Download

1 / 42

420 likes | 552 Views

Porter Analysis. A framework for evaluating the interaction of financial decisions and non-financial decisions in terms of their impact on firm value. P.V. Viswanath. Financial Theory and Strategic Decision-Making. Before Valuation.

E N D

Porter Analysis A framework for evaluating the interaction of financial decisions and non-financial decisions in terms of their impact on firm value P.V. Viswanath Financial Theory and Strategic Decision-Making

Before Valuation • A key part of Valuation is forecasting the future cashflows of the firm. • For that, it’s important to have a good understanding of what the firm is, its strengths, where it is, who its competitors and their strengths. • A firm does not operate in a vacuum. • Forecasting cashflows is impossible without knowing the environment.

Porter Analysis • Porter’s Five Forces model Analysis is a systematic way of analyzing the industry environment in which the firm finds itself. • Following this, it is necessary to do a SWOT-type analysis to evaluate the firm within this environment.

Using Porter Analysis • Porter Analysis is usually used for strategic purposes, such as in selecting firms for acquisitions. • We will look at it in terms of where and how financial decisions and financial variables matter. • The following slides will not explicitly discuss financial variables, but the point is to keep them in mind in our discussion of strategic decision-making.

Financial Decisions • What are the corporate decisions that you think of as financial?

Financial Decisions • Broadly speaking, we can divide corporate decisions into those that affect the composition of the left-hand side of the balance sheet (i.e. the assets side) and those that affect the composition right hand side of the balance sheet (i.e. the liabilities side). • The first category of decisions are operating decision. • Financial decisions are those that affect the composition of the liabilities of the firm, i.e the second kind.

Financial Decisions • Here is a partial list of financial decisions: • Short term financing • Long-term financing or the capital structure decision • Decisions regarding the maturity of debt • Decisions regarding currency in which to borrow • Decisions regarding borrowing at fixed rates or floating rates • Decisions to hedge interest rates or not

Financial Decisions • Decision to list on an exchange • Decision to pay dividends • Credit terms, such as number of days credit allowed, cash discounts, etc. • Hedging • Determining cost of capital and cost of capital are processes that have to do with financial decisions, but are not themselves financial decisions.

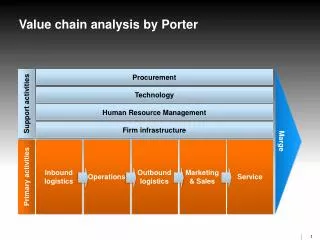

Financial Decisions • Many operating decisions will need to modifications of financial decisions. For example if the firm decides to sell abroad, it may then need to hedge its foreign currency inflows. • Normally operating decisions are primary, they are taken first, and they impact the financial decisions. This is not to say that the operating actions are taken first, just that these decisions are taken first, e.g. which industry to operate in, which market to target, where to locate a plant etc.

Financial Decisions • We are interested, here, in financial decisions that are going to affect or limit or enhance the operating decisions of the firm and the cashflows generated by the operating decisions. • This means that there will have to be some sort of higher-level coordination between the financial decision-makers and the operating decision-makers. • For example, a decision on credit policy will have to be coordinated with the decision as to which market segment to target – certain markets may require more liberal provision of credit. • Similarly, taking on financial leverage could lead to the firm being perceived as aggressive and hence impact the extent of competition for the firm.

Five Forces model of Porter • Ease of entry of competitors • How easy or difficult is it for new entrants to start to compete, which barriers do exist? • Threat of substitutes • How easily can the product or service be substituted, especially cheaper? • Bargaining power of buyers • How strong is the position of buyers, can they work together to order large volumes? • Bargaining power of suppliers • How strong is the position of sellers, are there many or only few potential suppliers, is there a monopoly? • Rivalry among the existing players • Is there a strong competition between the existing players, is one player very dominant or all all equal in strength/size? • Government Intervention • Can government policies be used to the advantage of the firm? From http://www.valuebasedmanagement.net/methods_porter_five_forces.html

Porter: Five Strategic Forces www-mime.eng.utoledo.edu/people/faculty/rbennett/engineering_management/Powerpoint%20Slides/ch09.ppt

New Entrants: Barriers to Entry • Economies of Scale • To the extent that there are economies of scale, it will be difficult for a new firm to come in and compete with established firms. • Product Differentiation • To the extent that the firm’s products are distinct and non-copiable, new firms won’t be able to come in and take away customers. • Brand Identification • To the extent that there is brand identification, customers will remember the firm’s product and will resist switching. • Switching Cost • If it is costly for the customer to switch, new entrants won’t be able to convince them to do so.

