Download

1 / 10

130 likes | 383 Views

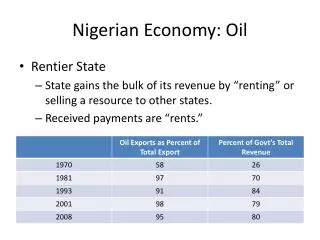

NIGERIAN NATIONAL PETROLEUM CORPORATION NIGERIAN CONTENT DEVELOPMENT JOURNEY. April 2010. Nigerian Content Implementation Model Current Status – Projections . Capacity limitations. No legal backing. Performance Risk for sole regulation-based implementation . Policy Target.

E N D

NIGERIAN NATIONAL PETROLEUM CORPORATIONNIGERIAN CONTENT DEVELOPMENT JOURNEY April 2010

Nigerian Content Implementation Model Current Status – Projections Capacity limitations. No legal backing Performance Risk for sole regulation-based implementation Policy Target Growth from NOC injection of operations focus • The major factor for NC growth between 2005 to 2010 is the injection of operations focus to NC implementation • Absence of legal backing to enforce compliance and limitations of critical capacity militated against higher performance • ACT provides impetus to add enforcement to Collaboration required to build local Capacity

Up to 2004 2004 -2010 2010-2015 95% Goods and Services Imported 65% import 20 - 30% import Shipyards Heavy industries Pipe Mills Equipment manufacturing Service Coys Training Institute Vessel Ownership R & D institutes 35% Nigerian Content Implementation Model Impact Of The Act On Local Capacity 5% locally Very low local capacity Improved Capacity Capacity gap Biz Opportunity

Nigerian Content Implementation Model Lessons learnt – Focus areas OPCO Performance Linked To Service Companies& Suppliers Over 60% Performed By Foreign Service Companies Local Capacity Building Will Improve Cost Effectiveness And Certainty Of Supply Deliberate Biz Strategy Needed To Build Capacity backed by Legislation

Nigerian Content Implementation ModelCurrent industry Compliance readiness for Schedule A of the Bill The wide capacity gap is a recipe for waiver-driven compliance

Nigerian Content Implementation Model IMPENDING OIL & GAS LEGISLATIONS PIB NC BILL

Nigerian Content Implementation ModelHighlights of the Nigerian Content Bill • Establishes a new body NCMB outside NNPC • Sets out specific targets for NC scope in all activities under schedule A of the ACT • 50% of Multi national coy Assets to be vested in Nigerian subsidiary • Nigerian indigenous company defined to be 51% owned by indigenes. • Indigenous Companies have first consideration for licenses, Oil blocks, Contracts • Indigenous companies have exclusivity on land and swamp activities • Creates Opportunities for Indigene’s employment and training • Changes to Schedule A Targets can only be effected through NASS • Power of the Minister to approve 3-year waiver for areas of insufficient capacity • Minister to make regulations • Fines for non-compliance

Nigerian Content Implementation ModelRegulator – Operator Roles Schematic Industry Activity Goal Collaboration is still key

Concluding Remarks • NNPC has responded to the National call to domicile significant portion of Oil &Gas derivatives • A robust foundation Has been Built • ACT provides unprecedented opportunity to create new business both in NNPC and Local Service companies from capacity building scope • Industry must continue to work together under the leadership of the board to achieve desired targets • Thank you