Download

1 / 122

1.22k likes | 1.32k Views

P a g e | 1 Inter n atio na l A s s oci a t ion of R isk a nd Co mpl i a n c e Pr o f e s s io na l s ( I A RCP) 12 0 0 G St re e t N W Su i t e 8 0 0 W a s h i ng t o n, D C 2 000 5 - 67 0 5 U SA T e l : 2 0 2 - 44 9 - 9750 www .ri s k - c ompl i ance-a ss o c i a tion . c om.

E N D

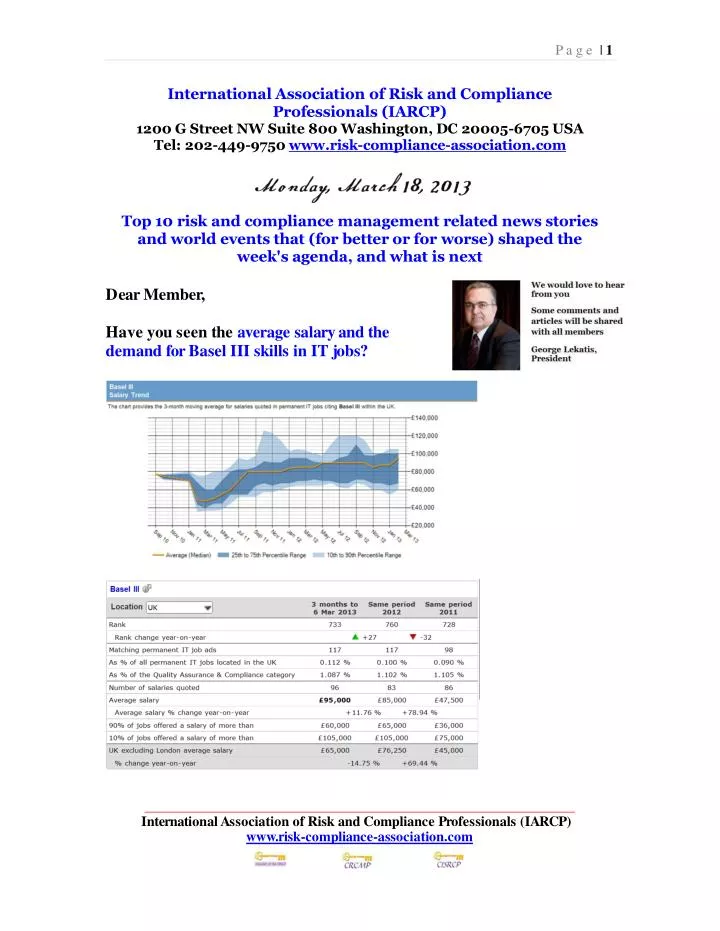

P age |1 InternationalAssociationofRiskandComplianceProfessionals(IARCP) 1200GStreet NWSuite800Washington,DC20005-6705USATel:202-449-9750www.risk-compliance-association.com Top10riskandcompliancemanagementrelatednewsstoriesandworldeventsthat(forbetterorforworse)shapedthe week'sagenda,andwhatisnext DearMember, HaveyouseentheaveragesalaryandthedemandforBaselIIIskillsin ITjobs? InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |2 Source:ITJobsWatch,thatprovidesauniqueperspectiveontoday'sinformation technologyjobmarket(noaffiliation). ReadmoreatNumber1blow. Also,areyougoodindisastermanagement? Accordingto PenttiHakkarainen,DeputyGovernoroftheBankofFinland,oneaspectofdisastermanagementiskeepingparticularlyriskyorvulnerablebusinessin aseparatelegalunitthusmakingiteasiertodivest/withdrawwithoutexposingtherestoftheoperationsforcontagion bycuttinglinkagesrapidly. Readmoreatnumber3below.Welcome totheTop10list. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |3 Amazing:Theaveragesalaryandthedemandfor BaselIII skillsinITjobsadvertisedacrosstheUK ThetablelooksatthedemandforBaselIIIskillsin ITjobsadvertisedacrosstheUK. IncludedisaguidetotheaveragesalariesofferedinITjobsthathavecitedBaselIIIoverthe3months to 6March2013withacomparison tothesameperiodintheprevious2years. Long-terminterestrates SpeechbyMrBenSBernanke,ChairmanoftheBoardofGovernorsoftheFederalReserveSystem,attheAnnualMonetary/MacroeconomicsConference“The pastandfutureofmonetarypolicy”,sponsored bytheFederalReserveBankofSanFrancisco,SanFrancisco,California Re-evaluatingtheuniversalbankingmodel:CantheVolcker,VickersorLiikanenrulesmakebankssafer? RemarksbyMrPenttiHakkarainen,DeputyGovernoroftheBankofFinland,atthe4th FutureofBankingSummit,organisedbyEconomistConferences,Paris InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |4 Reflectionsonreputationand itsconsequences Speechby MsSarahBloomRaskin,MemberoftheBoardofGovernorsoftheFederalReserveSystem,atthe2013BankingOutlookConference,FederalReserveBankofAtlanta,Atlanta,Georgia OpinionoftheEuropeanInsuranceandOccupationalPensionsAuthorityonSupervisoryResponsetoa ProlongedLow InterestRateEnvironment InvestigationsbytheFinancialSupervisoryAuthorityintoissuesconnectedwiththebankingcollapsehavenowconcluded Investigationsbythe FinancialSupervisoryAuthority(FME)intothe eventsprecedingthebankingcollapseintheautumnof2008,which beganimmediatelyfollowingthefailureofthethreelargecommercialbanks,havenowconcluded. FMEinvestigatedatotalof205cases. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |5 Averyinterestingpresentation Icelandspre-andpost-crisisexperience SECURITIES ANDEXCHANGECOMMISSION Noticeof FilingofProposed RuleChangetoRequirethatListedCompaniesHaveanInternalAuditFunction Pursuant toSection19(b)(1)oftheSecuritiesExchangeActof1934(“Act”)andRule19b-4thereunder,noticeisherebygiventhaton February20,2013,TheNASDAQStockMarketLLC(“Nasdaq”or“Exchange”)filed withtheSecuritiesandExchangeCommission(“Commission”)theproposedrulechangeasdescribedinItemsI,II,andIIIbelow,whichItemshavebeenpreparedbytheExchange. TheEuropeancrisisandthedevelopmentoftheEuropeanUnion