Download

1 / 56

590 likes | 1.21k Views

Chapter 16: Negotiability, Transferability, and Liability. Learning Objectives. What requirements must an instrument meet to be negotiable? What are the requirements for attaining the status of a holder in due course (HDC)?

E N D

Learning Objectives • What requirements must an instrument meet to be negotiable? • What are the requirements for attaining the status of a holder in due course (HDC)? • What is the difference between signature liability and warranty liability?

Learning Objectives • Certain defenses are valid against all holders, including HDC’s. What are these defenses called? Name four defenses that fall within this category. • Certain defenses can be used against an ordinary holder but are not effective against an HDC. What are these defenses called? Name four defenses that fall within this category.

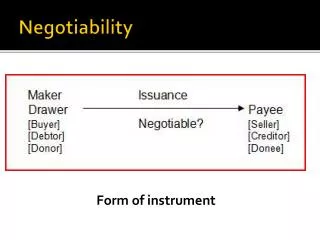

Types of Instruments • A “negotiable instrument” is a signed writing containing an unconditional promise to pay an exact sum of money. • Most negotiable instruments are paper documents, referred to as commercial paper.

Types of Instruments • The UCC specifies four types of negotiable instruments: • Drafts, Checks, Notes, and Certificates of Deposit. • Orders to Pay or Promises to Pay. • Can also be demand instruments or time instruments.

Types of Instruments • Drafts and Checks (Orders to Pay). • Unconditional order involves three parties: Drawer (creator of draft), Drawee (financial institution) and Payee. • Most common type of draft is a bank check.

Types of Instruments • Drafts and Checks (Orders to Pay). • Time Drafts and Sight Drafts. • Time Draft: payable certain future time. • Sight Draft: payable on sight. May be payable on acceptance (drawee’s written promise to pay the draft when due).

Types of Instruments • Drafts and Checks (Orders to Pay). • Trade Acceptances. • Type of draft frequently used in sale of goods. • Trade acceptance: seller of goods is both drawer and payee. Buyer of goods is the drawee.

Types of Instruments • Drafts and Checks (Orders to Pay). • Checks. • Three parties: Writer of the check is drawer, the bank is drawee, and person to whom check is made is payee. • Checks are payable on demand.

Types of Instruments • Promissory Notes and Certificates of Deposit (Promises to Pay). • Promissory Notes are two party instruments: • Maker (Promisor) and • Bearer (Promisee). • Can be payable at a definite time or on demand.

Types of Instruments • Promissory Notes and Certificates of Deposit (Promises to Pay). • Certificates of Deposit. Certificate of Deposit: type of note issued when a party deposits funds with a bank, and bank promises to repay funds with interest on certain date. • Bank is maker, and Depositor is Payee.

Requirements for Negotiability • For an Instrument to be negotiable, it must: • Be Signed by the Maker or Drawer. • Signature Requirements: manual or by a device. • Placement of the Signature.

Requirements for Negotiability • For an Instrument to be negotiable, it must: • Be an Unconditional Promise or Order to Pay. • Promise or Order. • Unconditionality of the Promise or Order. • State a Fixed Amount of Money.

Requirements for Negotiability • For an Instrument to be negotiable, it must: • Be Payable on Demand or at a Definite Time. • On Demand: “Payable at sight” or “Payable upon presentment.” • CASE 16.1 RegerDevelopment, LLC v. National City Bank (2010). Why doesn’t the duty of good faith apply to lenders seeking payment on demand notes?

Requirements for Negotiability • For an Instrument to be negotiable, it must: • Be Payable on Demand or at a Definite Time. • Payable at a Definite Time: specified date, within definite period of time, date or time readily ascertainable.

Requirements for Negotiability • Acceleration Clause: allows holder to demand full payment if a certain event occurs. • Extension Clause: the reverse of an extension clause.

Requirements for Negotiability • Be Payable to Order or Bearer, Unless It is a Check. • Order Instruments: payable to “the order of” an identified person, or to “an identified person or order.”

Requirements for Negotiability • Be Payable to Order or Bearer, Unless It is a Check. • Bearer Instruments: the holder is the payee. • CASE 16.2 Las Vegas Sands, LLC v. Nehme (2011). Why was the marker a bearer instrument?

Requirements for Negotiability • Factors That Do Not Affect Negotiability. • Omission of Date. • Postdating or Antedating. • Handwritten Terms outweigh typewritten and preprinted terms. • Words outweigh figures.

Requirements for Negotiability • Factors That Do Not Affect Negotiability. • If instrument states “with interest” but doesn’t specify the rate, it is the judgment rate of interest. • Check is negotiable even if there is a “nonnegotiable” note on it.

Transfer of Instruments • A negotiable instrument can be transferred by assignment or negotiation. • Transfer by Assignment. • Gives assignee only those rights assignor possessed. • Transferee is an assignee, not a holder.

Transfer of Instruments • Transfer by Negotiation. • Creates a holder, who receives the rights of a previous possessor. • There are two methods of negotiation so receiver becomes a holder, depending on whether instrument is an order or bearer instrument.

Transfer of Instruments • Transfer by Negotiation. • Negotiating Order Instruments: requires both indorsement and delivery. • Negotiating Bearer Instruments: delivery only. Indorsement is not necessary.

Indorsements • Signature with or without additional words or comments. • Blank Indorsements: does not specify a particular indorsee and may consist of a mere signature. • Special Indorsements: contains signature and identifies payee.

Indorsements • Qualified Indorsements: indorser who does not wish to be liable (“without recourse”). • Effect of Qualified Indorsements. • Special versus Blank Indorsements. • CASE 16.3 Hammett v. Deutsche Bank National Co. (2010). What was the legal effect of the blank qualified indorsement?

