Download

1 / 22

220 likes | 363 Views

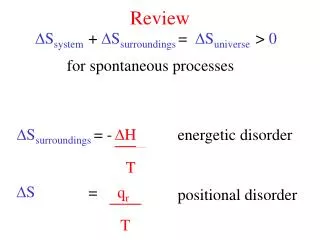

Review. FINA 7330 Advanced Corporate Finance Lecture 13 Ronald F. Singer Fall, 2009. Making Investment Decisions. NPV Rule Incremental Cash Flow After Tax basis when paid Opportunity Costs Changes in Working Capital Depreciation Not a Cash Flow Treat Inflation Consistently

E N D

Review FINA 7330 Advanced Corporate Finance Lecture 13 Ronald F. Singer Fall, 2009

Making Investment Decisions • NPV Rule • Incremental Cash Flow • After Tax basis when paid • Opportunity Costs • Changes in Working Capital • Depreciation Not a Cash Flow • Treat Inflation Consistently • MAXIMIZE NPV

Practical Problems in Capital Budgeting • Basically: What happens when you cannot take all positive NPV projects. • Must Consider the package of projects which maximizes the NPV of all possible alternatives • Classes: • Two possibilities • Once and for all deals • Repetitive deals

Once and for all deals Mutually Exclusive Projects: Basically dealing with mutually exclusive decisions • Mutually Exclusive Projects • Beware of the conflicts between IRR and NPV • Investment Timing: When is the optimal time to take on a project: (Want to max the Present value of the NPV) • Budget Constraints: What subset of all possible combinations give you the highest NPV

Repetitive Deals • Mutually Exclusive projects with different starting times, economic lives • Replacement Decision In general, you “smooth” the cash flows by finding Equivalent Annual Cash Flow, so that projects can be compared.

Repetitive Deals • Mutually Exclusive projects with different starting times, economic lives • Equivalent Annual Cash Flow • Replacement Decision • Replace when • EACF replacement > EACF existing

Analysis of Projects • Sensitivity Analysis • Scenario Analysis • Break Even Analysis • Monte Carlo Simulations • Real Options and Decision Trees • React to ongoing information as it is revealed

Strategic Investment Decisions • Trust Market Values • Look for comparative advantage • Consider opportunity costs • How will introducing this project effect other products you produce • When will introduction of this project induce competition • What will happen to the price over time

Payout Policy • Critical Dates • Announcement Date • Record Date • Payment Date • Ex-dividend Date

Payout Policy • Dividends versus repurchase of shares • Signaling implications of announcements • Agency Costs • Free Cash Flow • Tax implications • Liquidity

Lintner’s Model • DDiv(t) = a(Div(t)*-Div(t-1)) Where the dividend target (Div(t)*) is determined as a proportion of long run earnings

Payout Policy • What investors do • What firms do • What effect does dividend policy have on price

Empirical Payout Policy • Repurchases versus Dividends • Signals • Fixed price tenders versus open market purchases • High market/book versus low market/book • What does market/book tell you • What do you expect the reaction in these 2 cases to be • Repurchase versus Dividends

Long-Run Policy • Tax Effects • Free Cash Flow

Dividend Policy • What should corp. do? • What should individual do? • What is the impact on the total value of the firm

Agency Problems • How do you induce managers to act in stockholders’ interest

Message of EVA + Managers are motivated to only invest in projects that earn more than they cost. + EVA makes cost of capital visible to managers. + Leads to a reduction in assets employed. - EVA does not measure present value • Rewards quick paybacks and ignores time value of money + Present Value of EVA does measure NPV and thus consistent rewarding via EVA leads to good decisions

Capital Structure • Capital Structure Defined • The Modigliani Miller Theory • Static Tradeoff Theory • Taxes • Bankruptcy costs and costs of financial distress • Information costs • Pecking Order Theory

Capital Structure • Agency Problems • Underinvestment • Overinvestment (risk shifting)

Raising Capital • Information and how capital is raised • Debt versus equity • Cash flow in versus cash flow out • Organizational changes • Transactions that increase ownership concentration increase stock prices • Underwritten versus Rights offering • Greater Commitment by underwriter has positive impact on stock price

Summary • Leverage Increasing (+Price Reaction) • Cash Flow In (+Price Reaction) • Underwritten versus Rights Offering (less underpricing) • Firm Commitment versus Best Efforts • Negotiated versus Competitive Bid for underwriter • Traditional Registration versus Shelf Registration • Organizational Structure (Price reaction) • Increasing concentration of ownership • Voluntary Reorganization

Advent of “innovative securities” • Inefficient markets • Incomplete markets • Resolves conflicts of interest • Tax or regulatory arbitrage • Encourage efficient production