SpeechbyMrLarsRohde,GovernoroftheNationalBankofDenmark,attheEuropeanAffairsCommittee’sconsultation:“TheEuropeancrisisand thedevelopmentoftheEuropean Union”,formerUpperChamberoftheDanishParliament,Copenhagen InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |6 PromotinganinclusivefinancialsectorinPakistan SpeechbyMrYaseenAnwar,GovernoroftheStateBankofPakistan,attheClosureCeremonyofTermSarmayaCertificate(TFC)issuedbyTameerMicrofinanceBank,Karachi InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |7 Amazing:TheaveragesalaryandthedemandforBaselIIIskillsinITjobsadvertisedacrosstheUK ThefirsttablebelowlooksatthedemandforBaselIIIskillsin ITjobsadvertisedacrosstheUK. IncludedisaguidetotheaveragesalariesofferedinITjobsthathavecitedBaselIIIoverthe3months to 6March2013withacomparison tothesameperiodintheprevious2years. ThesecondtableisforcomparisonandprovidesaggregatesforalloftheQualityAssurance&Compliancecategory. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |8 InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |9 Source:ITJobsWatch,thatprovidesauniqueperspectiveontoday'sinformation technologyjobmarket(noaffiliation). Tolearnmore:http://www.itjobswatch.co.uk/jobs/uk/basel%20iii.do InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |10 Long-terminterestrates SpeechbyMrBenSBernanke,ChairmanoftheBoardofGovernorsoftheFederalReserveSystem,attheAnnualMonetary/MacroeconomicsConference “Thepastandfutureofmonetarypolicy”,sponsoredbythe FederalReserveBankofSanFrancisco,SanFrancisco,California Iwillbeginmyremarksbyposingaquestion:Whyarelong-terminterestratessolowintheUnitedStatesandinothermajorindustrialcountries? Atfirstblush,theanswerseemsobvious:Centralbanksinthosecountriesarepursuingaccommodativemonetarypolicies to boostgrowthand reduceslackintheireconomies. However,whilecentralbanks certainlyplayakeyrolein determiningthebehavioroflong-terminterestrates,theirsisonlyaproximateinfluence. Amorecompleteexplanationofthecurrentlow levelofratesmusttakeaccountofthebroadereconomicenvironmentinwhichcentralbanks arecurrentlyoperatingandoftheconstraintsthatthatenvironmentplacesontheirpolicychoices. Letmestartwithabriefoverviewoftherecenthistoryoflong-terminterestratesinsomekeyeconomies. Chart1showsthe10-yeargovernmentbondyieldsforfivemajorindustrialcountries:Canada,Germany,Japan,theUnitedKingdom,andtheUnitedStates. Notethatthemovementsintheseyieldsarequitecorrelateddespitesomedifferencesintheeconomiccircumstancesandcentralbankmandatesinthosecountries. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |11 Further,withthenotableexceptionofJapan,thelevelsoftheyieldshavebeenverysimilar– indeed,strikinglyso,withlong-term yieldsdecliningovertimeandcurrentlycloseto2percentin eachcase. Thesimilarbehavioroftheseyieldsattests totheglobalnatureoftheeconomicandfinancialdevelopmentsofrecentyears,aswellas to thebroadsimilarityinhow themonetarypolicymakersintheadvancedeconomieshaveresponded tothesedevelopments. Ofcourse,Japaneseyieldsareclearlyacaseapart,asJapanhasenduredanextendedperiodofdeflation,whileinflationintheotherfourcountrieshasbeenpositive andgenerallyclose tothestatedobjectivesofthemonetaryauthorities. ButevenJapaneseyieldshaveshownsome tendencytofluctuatealongwith otherbenchmarkyields,andtheyhavealsodeclinedovertheperiodshown. In mycomments,Iwilldelvemoredeeplyintothereasonswhytheselong-terminterestrateshavefallensolow. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |12 Thisexaminationmaybeuseful bothforunderstandingthecurrentstanceofpolicy andalsoforthinkingabouthow ratesmayevolve. Inshort,weexpectthatastheeconomyrecovers,long-termrateswillriseovertimetomorenormallevels. Areturntomorenormalconditionsinfinancialmarketswould,ofcourse,bemostwelcome. Manycommentatorshavenoted,however,thatbothanextendedperiod oflow ratesandthetransitionbacktowardnormallevelsmayposeriskstofinancialstability. In thefinalportionofmyremarks,IwilldiscusssomeaspectsofhowtheFederalReserveisapproachingtheserisks. Whyarelong-terminterestratessolow? So,whyarelong-terminterestratescurrentlysolow? Tohelpanswerthisquestion,itisusefultodecomposelonger-termyieldsintothreecomponents: Onereflectingexpectedinflationoverthe termofthesecurity; Anothercapturingtheexpectedpathofshort-termreal,orinflation-adjusted,interestrates; Andaresidualcomponentknownasthetermpremium. Ofcourse,noneofthesethreecomponentsisobserveddirectly,buttherearestandardwaysofestimatingthem. Chart2displaysoneversionofthisdecompositionofthe10-yearU.S. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |13 TreasuryyieldbasedonatermstructuremodeldevelopedbyFederalReservestaff. ThebroadfeaturesIwillemphasizearesimilarto thosefoundbyotherauthorsusingavarietyofmethods. Allthreecomponentsofthe10-yearyieldhavedeclinedsince2007. Thedecompositionattributesmuchofthedeclineintheyieldsince2010toasharpfall in thetermpremium,buttheexpectedshort-termrealratecomponentalsomoveddownsignificantly. Let’sconsidereachcomponentmoreclosely. Theexpectedinflationcomponenthasdriftedgraduallydownwardformanyyearsandhasbecomequitestable. In largepart,thedownwardtrendandstabilizationofexpectedinflationintheUnitedStatesareproductsoftheincreasingcredibilityoftheFederalReserve’scommitment topricestability. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |14 In January2012,theFederalOpenMarketCommittee(FOMC)underscoredthiscommitmentbyissuingastatement– sincereaffirmedatitsJanuary2013meeting– onitslonger-rungoalsandpolicystrategy,whichincludedalonger-runinflationtargetof2percent. The anchoringoflong-terminflationexpectationsnear2percenthasbeenakeyfactor influencinglong-terminterestratesoverrecentyears. Italmostcertainlyhelpedmitigatethestrongdisinflationarypressuresimmediatelyfollowingthecrisis. WhileIhavenotshownexpectedinflationforotheradvancedeconomies,thepictureswouldbeverysimilar– again,exceptforJapan. Withtheexpectedinflationcomponentofthe10-yearratenear2percentandtherateitselfabitbelow2percentrecently,itisclearthatthecombinationoftheothertwo components–theexpectedpathof short-termrealinterestratesandthetermpremium–mustmakeasmall netnegativecontribution. Theexpectedpathofshort-termrealinterestratesis,ofcourse,influencedbymonetarypolicy,boththecurrentstanceofpolicy andmarketparticipants’expectationsofhowpolicywillevolve. Thestanceofmonetarypolicy atanygiventime,inturn,isdrivenlargelybytheeconomicoutlook,theriskssurroundingthatoutlook,andattimesotherfactors,suchaswhetherthezerolowerboundonnominal interestratesisbinding. In thecurrentenvironment,bothpolicymakersandmarketparticipantswidelyagreethatsupportingtheU.S.economicrecoverywhilekeepinginflationcloseto2percentwilllikelyrequirerealshorttermrates,currentlynegative,toremainlow forsometime. Asshowninchart2,theexpectedaverageoftheshort-termrealrateoverthenext10yearshasgraduallydeclinedtonearzerooverthepastfewyears,inpartreflecting