Download

1 / 70

700 likes | 711 Views

This text provides an overview of cash payout procedures, dividend policies, and the tax treatment of dividends. It also explores the role of dividend reinvestment plans and discusses the residual theory of dividends.

E N D

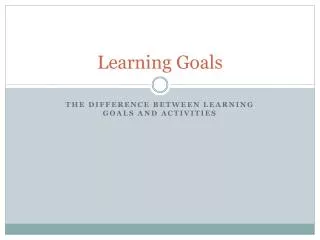

Learning Goals LG1 Understand cash payout procedures, their tax treatment, and the role of dividend reinvestment plans. LG2 Describe the residual theory of dividends and the key arguments with regard to dividend irrelevance and relevance. LG3 Discuss the key factors involved in establishing a dividend policy.

Learning Goals (cont.) LG4 Review and evaluate the three basic types of dividend policies. LG5 Evaluate stock dividends from accounting, shareholder, and company points of view. LG6 Explain stock splits and the firm’s motivation for undertaking them.

The Basics of Payout Policy:Elements of Payout Policy • The term payout policy refers to the decisions that a firm makes regarding whether to distribute cash to shareholders, how much cash to distribute, and the means by which cash should be distributed. • Cash can be distributed as a dividend or through stock repurchase plans.

The Basics of Payout Policy:General Lessons • Rapidly growing firms generally do not pay out cash to shareholders. • Slowing growth, positive cash flow generation, and favorable tax conditions can prompt firms to initiate cash payouts to investors. • Cash payouts can be made through dividends or share repurchases. • When business conditions are weak, firms are more willing to reduce share buybacks than to cut dividends.

Figure 14.1 Per Share Earnings and Dividends of the S&P 500 Index

Matter of Fact P&G’s Dividend History Few companies have replicated the dividend achievements of the consumer products giant, Procter & Gamble (P&G). P&G has paid dividends every year for more than a century, and it increased its dividend in every year from 1956–2010.

Figure 14.2 Aggregate Dividends and Repurchases for All U.S.-Listed Companies

Matter of Fact Share Repurchases Gain Worldwide Popularity • In most of the world’s largest economies, repurchases have been on the rise in recent years, eclipsing dividend payments at least some of the time in countries as diverse as Belgium, Denmark, Finland, Hungary, Ireland, Japan, Netherlands, South Korea, and Switzerland. • A recent study of payout policy at firms from 25 different countries found that share repurchases rose at an annual rate of 19% from 1999–2008.

Focus on Ethics Are Buybacks Really a Bargain? • In addition to simply returning cash to shareholders, companies also typically say they repurchase stock because they believe their stock is undervalued. • Yet new research shows that companies often use creative financial reporting to push earnings downward before buybacks, making the stock seem undervalued and causing its price to bounce higher after the buyback. Do you agree that corporate managers would manipulate their stock’s value prior to a buyback, or do you believe that corporations are more likely to initiate a buyback to enhance shareholder value?

The Mechanics of Payout Policy:Cash Dividend Payment Procedures • At quarterly or semiannual meetings, a firm’s board of directors decides whether and in what amount to pay cash dividends. • If the firm has already established a precedent of paying dividends, the decision facing the board is usually whether to maintain or increase the dividend, and that decision is based primarily on the firm’s recent performance and its ability to generate cash flow in the future. • Boards rarely cut dividends unless they believe that the firm’s ability to generate cash is in serious jeopardy.

Figure 14.3 U.S. Public IndustrialFirms Increasing, Decreasing, or Maintaining Dividends

The Mechanics of Payout Policy: Cash Dividend Payment Procedures (cont.) • The date of record (dividends) is set by the firm’s directors, the date on which all persons whose names are recorded as stockholders receive a declared dividend at a specified future time. • A stock is ex dividend for a period, beginning 2 business days prior to the date of record, during which a stock is sold without the right to receive the current dividend. • The payment date is set by the firm’s directors, the actual date on which the firm mails the dividend payment to the holders of record.

