Download

1 / 9

90 likes | 243 Views

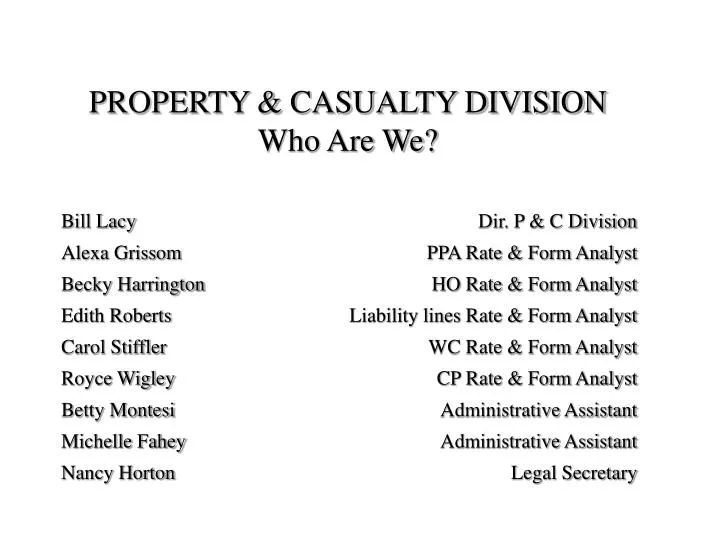

PROPERTY & CASUALTY DIVISION Who Are We? Bill Lacy Dir. P & C Division Alexa Grissom PPA Rate & Form Analyst Becky Harrington HO Rate & Form Analyst Edith Roberts Liability lines Rate & Form Analyst Carol Stiffler WC Rate & Form Analyst Royce Wigley CP Rate & Form Analyst

E N D

PROPERTY & CASUALTY DIVISION Who Are We? Bill Lacy Dir. P & C Division Alexa Grissom PPA Rate & Form Analyst Becky Harrington HO Rate & Form Analyst Edith Roberts Liability lines Rate & Form Analyst Carol Stiffler WC Rate & Form Analyst Royce Wigley CP Rate & Form Analyst Betty Montesi Administrative Assistant Michelle Fahey Administrative Assistant Nancy Horton Legal Secretary

What the Property & Casualty Division Does: Reviews all insurance rates for homeowners, private passenger automobile, workers compensation and professional liability Reviews all forms for virtually all insurance policies sold to Arkansans for personal and commercial property & casualty coverages Rate review: file and use with 20 day deemer Form review: prior approval with 30 day deemer Filings are received on paper and over the internet (The System for Electronic Rate and Form Filings, or “SERFF”) We handle over 4,000 separate filings each year Those filings contain over 25,000 rates and forms that must be reviewed Each Analysts, on average, reviews approximately 4 filings each working day In any give month, between 33% to 44% of filings are made through SERFF

What the Property & Casualty Division Does: Oversight responsibility for Arkansas’: Earthquake MAP plan Arkansas Rural Risk Underwriting Association – provides homeowners coverages for properties located in ISO public protection class areas 9 and 10 Assigned Risk Auto Plan – currently have less than a dozen policies in the plan Workers Compensation Assigned Risk Plan – premium volume has dropped over $5 million in the past 6 months Maintain list of surplus lines companies eligible to do business in the State License of regulate ALL Professional Employer Organizations (PEO) License and regulate advisory organizations Report to Legislature on Workers Compensation, Consumer Credit Use, Liability Insurance, Fire Loss and Medical Malpractice – see this link for recent reports: http://170.94.5.1/dataservices/PandC/PCData.htm Report to NAIC on filing review times and self-certification pilot program filings

