Download

1 / 12

120 likes | 145 Views

Learn about breakeven analysis and how it can help engineers understand the impact of their projects on profitability. This presentation covers concepts such as fixed costs, variable costs, revenue, and the breakeven volume. Discover the value of engineers to the company through understanding breakeven analysis.

E N D

Breakeven AnalysisPart 1Click here for Streaming Audio To Accompany Presentation (optional) EGR 403 Capital Allocation Theory Dr. Phillip R. Rosenkrantz Industrial & Manufacturing Engineering Department Cal Poly Pomona

EGR 403 - The Big Picture • Framework: Accounting& Breakeven Analysis • “Time-value of money” concepts - Ch. 3, 4 • Analysis methods • Ch. 5 - Present Worth • Ch. 6 - Annual Worth • Ch. 7, 8 - Rate of Return (incremental analysis) • Ch. 9 - Benefit Cost Ratio & other techniques • Refining the analysis • Ch. 10, 11 - Depreciation & Taxes • Ch. 12 - Replacement Analysis EGR 403 - Cal Poly Pomona - SV3

Introduction • Break even (BE) analysis helps engineers understand the “big picture” • Knowing how your project or assignment affects profitability can help you sell your projects to upper management • Understanding BE analysis illustrates the value of engineers to the company EGR 403 - Cal Poly Pomona - SV3

Recall from the P & L Statement • Fixed costs - do not vary (e.g., lease costs, rent, insurance) • Variable costs - vary with volume of production (e.g., labor, materials, supplies, rent, etc.) Overhead can also be applied here as a variable expense or burden rate. • Profit Equation - Profit = Revenue - Expenses EGR 403 - Cal Poly Pomona - SV3

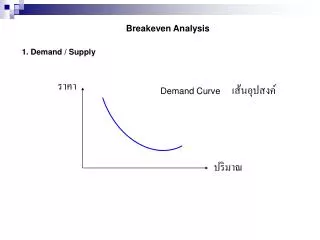

Breakeven Volume • Total Variable Cost (VC) is a function of volume (x) of units sold. Total VC = Variable Cost/unit * x • Total Cost = Fixed Cost + Total VC • Revenue is also a function of units sold: Revenue = Price/unit * x • Breakeven Volume is the number of units you need to sell so that: Revenue = Total Cost EGR 403 - Cal Poly Pomona - SV3

Breakeven Volume (cont’d) • Find x such that: Price/unit * x = Fixed + VC/unit * x • Therefore: xBE = Fixed Cost / (Price/unit - VC/unit) • If actual volume is < xBE , you have a loss • If actual volume is > xBE , you have a profit EGR 403 - Cal Poly Pomona - SV3

Fixed CostFixed cost is the the same, regardless of volume EGR 403 - Cal Poly Pomona - SV3

Variable Cost + Fixed CostTotal Cost goes up with volume because Variable Cost increases EGR 403 - Cal Poly Pomona - SV3

Total Revenue is based on volume and selling price/unit.Where the Revenue and Total Cost lines intersect is the Break Even (BE) Point. That volume is the BE Volume EGR 403 - Cal Poly Pomona - SV3

ProfitAbove the BE point, the difference between the Revenue and Total Cost lines represents profit EGR 403 - Cal Poly Pomona - SV3

LossIf volume is below the BE point, the difference between the lines represents a loss EGR 403 - Cal Poly Pomona - SV3

Break Even Analysis • Collect financial and cost information to determine fixed and variable costs • Fixed costs • Variable cost/unit (labor, materials, overhead) • Estimate Selling Price per unit from marketing analysis and market testing • Determine BE volume and compare to estimated sales • If estimated sales volume is not above the BE volume, make adjustments EGR 403 - Cal Poly Pomona - SV3