The Mechanics of Payout Policy: Cash Dividend Payment Procedures (cont.) On August 21, 2013, the board of directors of Best Buy announced that the firm’s next quarterly cash dividend would be $0.17 per share, payable October 1, 2013 to shareholders of record on Tuesday, September 10, 2013.The stock would begin trading ex-dividend on Friday, September 6, 2013. At the time, Best Buy had 340,967,179 shares of common stock outstanding, so the total dividend would be $57,964,420. Before the dividend was declared, the key accounts of the firm were as follows (dollar values quoted in thousands): • Cash: $680,000 • Dividends payable: $0 • Retained earnings: $3,395,000

The Mechanics of Payout Policy: Cash Dividend Payment Procedures (cont.) When the dividend was announced by the directors, almost $58 million of the retained earnings ($0.17 per share 341 million shares) was transferred to the dividends payable account. The key accounts thus became: • Cash: $680,000 • Dividends payable: $57,964 • Retained earnings: $3,337,036

The Mechanics of Payout Policy: Cash Dividend Payment Procedures (cont.) When Best Buy actually paid the dividend on October 26, this produced the following balances in the key accounts of the firm: • Cash: $622,036 • Dividends payable: $0 • Retained earnings: $3,337,036 The net effect of declaring and paying the dividend was to reduce the firm’s total assets (and stockholders’ equity) by almost $58 million.

The Mechanics of Payout Policy: Share Repurchase Procedures • Common methods for repurchasing shares include: • An open-market share repurchase is a share repurchase program in which firms simply buy back some of their outstanding shares on the open market. • A tender offer repurchase is a repurchase program in which a firm offers to repurchase a fixed number of shares, usually at a premium relative to the market value, and shareholders decide whether or not they want to sell back their shares at that price. • A Dutch Auction repurchase is a repurchase method in which the firm specifies how many shares it wants to buy back and a range of prices at which it is willing to repurchase shares. Investors specify how many shares they will sell at each price in the range, and the firm determines the minimum price required to repurchase its target number of shares. All investors who tender receive the same price.

The Mechanics of Payout Policy:Share Repurchase Procedures (cont.) In July 2013, Fidelity National Information Services announced a Dutch auction repurchase for 86 million common shares at prices ranging from $29 to $31.50 per share. At a price of $31.25, shareholders are willing to tender a total of 86 million shares, exactly the amount that Fidelity wants to repurchase.

The Mechanics of Payout Policy: Tax Treatment of Dividends and Repurchases For many years, dividends and share repurchases had very different tax consequences. • The dividends that investors received were generally taxed at ordinary income tax rates. • On the other hand, when firms repurchased shares, the taxes triggered by that type of payout were generally much lower. • Shareholders who did not participate did not owe any taxes. • Shareholders who did participate in the repurchase program might not owe any taxes on the funds they received if they were tax-exempt institutions, or if they sold their shares at a loss. • Shareholders who participated in the repurchase program and sold their shares for a profit only paid taxes at the (usually lower) capital gains tax rate, and even that tax only applied to the gain, not to the entire value of the shares repurchased.

The Mechanics of Payout Policy: Tax Treatment of Dividends and Repurchases The Jobs and Growth Tax Relief Reconciliation Act of 2003 significantly changed the tax treatment of corporate dividends for most taxpayers. • The act reduced the tax rate on corporate dividends for most taxpayers to the tax rate applicable to capital gains, which is a maximum rate of 5 percent to 15 percent, depending on the taxpayer’s tax bracket. • This change significantly diminishes the degree of “double taxation” of dividends, which results when the corporation is first taxed on its income and then when the investor who receives the dividend is also taxed on it. • After-tax cash flow to dividend recipients is much greater at the lower applicable tax rate; the result is noticeably higher dividend payouts by corporations today than prior to passage of the 2003 legislation. • The American Taxpayer Relief Act of 2012, extended the 15% rate on capital gains and dividends for taxpayers in all but the highest tax bracket.

