting on • prospective financial information (AT 301) • pro forma financial information (AT 401) • internal control over financial reporting (AT 501) • compliance with laws and regulations (AT 601) • management’s discussion and analysis (AT 701) • controls at service organizations (AT 801)

Clarifying the Attestation Standards • Objective: to make AT sections easier to read, understand and apply • Redraft in clarity format • New structure (objective is to eliminate repetition) • Chapter 1: Concepts common to all attestation engagements • Chapters 2-4: Levels of service (examination, review, agreed-upon procedures). • Each chapter addresses a specific level of service and builds on the common concepts chapter • Subject-matter specific chapters • Each chapter builds on common concepts and level of service chapters

Clarifying the Attestation Standards • Example – Reporting on an examination of prospective financial information • Currently, the following AT sections apply: • AT 20 • AT 50 • AT 401 • Proposed structure, the following sections would apply: • Chapter 1, Common Concepts • Chapter 2, Examinations • Chapter X, Forecasts

Clarifying the Attestation Standards • Convergence with standards of the International Audit and Assurance Standards Board (IAASB) • Foundation for the common concepts, examination, and review sections of the proposed attestation standards: • AICPA’s existing attestation standards • IAASB International Standards on Assurance Engagements (ISAE) 3000, “Assurance Engagements Other than Audits or Reviews of Historical Financial Information” (Dec 2013) • ISAE 3000 is IAASB’s framework standard for assurance engagements (equivalent of attestation engagements) • ISAE 3410, Assurance Engagements on Greenhouse Gas Emissions

Clarifying the Attestation Standards • Convergence with standards of the International Audit and Assurance Standards Board (IAASB) • AT 801 was converged with ISAE 3402, Assurance Reports on Controls at a Service Organization, when SSAE No. 16, Reporting on Controls at a Service Organization,was issued in April 2010 • Proposed “Reporting on Pro Forma Financial Information,” includes elements of ISAE 3420, Assurance Engagements to Report on the Compilation of Pro Forma Financial Information Included in a Prospectus

Clarifying the Attestation Standards • July 2013, the ASB issued an exposure draft of the first four “chapters” • Common Concepts • Examinations • Reviews • Agreed-upon Procedures • January 2014, the ASB issued an exposure draft of the following subject-specific chapters: • Financial Forecasts and Projections • Reporting on Pro Forma Financial Information • Compliance Attestation

Clarifying the Attestation Standards • AT 801 exposure vote on July 2014 ASB agenda • Reporting on Controls at Service Organization • Delayed to include guidance from AAG • One section not being clarified: • Management’s Discussion and Analysis (AT 701) • Will remain unclarified • One section moving and being replaced • An Examination of an Entity’s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements (AT 501) • Will be moved to auditing standards • Will be replaced by generic AT 501 examination standard on internal control

Clarifying the Attestation Standards • Final clarified SSAE will contain all attestation standards • One SSAE (SSAE No. 18) even though more than one exposure draft • Expected issuance in second half of 2015 (estimate) • Proposed effective date (estimate): • No earlier than for reports dated December 15, 2015

Clarifying the Attestation Standards • Exposure drafts http://www.aicpa.org/Research/ExposureDrafts/AccountingandAuditing/Pages/ExposureDrafts_ASB.aspx • More information Dedicated ASB Attest Clarity page on AICPA Website at http://www.aicpa.org/InterestAreas/FRC/AuditAttest/Pages/AttestClarityProject.aspx