downwardrevisionsinexpectationsaboutthe InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |15 paceoftheongoingrecoveryand,hence,apushingoutofexpectationsregardinghow longnominalshort-termrateswillremainlow. Asthepersistenceoftheeffectsofthecrisishavebecomeclearer,theFederalReserve’scommunicationshavereinforcedtheexpectationthatconditionsarelikelytowarranthighlyaccommodativepolicyforsometime: Mostrecently,the FOMCindicatedthatitexpectstomaintainanexceptionallylow levelofthefederalfundsrateatleastaslongastheunemploymentrateisabove6.5percent,projectedinflationbetweenoneandtwo yearsaheadisnomorethanahalfpercentagepointabovetheCommittee’s2percenttarget,andlong-terminflationexpectationsremainstable. In discussingtheroleofmonetarypolicy in determiningtheexpectedfuturepathofrealshort-termrates,Ihavecheatedalittle: Whatmonetarypolicyactuallycontrolsisnominalshort-termrates. However,becauseinflationadjustsslowly,controlofnominalshort-term ratesusuallytranslatesintocontrolofrealshort-termratesovertheshortandmediumterm. In thelongerterm,realinterestratesaredeterminedprimarilybynonmonetaryfactors,suchastheexpectedreturnto capitalinvestments,whichinturniscloselyrelatedtotheunderlyingstrengthoftheeconomy. Thefactthatmarketyieldscurrentlyincorporateanexpectationofverylow short-termrealinterestratesoverthenext10yearssuggeststhatmarketparticipantsanticipatepersistentlyslowgrowthand,consequently,low realreturns toinvestment. In otherwords,thelow levelofexpectedrealshortratesmayreflectnotonlyinvestorexpectationsforaslow cyclicalrecoverybutalsosomedowngradingoflonger-termgrowthprospects. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |16 Chart3,whichdisplays yieldsoninflation-indexed,long-termgovernmentbondsforthesamefivecountriesrepresentedinchart1,showsthatexpectedrealyieldsoverthelongertermarelow in otheradvancedindustrialeconomiesaswell. Noteagainthestrongsimilarityinreturnsacrosstheseeconomies,suggestingonceagaintheimportanceofcommonglobalfactors. Whileindexedyieldsspikeduparoundtheendof2008,reflectingmarketstressesattheheightofthecrisisthatundercutthedemandforthesebonds,theseeffectsdissipatedin 2009. Sincethattime,inflation-indexedyieldshavedeclinedsteadilyandnowstandbelowzeroineachcountry. Apparently,low longer-termrealrateexpectationsareplayinganimportantrolein accountingforlow 10-yearnominalratesin otherindustrialcountries,aswellasintheUnitedStates. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |17 Thethirdandfinalcomponentofthelong-terminterestrateis thetermpremium,definedastheresidualcomponentnotcapturedbyexpectedrealshort-termratesorexpectedinflation. AsInoted,thelargestportionofthedownwardmoveinlong-termratessince2010appearstobeduetoafall in the termpremium,soitdeservessomespecialdiscussion. Ingeneral,thetermpremiumistheextrareturninvestorsexpecttoobtainfromholdinglongtermbondsasopposedto holdingandrollingoverasequenceofshort-termsecuritiesoverthesameperiod. In part,thetermpremiumcompensatesbondholdersfor interestraterisk – therisk ofcapitalgainsandlossesthatinterestratechangesimplyforthevalueoflongertermbonds. Two changesinthenatureofthisinterestrateriskhaveprobablycontributedtoageneral downwardmovementofthe termpremiumin recentyears. First,thevolatilityofTreasuryyieldshasdeclined, in partbecauseshort-termratesarepressedupagainstthezerolowerboundandareexpectedtoremainthereforsometimetocome. Second,thecorrelationofbondpricesandstock priceshasbecomeincreasinglynegative overtime,implyingthatbondshavebecomemorevaluableasahedgeagainstrisksfromholdingotherassets. Beyondinterestraterisk,anumberofotherfactorsalsoaffectthe termpremiuminpractice. Forexample,duringperiodsoffinancialturmoil,thepricesoflonger-termTreasurysecuritiesareoftendrivenupbyso-calledsafe-havendemandsofinvestorswhoplacespecialvalueonthesafetyandliquidityofTreasurysecurities. Indeed,evenduringmoreplacidperiods,globaldemandsforsafeassetsincreasethevalueofTreasurysecurities. