Download

1 / 3

30 likes | 115 Views

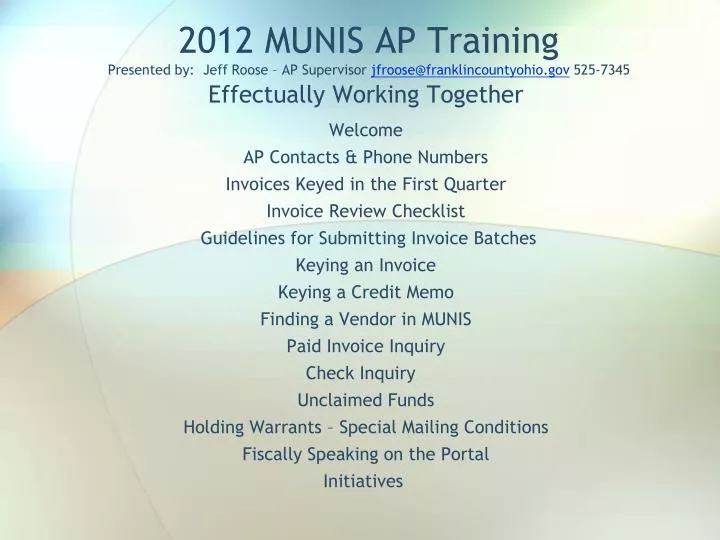

2012 MUNIS AP Training Presented by: Jeff Roose – AP Supervisor jfroose@franklincountyohio.gov 525-7345 . Effectually Working Together

E N D

2012 MUNIS AP TrainingPresented by: Jeff Roose – AP Supervisor jfroose@franklincountyohio.gov 525-7345 Effectually Working Together WelcomeAP Contacts & Phone NumbersInvoices Keyed in the First QuarterInvoice Review Checklist Guidelines for Submitting Invoice Batches Keying an InvoiceKeying a Credit MemoFinding a Vendor in MUNISPaid Invoice InquiryCheck Inquiry Unclaimed FundsHolding Warrants – Special Mailing ConditionsFiscally Speaking on the PortalInitiatives

The Auditor’s Role and Relationship Accounts Payable Responsibilities: Pursuant to Ohio Revised Code 319.16, warrants shall be issued upon presentation of the proper order or voucher and evidentiary matter for the moneys, and record kept of all such warrants showing the number, date of issue, amount for which drawn, in whose favor, for what purpose, and on what fund. If the validity of an expenditure is questioned, the agency who presented the voucher shall be notified. Regrettably, from time to time, it will be necessary for us to return an invoice or batch back for correction. Please don’t take it personally! It is our responsibility to safeguard you and your agency as the last line of defense before payment is completed. Auditing: We base our internal reviewing practices on recommendations & bulletins from the Ohio Auditor of State (AOS), opinions of the Ohio Attorney General, the Ohio Revised & Administrative Code, and applicable Federal, State or Local regulations. Invoices presented for payment that do not obey established policy, list vague line-item detail, or which may be misconstrued as not having Proper Public Purpose may be returned for clarification. Supporting Language: Invoices that are guaranteed by contract, resolution or grant must include the following signed and dated verbiage if they are not itemized: “I certify that the claims made to (AGENCY) for payment of purchased services are for actual services rendered for eligible and allowable program activities. The supporting documentation associated with this payment request, is being stored at our office and shall be made available for audit if required.” Findings for Recovery Impact: If the Auditor of State determines that taxpayer funds were spent inappropriately or incorrectly, those monies may be recovered wholly or independently; meaning reimbursement to the State may be required from everyone who contributed in the comprehensive record of payment.