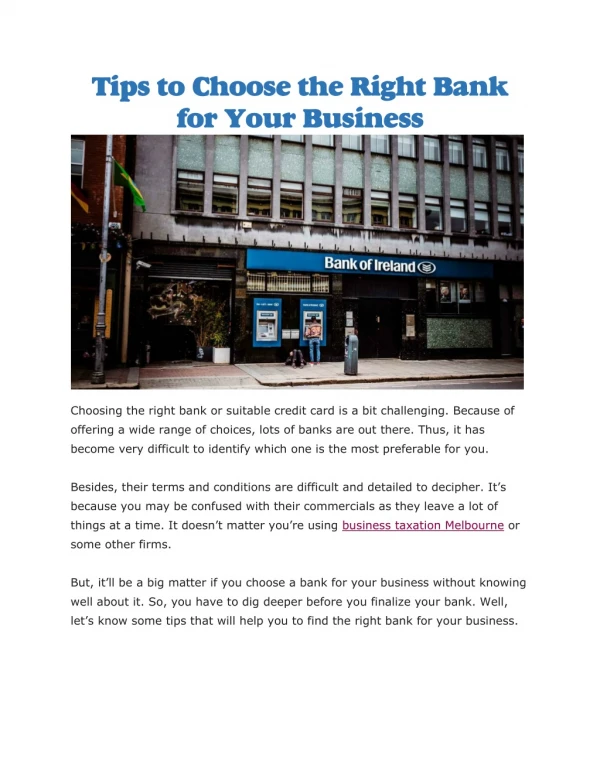

Download

1 / 28

280 likes | 489 Views

Taxation and Incentives in the Business Enterprise. Research Project on “Enterprise Law as a Structure for Incentives”. By: David Gamage Assistant Professor, UC Berkeley (Boalt Hall) School of Law . Outline. -- What Does Research Tell Us About the Incentive Effects of Taxation?.

E N D

Taxation and Incentives in the Business Enterprise Research Project on “Enterprise Law as a Structure for Incentives” By: David Gamage Assistant Professor, UC Berkeley (Boalt Hall) School of Law

Outline -- What Does Research Tell Us About the Incentive Effects of Taxation? -- How do Human and Monetary Capital Providers Respond to Taxation? -- How Should the Government Tax the Business Enterprise?

Measuring Incentive Effects: Elasticities • Elasticities are measurements of responses to taxation Elasticity = percent change in behavior divided by percent change in price • Uncompensated elasticities include both an income effect and a substitution effect • Compensated elasticities include only a substitution effect • Public Finance Theory says that compensated elasticities are a better measure of excess burden

Elasticities of Income Taxation • Measured labor supply elasticities are low Elasticities of hours worked for men are near zero Labor force participation elasticities for men are higher, but sill very low Elasticities for married women are considerably higher than for men, but are still only moderate and are converging over time • Taxable Income Elasticities are considerably higher Median estimates are around 0.4 Most studies find much higher elasticities for high income taxpayers than for low income taxpayers

What Does an Elasticity of .4 Mean? • Elasticity of Taxable Income equals the percentage change in reported taxable income associated with a one-percent increase in the net-of-tax rate, where the net-of-tax rate equals one minus the marginal tax rate • So, if the current tax rate is 10%, the effect on reported taxable income of raising the tax rate to 11% would be: • The net-of-tax-rate would decrease from 90% to 89%, making a 1.11% decrease in the net-of-tax rate (1/90). • Hence, the percentage decrease in reported taxable income would be: 0.4 times 1.11%, or, 0.444%.

The Gap Between the Measures Factors that could explain the gap: • Tax evasion and avoidance • Tax deferral and tax shifting • Work effort Only work effort would have the same social welfare implications as labor supply distortions under the standard models. Tax deferral and shifting do not represent excess burden (except for transaction costs). Avoidance and evasion are more complicated.

Avoidance and Evasion: Question 1 Do avoidance and evasion responses create the same excess burden as labor/leisure responses? The standard answer assumes yes (Feldstein 99) --taxpayers will avoid/evade until the costs of doing so equal the costs of the tax dollars saved --assumes increasing costs of avoidance/evasion But there is an argument for no(Chetty 2008) --some of the private costs of avoidance/evasion may not be social costs

Avoidance and Evasion: Question 2 Do avoidance and evasion responses have the same policy implications as labor/leisure responses? Under standard models based on labor/leisure distortions, two important results can be derived: • Production Efficiency (Diamond-Mirrlees 1971) • Non-Differential Commodity Taxation (Atkinson-Stiglitz 1976) I argue that neither of these results necessarily applies to tax avoidance/evasion distortions (Gamage, work-in progress).

Avoidance and Evasion: Question 2 cont. • Under the standard models – with production efficiency and non-differential commodity taxation – it is hard to justify taxing the business enterprise (except for withholding and pass-through regimes). -In general, there should only be a comprehensive personal income tax • But if evasion/avoidance are important, and if my result holds, enterprise taxation may be desirable. -By raising revenue from enterprise taxation, income tax rates can be reduced.

Hierarchy of Adjustments • In general, taxpayers will respond to taxes: • First, with deferral and tax shifting; • Second, with avoidance and evasion; and, • Third, with “real responses.” • (Slemrod 1996) Without comprehensive tax systems, we may not ever observe significant real responses. The extent of deferral, tax shifting, avoidance, and evasion will depend on the design of the tax system.