Important Issues and Legislation • Credit Scoring • No changes from last legislative session • First Credit use report indicates only 11% of policyholders in personal lines insurance paid a higher premium because of insurance companies using credit in determining premiums • Over one-half of companies use credit (comprising approximately 87% of the total premium for personal lines) • Report is available at http://170.94.5.1/dataservices/PandC/PCData.htm • NEW ISSUE: C.LU.E. AND ISO A-PLUS databases are “consumer credit reporting agencies” requiring insurers to give notices under Act 1452 of 2003 • Fire Losses • Act 1345 of 2003 fire loss report • Largest counties in population or in number of policies tended to have higher loss ratios for fire losses

Important Issues and Legislation (continued) • Medical Malpractice • Act 1007 of 2003 required an annual report on the state of the market • 2004 Report found that rate increases were slowing in both frequency and amount • 2005 Report showed around 100% loss ratio without operating, selling expenses, etc • Loss ratios still in excess of 100% • Recommended no changes be made to tort reform legislation passed in 2003 • Workers Compensation • Annual report indicated that rates continue to decrease • Assigned risk plan premium is decreasing • Act 1917 of 2005 requires a subcontractor to have coverage before it can accept a certificate of coverage from its subcontractors.

Important Issues and Legislation (continued) • Insurance Reform – Act 1697 of 2005 • Requires the Department to place its homeowners and private passenger auto rate surveys on the internet along with a notice of any overall rate increase made in a filing – effective August 12, 2005 • Requires a notice to HO and PPA insureds if overall rates increase by 20% due to a rate filing. The Insurance Department must run a legal notice in a state wide publication of such a filing as well – effective June 1, 2006 • Malpractice rate filings that have an overall impact of 20% or greater require the insurer to run a notice in the newspaper of the filing – effective – effective January 1, 2006 • We now must approve or disapprove all malpractice rate filings with a 60 days of filing - effective January 1, 2006 • Put into code Rule 23 filing requirements for malpractice rates - effective January 1, 2006

Important Issues and Legislation (continued) • Act 269 of 2005 – prohibits conditioning settlement of a claim on issuing a single check jointly to the injured party and the injured party’s insurance company • Act 1194 of 2005 prohibits using “not a fault” accidents in determining rates and non renewals for “motor vehicle liability insurance” – includes both commercial and PPA • Review A.C.A. 23-63-109 and 110 regarding rates and non renewals for weather claims and no loss claims, respectively • Review Directive 1A-2004 regarding cancellation and non renewal generally • Improvements to State Based Systems (NAIC and Arkansas efforts) • We participate in the NAIC self certification pilot program • We report to the NAIC concerning our turn around time for rate and form filings • For no problem filings we review in an average of 1 day (for SERFF, 7 days for paper) • Problem filings are reviewed in an average of 16 days • 100% of no problem filings handled in less than 30 days for most recent month

Important Issues and Legislation (continued) • Mechanized logging and Workers Compensation • All employers receiving the mechanized logging class code in Arkansas for workers compensation must have a current certification on file that the employer qualifies for the class code – issued by the Arkansas Timber Producers Association • Private Passenger Auto • Most filings are indicating rate decreases • Act 1194 of 2005 should cause a review of how “not at fault” claims are treated – PROXIMATE CAUSATION TEST • means … not at fault with regard to any negligent or intentional act that was the proximate cause of any accident or injury, to be determined in accordance with policy language and state law… • Cost of defense shall not be a factor in determining whether or not a person is “innocent.” Cost of defense may, however, be considered a “loss” under Ark. Code Ann. § 23-61-310,… • Look for website changes and updates: • http://170.94.5.1/dataservices/PandC/pchome.htm

Other Department Changes of Note • Web Site Updates • ARKANSAS INSURANCE DEPARTMENT • http://insurance.arkansas.gov/ • PROPERTY & CASUALTY DIVISION • http://www.insurance.arkansas.gov/PandC/divpage.htm • Rule updates • Rule 23 on rate and form filing requirements • Mostly technical • New PPA and HO survey forms • Professional Liability Law changes (Act 1697) • Speed to Market updates • Rule 61 • Updates to AR166 reports (Act 166 of 1993) regarding all lines of liability insurance annual performance