Indorsements • Restrictive Indorsements: requires indorsee to comply with certain instructions regarding funds. • Conditional Indorsements. • Indorsements for Deposit or Collection. • Trust (Agency) Indorsements.

Indorsements • Miscellaneous Indorsement Problems. • Misspelled Names. Indorsement should generally be identical to name on instrument. • Misspelled name OK. • Instruments Payable to Legal Entities. • Negotiable by authorized representative of the entity.

Indorsements • Miscellaneous Indorsement Problems. • Alternative or Joint Payees. • Alternative Payees Presumed- either may indorse. Jointly - both must indorse. • Suspension of the Drawer’s Obligation.

Holder in Due Course (HDC) • Holder versus Holder in Due Course (HDC). • Holder possess an order or bearer paper and the instrument is drawn or indorsed to the holder. • HDC: holder plus takes for value, takes in good faith, and without notice of defense to payment.

Holder in Due Course (HDC) • Requirements for HDC Status. • Taking “For Value”: No value if gift or inheritance. Not the same as consideration. Holder can take for value by: • Performing the instrument’s promise. • Acquiring a security interest or other lien in the instrument.

Holder in Due Course (HDC) • Requirements for HDC Status. • Taking for Value. • Taking instrument in payment for an antecedent debt. • Giving a negotiable instrument as payment. • Giving irrevocable commitment as payment.

Holder in Due Course (HDC) • Requirements for HDC Status. • Taking in Good Faith. • Honesty in fact and observance of reasonable commercial standards of fair dealing. • Only applies to holder, not transferor. • CASE 16.4 Triffin v. Liccardi Ford, Inc. (2011). Why wasn’t Triffin a holder in due course?

Holder in Due Course (HDC) • Requirements for HDC Status. • Taking Without Notice: Holder takes the instrument with notice if he knows/has reason to know: • Instrument is overdue. • Instrument has been dishonored. • Actual knowledge or any suspicious event.

Holder in Due Course (HDC) • Holder through an HDC. • “Shelter Principle”: A person who does not qualify to be a HDC but who derives her title through an HDC can acquire the rights and defenses of an HDC.

Holder in Due Course (HDC) • Holder through an HDC. • Purpose of the Shelter Principle: extends benefits of HDC and allows HDC to dispose of instrument. • Limitations on the Shelter Principle: no fraud, illegality, claim or defense.

Signature and Warranty Liability • Signature Liability. • Relates to signatures on instruments. • Signers of negotiable instruments are potentially liable for amount stated on instrument. • Primary Liability: Makers/Acceptors. • Secondary Liability: Drawers/Indorsers.

Signature and Warranty Liability • Signature Liability. • Primary Liability. Person: • Promises to pay the note. • Obligated to pay terms of instrument at time of signing. • Acceptors: Drawee promises to pay an instrument when presented for payment.

Signature and Warranty Liability • Signature Liability. • Secondary Liability. • Proper Presentment: Must be timely (checks w/in 30 days). • Timely Presentment: Manner of Notice in any Reasonable manner. • Dishonor. • Proper Notice.

Signature and Warranty Liability • Signature Liability. • Unauthorized Signatures: arise in two situations: • Forgery: does not bind Principal but Bank may be liable if negligent. • Unauthorized Signature: Agent is personally liable, but Principal is not, unless ratified.

Signature and Warranty Liability • Signature Liability. • Unauthorized Signatures: Exceptions to the General Rule of No Liability: • Ratification of Signature: principal become liable. • Negligence: party who substantially contributed to forgery is liable.

Signature and Warranty Liability • Signature Liability. • Special Rules for Unauthorized Indorsements. • Unauthorized indorsement does not bind maker/drawer except: • Imposter Rule: one who induces a maker to issue an instrument in the name of an impersonated payee.

Signature and Warranty Liability • Signature Liability. • Special Rules for Unauthorized Indorsements. • Unauthorized indorsement does not bind maker/drawer except: • Fictitious Payees: cause an instrument to be issued to a payee who will have no interest in the instrument.

Signature and Warranty Liability • Warranty Liability. • Transferors make certain implied warranties regarding instruments they negotiate. • Warranty Liability not subject to conditions of proper presentment, dishonor, or notice. • Warranties: Transfer or Presentment.

Signature and Warranty Liability • Warranty Liability. • Transfer Warranties: Following warranties extend to all subsequent holders: • Transferor is entitled to enforce the instrument. • Signatures are authentic and authorized.

Signature and Warranty Liability • Warranty Liability. • Transfer Warranties: Following warranties extend to all subsequent holders: • Instrument has not been altered. • Instrument not subject to defense. • Transferor has no notice of insolvency.

Signature and Warranty Liability • Warranty Liability. • Transfer Warranties. • Parties to Whom Warranty Liability Extends:Extends warranty to any holder who takes in good faith. Without indorsement, warranties extend only to immediate transferee.

Signature and Warranty Liability • Warranty Liability. • Transfer Warranties. • Recovery for Breach of Warranty: good faith holder can sue for breach of warranty. Notice of the claim within 30 days.

Signature and Warranty Liability • Warranty Liability. • Presentment Warranties: person who presents an instrument makes the following presentment warranties: • No missing or unauthorized indorsements. • Instrument has not been altered. • Person obtaining payment has no knowledge signature is unauthorized.

Defenses, Limitations and Discharge • Universal (or Real) - can be used to defeat a holder and a HDC. • Personal - can be used to defeat a holder but not a HDC.

Defenses, Limitations and Discharge • Universal Defenses. • Forgery of maker’s or drawer’s signature. • Or if an authorized agent exceeds his authority to the amount which exceeds his authority. • Fraud in the Execution: the ”autograph” situation, not fraud in the inducement.