New Entrants: Barriers to Entry • Access to Distribution Channels • If the firm has preferential or monopolistic access to distribution channels, it is more resistant to competition. • Capital Requirements • If capital requirements are high, new under-capitalized firms won’t be able to enter the industry. • Access to Latest Technology • If technology is important in the industry, new firms are less likely to have access to them, which is good for established firms. • Experience and Learning Effects • If experience is necessary for a firm to figure out how to operate efficiently, established firms have a distinct advantage.

Barriers to Entry: Examples • Regulatory restrictions (e.g. banking license) • brand names (e.g. Xerox, McDonalds – can develop customer loyalty; hard to develop and/or imitate) • patents (illegal to exploit without ownership; e.g. new drugs – cf. also RIM) • A small co., NTP, had a patent on crucial technology that RIM used for its Blackberry • unique know-how (e.g. WalMart’s “hot docking” technique of logistics management) • Accumulated experience (cf. learning curve)

New Entrants/ Industry Competition: Government Action • Industry Protection • Industry Regulation • Consistency of Policies • Capital Movement Amongst Countries • Custom Duties • Foreign Exchange • Foreign Ownership • Assistance Provided to Competitors

Finance and Industry Entry • How can financial strategies make it more difficult for new firms to enter the industry and compete with your firm?

Porter: Five Strategic Forces www-mime.eng.utoledo.edu/people/faculty/rbennett/engineering_management/Powerpoint%20Slides/ch09.ppt

Industry Competition:Rivalry Among Competitors • Concentration and Balance among Competitors • To the extent that there is no single large competitor, the firm is better off • Industry Growth • If the industry is growing, there’s more room for everybody; less pressure on the firm • Fixed Cost • The higher the operating leverage, the more competitors are going to be hungry for revenue – downside risks are greater • Product Differentiation • If products are differentiated, markets are in a sense, segmented, and there are no competitors

Industry Competition:Rivalry Among Competitors • Intermittent Overcapacity • The extent to which firms have overcapacity from time to time, leading them to find additional sources of orders to keep resources fully employed. • Switching Costs • The extent to which it’s easy for customers to switch from this firm to other firms’ products will also determine how much other firms will exert themselves to get them to switch • Corporate Strategic Stakes • If the strategic stakes are high – for example, if there is only room for a few players, then firms will fight harder

Industry Competition:Barriers to Exit • Asset Specialization • If assets are specialized, firms will not want to exit – quitting the industry can be costly in terms of lower prices for assets no longer in use. • One-time Cost of Exit • For example, if businesses are required to pay for any environmental costs before they exit or if they have to set aside funds to pay for potential future lawsuits, they are less likely to exit a business • Strategic Interrelationships with Other Businesses • Emotional Barriers • Government and Social Restrictions

Finance and Fighting Competitors • How can the right financial decision help overwhelm or outgun existing competitors?

Porter: Five Strategic Forces www-mime.eng.utoledo.edu/people/faculty/rbennett/engineering_management/Powerpoint%20Slides/ch09.ppt

Bargaining Power of Suppliers • Number of Important Suppliers • The fewer the number of important suppliers, the more power they have over the firm, and the greater their ability to extract producer surplus. • Availability of Substitutes for the Suppliers’ Products • This would reduce supplier power. • Differentiation or Switching Costs of Suppliers’ Products • If it’s difficult for the firm to switch to other suppliers, the current suppliers can charge more. • Suppliers’ Threat of Forward Integration • To the extent that suppliers might potentially themselves become competitors, they are less reliable and need to be looked at strategically

Bargaining Power of Suppliers • Industry Threat of Forward Integration • To what extent is it possible that the entire supplier industry might integrate forward? • Suppliers’ Contribution to Quality or Service of the Industry Products • How crucial are suppliers in the maintenance of the quality of industry products? Clearly, this will determine supplier power. Also, if this is an important factor, then the supplier industry might be more important, and might integrate forward. • Total Industry Cost Contributed by Suppliers • This goes to the same issue as above, but from a more quantitative perspective. • Importance of the Industry to Suppliers’ Profits

Finance and Suppliers • How can financial decisions help redress the balance of power between the firm and its suppliers?