Focus on Practice Capital Gains and Dividend Tax Treatment Extended to 2012 and Beyond for Some • Prior to 2003, dividends were taxed once as part of corporate earnings, and again as the personal income of the investor, in both cases with a potential top rate of 35%. The result was an effective tax rate of 57.75% on some dividends. • Though the 2003 tax law did not completely eliminate the double taxation of dividends, it reduced the maximum possible effect of the double taxation of dividends to 44.75%. For taxpayers in the lower tax brackets, the combined effect was a maximum of 38.25%. • The American Taxpayer Relief Act of 2012 extended the 15% rate for taxpayers in the 25, 28, 33, and 35% income tax brackets. However, individuals making more than $400,000 and couples earning more than $450,000 will now pay 20% on capital gain and dividends. How might the expected future reappearance of higher tax rates on individuals receiving dividends affect corporate dividend payout policies?

Personal Finance Example The board of directors of Espinoza Industries, Inc., on October 4 of the current year, declared a quarterly dividend of $0.46 per share payable to all holders of record on Friday, October 30. They set a payment date of November 19. Rob and Kate Heckman, who purchased 500 shares of Espinoza’s common stock on Thursday, October 15, wish to determine whether they will receive the recently declared dividend and, if so, when and how much they would net after taxes from the dividend given that the dividends would be subject to a 15% federal income tax.

Personal Finance Example (cont.) Given the Friday, October 30 date of record, the stock would begin selling ex dividend 2 business days earlier on Wednesday, October 28. Purchasers of the stock on or before Tuesday, October 27, would receive the right to the dividend. Because the Heckmans purchased the stock on October 15, they would be eligible to receive the dividend of $0.46 per share. Thus, the Heckmans will receive $230 in dividends ($0.46 per share 500 shares), which will be mailed to them on the November 19 payment date. Because they are subject to a 15% federal income tax on the dividends, the Heckmans will net $195.50 [(1 – 0.15) $230] after taxes from the Espinoza Industries dividend.

The Mechanics of Payout Policy: Dividend Reinvestment Plans Dividend reinvestment plans (DRIPs) are plans that enable stockholders to use dividends received on the firm’s stock to acquire additional shares—even fractional shares—at little or no transaction cost. • Some companies even allow investors to make their initial purchases of the firm’s stock directly from the company without going through a broker. • With DRIPs, plan participants typically can acquire shares at about 5 percent below the prevailing market price.

The Mechanics of Payout Policy: Stock Price Reactions to Corporate Payouts What happens to the stock price when a firm pays a dividend or repurchases shares? • In theory, when a stock begins trading ex dividend, the stock price should fall by exactly the amount of the dividend. • In theory, when a firm buys back shares at the going market price, the market price of the stock should remain the same. • In practice, taxes and a variety of other market imperfections may cause the actual change in share price in response to a dividend payment or share repurchase to deviate from what we expect in theory.

Relevance of Payout Policy • The financial literature has reported numerous theories and empirical findings concerning payout policy. • Although this research provides some interesting insights about payout policy, capital budgeting and capital structure decisions are generally considered far more important than payout decisions. • In other words, firms should not sacrifice good investment and financing decisions for a payout policy of questionable importance. • The most important question about payout policy is this: Does payout policy have a significant effect on the value of a firm?

Relevance of Payout Policy: Residual Theory of Dividends The residual theory of dividends is a school of thought that suggests that the dividend paid by a firm should be viewed as a residual—the amount left over after all acceptable investment opportunities have been undertaken.

Relevance of Payout Policy: Residual Theory of Dividends (cont.) Using the residual theory of dividends, the firm would treat the dividend decision in three steps, as follows: • Determine its optimal level of capital expenditures, which would be the level that exploits all of a firm’s positive NPV projects. • Using the optimal capital structure proportions, estimate the total amount of equity financing needed to support the expenditures generated in Step 1. • Because the cost of retained earnings, rr, is less than the cost of new common stock, rn, use retained earnings to meet the equity requirement determined in Step 2. If retained earnings are inadequate to meet this need, sell new common stock. If the available retained earnings are in excess of this need, distribute the surplus amount—the residual—as dividends.

Relevance of Payout Policy: The Dividend Irrelevance Theory The dividend irrelevance theory is Miller and Modigliani’s theory that in a perfect world, the firm’s value is determined solely by the earning power and risk of its assets (investments) and that the manner in which it splits its earnings stream between dividends and internally retained (and reinvested) funds does not affect this value. • In a perfect world (certainty, no taxes, no transactions costs, and no other market imperfections), the value of the firm is unaffected by the distribution of dividends. • Of course, real markets do not satisfy the “perfect markets” assumptions of Modigliani and Miller’s original theory.

