Download

1 / 16

160 likes | 181 Views

Learn how to identify, evaluate, and implement countermeasures for process improvement. Utilize cost/benefit analysis, cash flow valuation, and action planning. Track results, standardize, and replicate successful strategies.

E N D

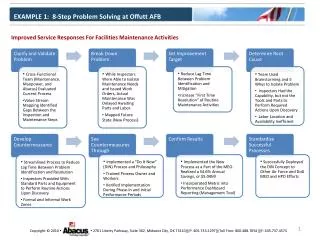

Sigma Quality Management -6 -4 -2 0 2 4 6 Selecting & Implementing Countermeasures

Analyze Root Causes/Process Variables Identify the possible countermeasures Evaluate and select the best countermeasures Plan to implement the countermeasures To: Execute the Countermeasures Selecting Countermeasures - Roadmap

Generating Countermeasures • Attacking the Causes • Long Lasting Improvements • Temporary Fixes • Don’t Reinvent the Wheel • Phased Implementation • Error proofing vice Inspection

Cost/Benefit Analysis • Quantifying Benefits • Quantifying Costs

“Gozzinta’s & Goesoutta’s” Sources of Cash Benefits: • Cash received as a result of sales, • Cost reductions (when a more efficient process replaces a less efficient one, or from tax benefits), • Cash received when replaced equipment is sold, and • Cash received from salvage value of equipment, plant or facility at end-of-life. Sources of Cash Payments: • Initial cost of the investment (capital cost), • Capital improvements made during the life of the equipment/plant/facility, • Operating costs, such as wages, materials, energy, taxes and maintenance.

Time Period (Years) 0 1 2 3 4 5 Income Statement Changes: Sales (A) 0 $7500 $8000 $8000 $7500 $7500 O perating Expenses (B) (416) (6972) (6972) (6972) (6972) (6972) Depreciation (C) 0 (560) (336) (202) (151) (151) Pretax Profit (D = A+ B + C) (416) (32) 692 826 377 377 Taxes (F = D x E) (E =tax rate = 0.34) 141 11 235 281 128 128 Profit after Taxes (G = D + F) (275) (21) 457 545 249 249 Non cash Charges: Depreciation ( - C) 0 560 336 202 151 151 Capital Investments: Property, facility, equipment (H) (1400) 0 0 0 0 0 Working Capital Changes (I) (940) 0 0 0 0 900 Residual Net Cash Flow (J = G + H + I) $(2615) $539 $793 $747 $400 $1300 Cash Flow

Valuing Different Proposals Benefit Cost Ratio: Calculate the Ratio of Net Benefits to the Investment: Benefit Cost Ratio = ($539 + 793 + 747 + 400 + 1300)/$2615 = $3779/2615 = 1.45 Payback Period: Calculate the time required for the annual net benefits exceed the initial investment cost: Payback Period = Investment/Average Yearly Net Benefit = $2615/756 = 3.5 Years Annual Worth Present Worth Rate of Return

Barriers Aids Cost to implement Savings Fear of change Fixing old problems Lack of experience Learning something new Barriers & Aids Analysis

Implement the Action Plan Monitor Progress of Implementation Check Results – Plan and Performance To Standardize/ Replicate Countermeasures Executing Countermeasures - Roadmap

Tracking Results # Defects Time Countermeasures Implemented Your Factor’s Effect: Results Change (Process Output): “External” Factor’s Change Effect:

Standardization/Replication • Standardization Methods • Replication of Improvements – Leveraging Your Work