Download

1 / 25

310 likes | 1.05k Views

Part IIA, Paper 1 Consumer and Producer Theory. Lecture 7 Production Function and Cost Function Flavio Toxvaerd. Today’s Outline. Quick recap The production function Isoquants and optimality condition The producer’s problem Factor demands Cost function, short run vs. long run.

E N D

Part IIA, Paper 1Consumer and Producer Theory Lecture 7 Production Function and Cost Function Flavio Toxvaerd

Today’s Outline • Quick recap • The production function • Isoquants and optimality condition • The producer’s problem • Factor demands • Cost function, short run vs. long run

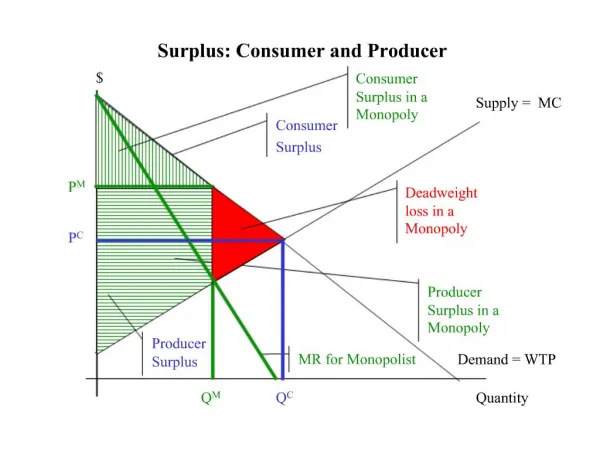

Producer Theory We wish to analyse production decisions of firms with the same rigour as used to analyse consumption decisions Consumer Theory Represent preferences (Utility function) Utility maximisation Dual problem (min expenditure to obtain desired utility) Producer Theory Represent technology (Production function) Profit maximisation Cost function (min expenditure to obtain desired output)

Technology What is technology? May be represented as a mapping from inputs (X) to outputs (Y) such that, for any vector of inputs denotes the set of outputs that can be obtained using x. Note: T(x) is not a function, more than one output may be possible with the same input x Inputs Outputs

Production Plans • A production plan is a vector of inputs and outputs ( x , y ) where x = (x1,…,xn) is a vector of inputs and y = (y1,…,ym) is a vector of outputs • A production plan (x , y) is feasible if y T(x) and so, technology allows the vector of inputs, x, to be converted into the vector of outputs, y.

Production Possibility Set The production possibility set (PPS) is the set of all feasible production plans Efficient production y PPS x

Assumptions on the PPS • Assumption 1: if x = 0 and (x,y)PPS, then y = 0 • Assumption 2: Free disposal • if (x,y)PPS then • for all x’x, (x’,y)PPS • for all y’y, (x,y’)PPS • Assumption 3: The PPS is closed: so the boundary of the PPS is contained in the PPS - and ‘efficient’ production well defined

Input Requirement Set • The input requirement set is the set of vectors of inputs required to produce a particular vector of outputs x2 • The Efficient boundary of IRS is an isoquant • Assumption 4: All input requirement sets are convex. • (PPS is quasi-concave) x1

Restricted Production Set The restricted production setis the set of all the vectors of outputs that are feasible given a particular vector of inputs, Efficient boundary of RPS is also sometimes called the Production Possibility Frontier y2 or, when there is only one output, the production function y1

The Production Function y = F(x) • Assumption 1:F(0) = 0 • Assumption 2: F(x) is a non-decreasing function isoquants are downward sloping • Assumption 3: production function defined • Assumption 4: isoquants are convex production function is quasi-concave

Isoquants Isoquants show combinations of inputs for which output is constant |slope of isoquant| = Technical Rate of Substitution

Production Problem First order conditions:

Production Problem Eliminating the Lagrange Multiplier () gives RTS = Ratio of Prices Production function and Note, with more than two commodities have FOC

Conditional Factor Demand Function • Solution gives the cost minimising levels on inputs x1= x1(p1,p2,y) , x2= x2(p1,p2,y) • Giving demand for inputs as a function of prices and the desired output level • This is the Conditional Factor Demand Function

Cost Function The cost function C(p,y) gives the minimum cost of producing a specified output level (y) given the factor prices (p) This is just the equivalent of the Expenditure Function in consumer theory

Properties of the Cost Function • Homogeneous of degree 1 in prices • Proof: No change in relative prices, so no change in optimal solution - so expenditure changes by same proportion. • Non-decreasing in prices • Concave in prices • Proof: If prices change, costs will increase linearly if inputs are unchanged. Thus any change in input usage must be to reduce costs - and so costs increases less than linearly

Envelope Theorem How do costs change when prices or desired output change? Sheppard’s Lemma Marginal Cost

Duality • Duality ensures that there is a direct relationship between the production function and the cost function – the cost function fully ‘represents’ production • For every ‘acceptable’ cost function, there exists an equivalent production function which possesses convex isoquants

x2 x02 x1 x01

Short Run Cost Function If not all inputs are variable, then the constrained optimisation problem is more constrained – minimise costs subject to some inputs being fixed Gives constrained solution and obtain short run (constrained) cost function

Properties of the SR Cost Function • Homogeneous of degree 1 in prices. • Non-decreasing in prices. • Concave in prices 4. 5. 6.

Summary • Production function and isoquants • The producer’s problem • Optimality condition • Dual problem

Readings • Varian, Intermediate Micro chapters 17, 19, 20 • Varian, Microeconomics Analysis, chapters 1,4,5,6

Next Time… • Profit maximisation • Factor demands • The supply function