Relevance of Payout Policy: The Dividend Irrelevance Theory (cont.) The clientele effect is the argument that different payout policies attract different types of investors but still do not change the value of the firm. • Tax-exempt investors may invest more heavily in firms that pay dividends because they are not affected by the typically higher tax rates on dividends. • Investors who would have to pay higher taxes on dividends may prefer to invest in firms that retain more earnings rather than paying dividends. • If a firm changes its payout policy, the value of the firm will not change—what will change is the type of investor who holds the firm’s shares.

Relevance of Payout Policy: Arguments for Dividend Relevance • Dividend relevance theory is the theory, advanced by Gordon and Lintner, that there is a direct relationship between a firm’s dividend policy and its market value. • The bird-in-the-hand argument is the belief, in support of dividend relevance theory, that investors see current dividends as less risky than future dividends or capital gains.

Relevance of Payout Policy: Arguments for Dividend Relevance (cont.) Studies have shown that large changes in dividends do affect share price. • Informational content is the information provided by the dividends of a firm with respect to future earnings, which causes owners to bid up or down the price of the firm’s stock. • The agency cost theory says that a firm that commits to paying dividends is reassuring shareholders that managers will not waste their money. • Although many other arguments related to dividend relevance have been put forward, empirical studies have not provided evidence that conclusively settles the debate about whether and how payout policy affects firm value.

Factors Affecting Dividend Policy Dividend policy represents the firm’s plan of action to be followed whenever it makes a dividend decision. First consider five factors in establishing a dividend policy: • legal constraints • contractual constraints • the firm’s growth prospects • owner considerations • market considerations

Factors Affecting Dividend Policy: Legal Constraints • Most states prohibit corporations from paying out as cash dividends any portion of the firm’s “legal capital,” which is typically measured by the par value of common stock. • Other states define legal capital to include not only the par value of the common stock, but also any paid-in capital in excess of par. • These capital impairment restrictions are generally established to provide a sufficient equity base to protect creditors’ claims.

Factors Affecting Dividend Policy: Legal Constraints (cont.) In states where the firm’s legal capital is defined as the par value of its common stock, Miller Flour Company could pay out $340,000 ($200,000 + $140,000) in cash dividends without impairing its capital. In states where the firm’s legal capital includes all paid-in capital, the firm could pay out only $140,000 in dividends.

Factors Affecting Dividend Policy: Legal Constraints (cont.) • If a firm has overdue liabilities or is legally insolvent or bankrupt, most states prohibit its payment of cash dividends. • In addition, the Internal Revenue Service prohibits firms from accumulating earnings to reduce the owners’ taxes. • The excess earnings accumulation tax is the tax the IRS levies on retained earnings above $250,000 for most businesses when it determines that the firm has accumulated an excess of earnings to allow owners to delay paying ordinary income taxes on dividends received.

Factors Affecting Dividend Policy: Contractual Constraints • Often the firm’s ability to pay cash dividends is constrained by restrictive provisions in a loan agreement. • Generally, these constraints prohibit the payment of cash dividends until the firm achieves a certain level of earnings, or they may limit dividends to a certain dollar amount or percentage of earnings. • Constraints on dividends help to protect creditors from losses due to the firm’s insolvency.

Factors Affecting Dividend Policy: Growth Prospects • A growth firm is likely to have to depend heavily on internal financing through retained earnings, so it is likely to pay out only a very small percentage of its earnings as dividends. • A more established firm is in a better position to pay out a large proportion of its earnings, particularly if it has ready sources of financing.

Factors Affecting Dividend Policy: Owner Considerations Tax status of a firm’s owners: • If a firm has a large percentage of wealthy stockholders who have sizable incomes, it may decide to pay out a lower percentage of its earnings to allow the owners to delay the payment of taxes until they sell the stock. Owners’ investment opportunities: • If it appears that the owners have better opportunities externally, the firm should pay out a higher percentage of its earnings. Potential dilution of ownership: • If a firm pays out a high percentage of earnings, new equity capital will have to be raised with common stock. The result of a new stock issue may be dilution of both control and earnings for the existing owners.

