Download

1 / 23

230 likes | 363 Views

School Property Tax Relief in Wisconsin Association for Equity in Funding Milwaukee, January 19, 2012. Andrew Reschovsky Professor of Public Affairs and Applied Economics Robert M. La Follette School of Public Affairs University of Wisconsin-Madison. Outline.

E N D

School Property Tax Relief in WisconsinAssociation for Equity in FundingMilwaukee, January 19, 2012 Andrew Reschovsky Professor of Public Affairs and Applied Economics Robert M. La Follette School of Public Affairs University of Wisconsin-Madison

Outline • Analysis of the School Levy Credit and the First Dollar Credit • Assessing other kinds of property tax relief • Revenue caps and levy limits • Circuit Breakers—the homestead credit • Equitable school funding and effective property tax relief

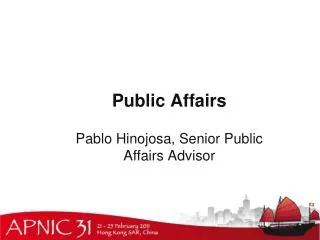

Percentage Change in Inflation-Adjusted Componentsof State Support for Public Education, 2008 to 2013

Analyzing the School Levy Credit • Credit is allocated to municipalities in proportion to their share of the statewide school property tax levy • Property wealthy municipalities generally have higher property tax levies and hence get larger credits • Within a municipality, each taxpayer’s credit is equal to her share of total municipal assessed property value • Those with more valuable property tend to have higher incomes and lower property tax burdens

Who Benefits from the School Levy Credit? • 71% of residential property tax revenue is paid by Wisconsin homeowners on their principle residence • This means that only 51% of the School Levy Credit provides tax relief to WI homeowners on their principle residence • About 26% of credit goes to owners of non-residential property (many of them non-residents) and non-resident owners of vacation property in Wisconsin • Average credit ~ 16% of property tax levy

First Dollar Credit • Credit goes to all improved parcels • Credit = school mill rate x credit base (first $X of assessed value) • $X determined each year by the total dollar amount allocated to the First Dollar Credit • In 2010(11) credit base = $6,900; average credit = $67 • Credit as a % of levy higher for low-value property

Tony Evers Proposal to End theSchool Levy Credit • Proposal: Use the money now allocated to the SLC for equalization aid • Analysis: As long as the revenue cap remains unchanged, any additional aid will translate into property tax relief • The taxpayers who benefit the most from the reform proposal will be different than those that benefit from the SLC, but in the end total property tax relief and total school revenues will remain unchanged

Criteria by Which to JudgeProperty Tax Relief Policies • Tax relief measures should not interfere with the freedom of elected local officials to determine the level of property taxation within their community • Relief measures should do nothing to limit or distort the essence of the property tax as a tax on the market value of property • Property tax relief should be targeted to taxpayers for whom the property tax causes substantial economic hardship

Assessing Property Tax Reliefin Wisconsin • School revenue caps and county and municipal levy limits reduce local control • They provide untargeted property tax relief by forcing reductions in mill rates • These limits take no account of variations across communities in the “costs” of providing public services • The effect is inadvertently to create tighter limits in the places facing higher costs, e.g. more low-income students to educate

Assessing Property Tax Reliefin Wisconsin (cont.) • Targeted property tax relief only through the Homestead Credit • 2009-10, $129.2 mil. to 76,200 claimants • Total credit = 1.4% of total property tax levy • Maximum credit = $1,184; maximum income for eligibility=$24,500 • DOR estimated that only 43% of eligible taxpayers received the credit

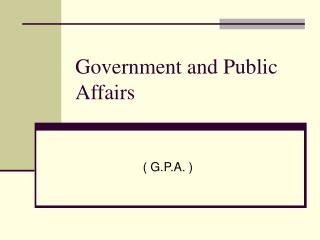

Gross and Net Property Tax BurdensWisconsin Homeowners, 2005

Number of Wisconsin School Districts That Took Following Actions This Year Wisconsin Assoc. of School Boards Survey (Nov. 2011)

Number of Wisconsin School Districts Expectations About Next Year’s Cuts Wisconsin Assoc. of School Boards Survey (Nov. 2011)

Fiscal Equalization Among K-12 School Districts, 2010-11Success in Achieving Access Equality and Spending Equalization