Download

1 / 12

120 likes | 274 Views

Financial Intermediaries in the United States: What they are. What they do. Why the Banking Industry Is Regulated. Banks hold money. Banks provide credit. The government focuses on information problems and liquidity risk.

E N D

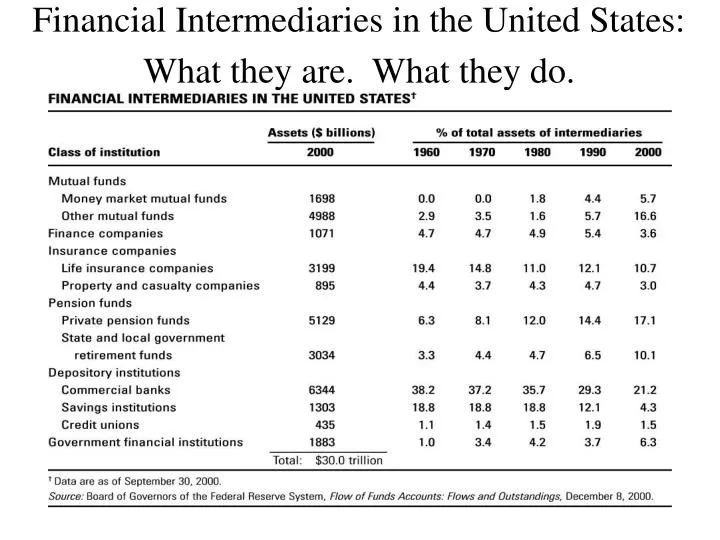

Financial Intermediaries in the United States:What they are. What they do.

Why the Banking Industry Is Regulated • Banks hold money. Banks provide credit. • The government focuses on information problems and liquidity risk. • Bank run: many depositors withdraw their deposits and the bank’s funds are exhausted. • Contagion: spreading of bad news about one bank to include other banks. • Bankers’ private information limits depositors’ ability to sort out weak banks.

Government Intervention in the Banking Industry • Federal Reserve was created to serve as a lender of last resort and issue currency. Since 1863 limits on banks’ ability to open branches have been imposed. • Numerous bank failures led to the creation of the Federal Deposit Insurance Corporation. • Moral hazard problems caused by bank insurance increased the need for monitoring. • Interest rate ceilings (Regulation Q) were intended to buttress bank profits.

Stock Market Crash, 1929 Britain off Gold, Sept. 1931 Banking Crises, 1932-33 Credit Crunch, 1966 Penn Central Bankruptcy, 1970 Continental Illinois, 1975 Hunt Brothers Silver Corner Franklin National Bank, 1984 LDC Debt Crisis, 1980s Stock Market Crash, 1987 S & L Debacle, 1989 – 91 Penn Square/Oil Patch/Junk Bonds Tequila Crisis, 1994-5 Asian Contagion, 1997 – 8 Long – Term Capital Management, 1998 911 Enron, 2001 Argentina, 2001 Crisis and ResponseFinancial Crises We Have Known

International Banking ServicesBranches, Agency Offices, Edge Act Corps, IBFsEurodollar Markets (LIBOR)

The Money Supply ProcessM = C + D and B = Bnon + BR = C + Rso M = {[1 + (C/D)] / [(C/D) + (R/D) + (ER/D)]} x B = m x B