Bargaining Power of Customers • Number of Important Buyers • The greater the number of important buyers, the less power does the firm have to manipulate prices • Availability of Substitutes for the Industry Products • The impact of this on price elasticity of demand for the industry’s products is obvious. • Buyer’s Switching Costs • This is relevant both in terms of switching to competitors’ products and switching to products manufactured by other industries. • Buyer’s Threat of Backward Integration • The buyer might choose to integrate backward and manufacture his input goods, himself. This means that buyers have to be looked at strategically; they also have more power over the prices they are charged.

Bargaining Power of Customers • Industry Threat of Backward Integration • The entire buyer industry might integrate backward. • Contribution to Quality or Service of Buyer’s Products • The greater the contribution of the firm’s product to the quality of the product, the greater the power of the firm. On the other hand, this might also impel the buyer to integrate backward. • Total Buyer’s Cost Contributed by the Industry • This is similar to the previous point, but in a more quantitative fashion. • Buyer’s Profitability • The more profitable buyers are, the more amenable they are to paying more for their input products.

Finance and Customers • How can financial decisions help increase the firm’s economic power vis-à-vis its customers?

Porter: Five Strategic Forces www-mime.eng.utoledo.edu/people/faculty/rbennett/engineering_management/Powerpoint%20Slides/ch09.ppt

Substitutes • Some of these points have already been addressed in looking at buyers/suppliers. However, it’s useful to consider it again from the product perspective, rather than from the perspective of other economic actors. • Availability of Close Substitutes • User’s Switching Costs • Substitute Producer’s Profitability and Aggressiveness • Where is the substitute product located on the Price/Value dimensions?

Finance and Competition from Substitutes • Can financial decisions help the firm ward off substitutes competing against its products?

Porter Model Applied:Pharmaceutical Industry 1990s • Barriers to Entry – Very Attractive • Steep R&D experience curve effects • Large economies-of-scale barriers in R&D • Critical Mass in R&D and marketing required global scale • Significant R&D and marketing costs • High Risk inherent in the drug development process • Increasing threat of new entries from biotechnology companies

Porter Model Applied:Pharmaceutical Industry 1990s • Bargaining Power of Suppliers • Mostly Commodities • Individual Scientists may have some personal leverage

Porter Model Applied:Pharmaceutical Industry 1990s • Bargaining Power of Buyers: Mildly Unattractive • Buying Process is price sensitive – the consumer did not pay and the buyer did not pay • Large power of buyers – plan sponsors with an incentive to contain costs • Mail-order pharmacies obtain large discounts on volume drugs • Large aggregated buyers – hospital suppliers, large distributors, government institutions

Porter Model Applied:Pharmaceutical Industry 1990s • Threat of Substitutes: Mildly Unattractive • Generic drugs weakening branded drugs • More than half the patent life spent on product development and approval process • Technological development is making imitation easier – reverse engineering • Consumer aversion to chemical substances erodes the appeal for pharmaceutical drugs

Porter Model Applied:Pharmaceutical Industry 1990s • Intensity of Rivalry: Attractive • Global Competition Concentrated Amongst fifteen large companies • Most companies focus on certain types of disease therapy • Competition amongst incumbents limited by patent protection • Competition based on price and product differentiation • Government intervention increases rivalry • Strategic alliances establish collaborative agreements among industry players • Very profitable industry, but declining margins

Resource-based Views of the Firm: Tangible Assets • Tangible assets are the easiest to value, and often are the only resources that appear on a firm’s balance sheet. • They include real estate, production facilities, and raw materials, among others. • Although tangible resources may be essential to a firm’s strategy, due to their standard nature, they rarely are a source of competitive advantage. Source: David Collis and Cynthia Montgomery

Resource-based Views of the Firm: Intangible Assets • Intangible assets include such things as • company reputations, • brand names, • cultures, • technological knowledge, • patents and trademarks, and • accumulated learning and experience.

Firm Resources:Organizational Capabilities • Organizational capabilities are not factor inputs like tangible and intangible assets • They are complex combinations of assets, people, and processes that organizations use to transform inputs into outputs. • Includes a set of abilities describing efficiency and effectiveness: low cost structure, “lean” manufacturing, high quality production, fast product development.

Putting things together • Now that we have looked at the firm’s environment and its assets, we need to look at the firm’s strategy within this environment and how this relates to the other parties identified in the “five forces model.” • We must keep in mind, however, that our objective is not to craft new strategy for the firm, but rather to appreciate its current and potential strategy in • forecasting future cashflows • Evaluating investment risks • A useful place to find relevant information is the firm’s 10-K filing, particularly the “Risk Factors section.”

The impact of finance • Think again about capital structure, about financial risk management, about dividend policy and how they might affect all the issues relating to value creation in a firm.