Download

1 / 18

210 likes | 620 Views

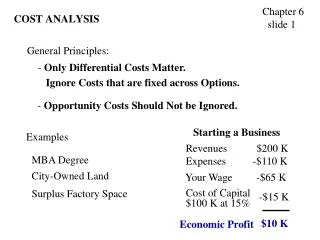

Cost Analysis. Control costs Improve cost structure – problems show up Cost structure – relative proportion of each type of cost – fixed, variable, mixed Improve effectiveness of firm Which costs eroding profit margin What first? – earnings decrease Analyze situation, target problem areas.

E N D

1 Cost Analysis • Control costs • Improve cost structure – problems show up • Cost structure – relative proportion of each type of cost – fixed, variable, mixed • Improve effectiveness of firm • Which costs eroding profit margin • What first? – earnings decrease • Analyze situation, target problem areas

2 • Cost behavior – • Fixed – remain constant – i.e. equipment • Variable – dollar amount varies in direct proportion to changes in activity level – i.e. Battery in car • Mixed – contains both variable and fixed elements – license fee of $25,000/year and $3/dinner party • Stepped costs – variable but increases in big chunks – i.e. Wages of maintenance workers

3 • Make sure that costing done correctly, reduce costs • Standard costing – assigning overhead costs based upon one predetermined rate based on volume • Activity based costing - designed to provide managers with cost information for strategic and other decisions that potentially affect capacity and therefore affect fixed as well as variable costs. • Most organizations maintain two costing systems – internal – most useful information. • Uses drivers at various levels

8 Activity Based Costing • Two stage allocation process • Assign costs to pools, then assign to products using cost drivers • I.e. Sell 50,000 CD units, 200,000 tape units = 250,000 units total • Both require two direct labor hours to complete = 500,000 direct labor-hours • Total manufacturing overhead = $10,000,000

9 Traditional Costing Method

10 ABC Costing

12 • Full capacity – constrained resource? • Constraint – limited resource that could restrict company’s ability to satisfy demand – how used • Theory of constraints • Should not necessarily promote products with highest CM but rather promote the product with the highest contribution margin per unit of constrained resource

13 • Value chain analysis – major business functions that add value to product and/or service • Eliminate or minimize non-value activities • Value-added activities – efficient as possible • Design in quality – reduce rework or scrap • Costs of quality • Prevention costs – plan the process to ensure that defects do not occur • Appraisal costs – measure the level of quality to insure customer requirements • Internal failure costs – rectify defective output before reaches customer • External failure costs – costs associated with delivering defective output to customer

14 • Effectiveness ratios • Inventory turnover = COGS/average inventory – how frequently sells inventory • JIT inventory system • Lower costs by long-term contracts • Closer relationship w/suppliers – guarantee deliver • Reduce scrap by increasing quality • Obsolete inventory on hand? • A/R turnover – Credit sales/average accounts receivable – ability to collect cash from credit customers • What is working? • Reduce operating cycle – need less working capital – invest in more productive activities

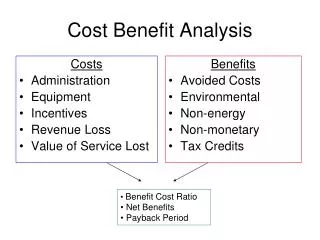

15 • Gross margin covers all costs - customers • 80/20 rule – 80% of headaches come from 20% of customers – how to find them? • Customer profitability – no problems • Find all costs – product fulfillment cycle • Some customers require extra work • Extra sales calls, customer service, smaller transportation lots, smaller orders – all add to costs • Expend effort on customers that are most profitable • Drop services that don’t increase goodwill or profitable

16 • Operating leverage – increase profitability • Multiplying force – how sensitive is net operating income to percentage change in sales, if high a small percentage increase in sales can produce a much larger percentage increase in net operating income • Mix of fixed versus variable costs • Capital intensive vs. labor intensive • Leverage multiplier - CM/NI

18 • Download • Capital budgeting spreadsheet • Theory of constraints • Capital budgeting problems • Read Introduction to ABC Costing • Read internal control process • Read Survey Masters LLC • Assign #3 – ABC Costing/unit problem (due 2/2) • Assign #4 – profitability ratios (due 2/2) • Gross margin % - 07-05 • Profit margin – 07-05 • Return on Assets – 07-05 • Return on Equity - 07-05