Caveats • Most studies can only measure short-term responses to tax changes. Long-term effects may be stronger or weaker. The welfare consequences of avoidance and evasion depend on the cost functions for engaging in these responses. Government policy partially determines the elasticities for deferral, tax shifting, avoidance, and evasion; and thereby partially determines the elasticities of real responses.

Summary of Section • Under the standard models based on “real responses,” it is hard to justify taxing the business enterprise. However, the “real responses” that underlie these standard models may be considerably less important than avoidance and evasion responses. If avoidance and evasion responses are important, it may be desirable to tax the business enterprise.

Outline -- What Does Research Tell Us About the Incentive Effects of Taxation? -- How do Human and Monetary Capital Providers Respond to Taxation? -- How Should the Government Tax the Business Enterprise?

I. Managers (1 of 2) • Managers seek to maximize: • 1) Their monetary compensation; • 2) Their non-monetary compensation (e.g., fringe benefits); and, • 3) (perhaps also,) Their work-related power and status. Monetary compensation is usually taxed, non-monetary compensation can often go untaxed, and work-related power and status is rarely taxed.

I. Managers (2 of 2) Managers are likely to respond to taxation by shifting from (taxable) monetary compensation to (nontaxable) non-monetary compensation and work-related power and status. Managers are also likely to use deferral, tax shifting (conversion), and avoidance to minimize their tax liabilities. E.g., conversion of income to capital gains through incentive compensation; negotiating custom non-taxable fringe benefit packages.

II. Employees (1 of 1) • Like managers, employees seek to maximize: • 1) Their monetary compensation; • 2) Their non-monetary compensation (e.g., fringe benefits); and, • 3) (perhaps also,) Their work-related power and status. Employees will use similar strategies as managers, but have less flexibility as must often take standardized contracts rather than negotiating custom contracts.

I & II. Managers and Employees (1 of 1) • It is unclear how managers and employees are affected by business level taxes: • -It is unclear how these taxes affect take home pay. • -If the taxes encourage retained earnings, may facilitate managerial empire building. • -But the recordkeeping requirements of a business tax may facilitate stronger corporate governance. The incidence of business-level taxes is ambiguous, and may differ among countries (depending on the countries’ competitive positions).

III. Shareholders and Creditors (1 of 2) The project separates shareholders and creditors, but for tax law analysis, it is important to realize that there is not a clear distinction between them. Two distinctions are usually cited: (1) share of upside gains v. protection from downside risk; (2) degree of control. But numerous hybrid instruments have been created blurring these distinctions. And the higher the debt to equity ratio, the more debt begins to look like equity. It may be more accurate to think of creditors and shareholders as falling on a continuum, rather than being two distinct categories.

III. Shareholders and Creditors (2 of 2) • If shareholders and creditors are taxed differently (as in the U.S. corporate tax), there will be strong incentives for transactions to be characterized as falling in the tax-favored category. • Both shareholders and creditors will generally seek to avoid realization events. May encourage retained earnings and managerial empire building. • Shareholders and creditors may benefit from auditing and validating functions of tax law, as these may help to hold managers accountable.

Outline -- What Does Research Tell Us About the Incentive Effects of Taxation? -- How do Human and Monetary Capital Providers Respond to Taxation? -- How Should the Government Tax the Business Enterprise?

Models of Government Behavior (1 of 2) • Leviathan Model -Government as tax maximizer -Model does not account for the fact that government is composed of individual agents, few of which benefit directly from higher revenues -Model may be most descriptive when governing power is both centralized and stable -The ideology of the governing party is also important

Models of Government Behavior (2 of 2) • Beneficial Dictator Model -Government as social welfare maximizer -Model does not account for public choice motives of government actors -However, we should not assume the model has no descriptive power • Interest Group Bargaining Model -Broad public opinion governs for highly salient issues, narrow interest groups win for less salient issues -Most tax issues are narrow and less salient

Principles of Efficient Taxation • MinimizeExcess Burden • Promote Socially Desirable Redistribution • Deter Negative Externalities / Promote Positive Externalities • Enact Countercyclical Fiscal Stimulus

Countercyclical Fiscal Stimulus Can enterprise taxation enact countercyclical fiscal stimulus? • Shift timing of investment decisions --temporary tax breaks during downturns (e.g., accelerated depreciation, investment tax credits) --promised tax increases in the future --temporary extension of non-recognition rules for investment decisions

Negative and Positive Externalities Can enterprise taxation serve pigouvian ends? • Standard pigouvian taxes can be implemented through enterprise taxation --e.g., carbon tax penalties • The prospect for enterprise-specific pigouvian taxes is more ambiguous --Can taxation reduce collective action problems among human capital providers and monetary capital providers? --How does enterprise taxation interact with the goals of non-tax enterprise law? --e.g., Tobin taxes

Socially Desirable Redistribution Can enterprise taxation enact socially desirable redistribution? • Definition of Socially Desirable Redistribution --individual and social welfare functions --“redistribution” is a loaded term • Incidence of enterprise taxation is unknown --open v. closed economies • Desirability of taxing capital is unclear --Atkinson-Stiglitz & Chamley-Judd --Impact of avoidance and evasion

Minimize Excess Burden How can enterprise taxation raise revenue while creating the minimum possible excess burden? • Tax inelastic decisions --tax advantage of frictions between parties --But must avoid overtaxing these decisions or might foster an infrastructure of avoidance • Broad, comprehensive base is often best approach --Except where multiple taxes can lead to reduced tax rates on multiple decision-making margins

Outline -- What Does Research Tell Us About the Incentive Effects of Taxation? -- How do Human and Monetary Capital Providers Respond to Taxation? -- How Should the Government Tax the Business Enterprise?