Factors Affecting Dividend Policy: Market Considerations Catering theory is a theory that says firms cater to the preferences of investors, initiating or increasing dividend payments during periods in which high-dividend stocks are particularly appealing to investors.

Types of Dividend Policies: Constant-Payout-Ratio Dividend Policy • A firm’s dividend payout ratio indicates the percentage of each dollar earned that a firm distributes to the owners in the form of cash. It is calculated by dividing the firm’s cash dividend per share by its earnings per share. • A constant-payout-ratio dividend policy is a dividend policy based on the payment of a certain percentage of earnings to owners in each dividend period.

Types of Dividend Policies: Constant-Payout-Ratio Dividend Policy (cont.) Peachtree Industries, a miner of potassium, has a policy of paying out 40% of earnings in cash dividends. In periods when a loss occurs, the firm’s policy is to pay no cash dividends.

Types of Dividend Policies: Regular Dividend Policy • Regular dividend policy is a dividend policy based on the payment of a fixed-dollar dividend in each period. • A regular dividend policy is often build around a target dividend-payout ratio, which is a dividend policy under which the firm attempts to pay out a certain percentage of earnings as a stated dollar dividend and adjusts that dividend toward a target payout as proven earnings increases occur.

Types of Dividend Policies: Regular Dividend Policy (cont.) The dividend policy of Woodward Laboratories, a producer of a popular artificial sweetener, is to pay dividends of $1.00 per share until per-share earnings have exceeded $4.00 for 3 consecutive years. At that point, the annual dividend is raised to $1.50 per share, and a new earnings plateau is established.

Types of Dividend Policies: Low-Regular-and-Extra Dividend Policy • A low-regular-and-extra dividend policy is a dividend policy based on paying a low regular dividend, supplemented by an additional (“extra”) dividend when earnings are higher than normal in a given period. • An extra dividend is an additional dividend optionally paid by the firm when earnings are higher than normal in a given period.

Other Forms of Dividends A stock dividend is the payment, to existing owners, of a dividend in the form of stock. • In a stock dividend, investors simply receive additional shares in proportion to the shares they already own. • No cash is distributed, and no real value is transferred from the firm to investors. • Instead, because the number of outstanding shares increases, the stock price declines roughly in line with the amount of the stock dividend. • In an accounting sense, the payment of a stock dividend is a shifting of funds between stockholders’ equity accounts rather than an outflow of funds.

Other Forms of Dividends (cont.) The current stockholders’ equity on the balance sheet of Garrison Corporation, a distributor of prefabricated cabinets, is as shown in the following accounts. Preferred stock $300,000 Common stock (100,000 shares @ $4 par) 400,000 Paid-in capital in excess of par 600,000 Retained earnings 700,000 Total stockholders’ equity $2,000,000

Other Forms of Dividends (cont.) Garrison declares a 10% stock dividend when the market price of its stock is $15 per share. The resulting account balances are as follows: Preferred stock $300,000 Common stock (110,000 shares @ $4 par) 440,000 Paid-in capital in excess of par 710,000 Retained earnings 550,000 Total stockholders’ equity $2,000,000

Other Forms of Dividends (cont.) Ms. X owned 10,000 shares of Garrison Corporation’s stock. • The company’s most recent earnings were $220,000, and earnings are not expected to change in the near future. • Before the stock dividend, Ms. X owned 10% of the firm’s stock, which was selling for $15 per share. • Because Ms. X owned 10,000 shares, her earnings were $22,000 ($2.20 per share 10,000 shares). • After receiving the 10% stock dividend, Ms. X has 11,000 shares, which again is 10% of the ownership (11,000 shares ÷ 110,000 shares). • The market price of the stock can be expected to drop to $13.64 per share [$15 (1.00 ÷ 1.10)], which means that the market value of Ms. X’s holdings is $150,000 (11,000 shares $13.64 per share). • The future earnings per share drops to $2.