Download

1 / 8

80 likes | 215 Views

Reporting Irregular Items on the Multi-Step Income Statement. Georgia CTAE Resource Network Curriculum Office, June 2009 To accompany curriculum for the Georgia Peach State Career Pathways June 2009, Dr. Marilynn Skinner . REPORTING IRREGULAR ITEMS. ALL-INCLUSIVE APPROACH

E N D

Reporting Irregular Items on the Multi-Step Income Statement Georgia CTAE Resource Network Curriculum Office, June 2009 To accompany curriculum for the Georgia Peach State Career Pathways June 2009, Dr. Marilynn Skinner

REPORTING IRREGULAR ITEMS ALL-INCLUSIVE APPROACH most items are recorded in current period income CURRENT OPERATING APPROACH income from regular and recurrent items is reported MODIFIED ALL-INCLUSIVE APPROACH irregular items are highlighted

Discontinued Operations Assets Operating Results Activities of the segment Clearly distinguishable • Not “discontinued operations” • disposal of a part of a business line • shifting production locations • phasing out a product line

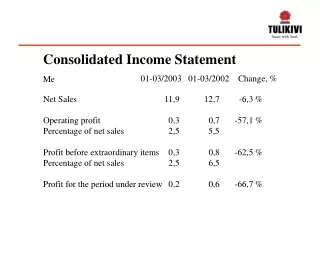

Income from continuing operations $20,000,000 Discontinued operations Loss from operation of discontinued division (net of tax) $300,000 Loss from disposal of division (net of tax) 500,000 800,000 Net Income $19,200,000

Extraordinary Items • Unusual (unrelated to ordinary activities) • Infrequent • Not “extraordinary” • write-down of receivables, inventories, etc. • gains or losses from sale of PP&E • effects of a strike Question 27, p. 151 $450,000 gain on forced condemnation sale of facility.

Unusual Gains and Losses • unusual or infrequent but not both • report in “Other Gains and Losses” • before income tax

Changes in Accounting Principle • e.g. change in inventory or depreciation method • report the retroactive impact as of the beginning of the year • report as an adjustment to beginning R/E; not on the income statement Brief Exercise 4-7, p. 153 Change in estimate of bad debt expense.

Changes in Estimates • e.g. change in estimate of the useful life of an asset or bad debts expense • do not handle retroactively • include in ordinary income Prior Period Adjustments • record as an adjustment to the beginning balance of retained earnings • does not affect net income