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |18 Manyforeigngovernmentsandcentralbanks,particularlythosewithsustainedcurrentaccountsurpluses,holdsubstantialinternationalreservesintheformofTreasuries. ForeignholdingsofU.S.Treasurysecuritiescurrentlyamount to about $5-1/2trillion,roughlyhalfofthe totalamountofmarketableTreasurydebtoutstanding. Theglobaleconomicandfinancialstressesofrecentyears–triggeredfirstbythefinancialcrisis,andthenbytheproblemsintheeuroarea – appeartohavesignificantlyelevatedthe safe-havendemandfor Treasurysecuritiesattimes,pushingdownTreasuryyieldsandimplyingalower,orevenanegative,termpremium. FederalReserveactionshavealsoaffectedtermpremiumsinrecentyears,mostprominentlythroughaseriesofLarge-ScaleAssetPurchase(LSAP)programs. Theseprogramsconsistofopenmarketpurchasesofagencydebt,agencymortgage-backedsecurities,andlongertermTreasurysecurities. TotheextentthatTreasurysecuritiesandagency-guaranteedsecuritiesarenotperfectsubstitutesforotherassets,FederalReservepurchasesoftheseassetsshouldlowertheirtermpremiums,putting downward pressureonlonger-terminterestratesandeasingfinancialconditionsmorebroadly. Althoughestimatedeffectsvary,agrowingbodyofresearchsupportstheviewthatLSAPsareeffectiveatbringingdowntermpremiumsandthusreducinglonger-termrates. Ofcourse,theFederalReservehasusedthisunconventionalapproachtoloweringlonger-termratesbecause,withshort-termratesnearzero,itcannolongeruseitsconventionalapproachofcuttingthetargetforthefederalfundsrate. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |19 Accordingly,thisportionofthedeclineinthe termpremiummightultimatelybeattributedtothesluggisheconomicrecovery,which promptedadditionalpolicy actionfromtheFederalReserve. Let’srecap. Long-terminterestratesarethesumofexpectedinflation,expectedrealshortterminterestrates,andatermpremium. Expectedinflationhasbeenlow andstable,reflectingcentralbankmandatesandcredibilityaswellasconsiderableresourceslackinthemajorindustrialeconomies. Real interestratesareexpected to remainlow,reflectingtheweaknessoftherecoveryinadvancedeconomies (andpossiblysomedowngradingoflonger-termgrowthprospectsaswell). Thisweakness,allelsebeingequal, dictatesthatmonetarypolicy mustremainaccommodativeifitis to supporttherecoveryandreducedisinflationaryrisks. Putanotherway,atthepresenttimethemajorindustrialeconomiesapparently cannotsustainsignificantlyhigherrealratesofreturn; in thatrespect,centralbanks – solongastheyaremeetingtheirpricestabilitymandates– havelittlechoicebuttotakeactionsthatkeepnominal long-termratesrelativelylow,assuggestedby thesimilarityinthelevelsoftheratesshowninchart1. Finally,termpremiumsarelow ornegative,reflectingahostoffactors,includingcentralbankactionsinsupportofeconomicrecovery. Thus,whilethecurrentconstellationoflong-termratesacrossmanyadvancedcountrieshasfewprecedents,itisnotpuzzling: Itfollowsnaturallyfromtheeconomiccircumstancesof thesecountriesandtheimplicationsofthesecircumstancesforthepoliciesoftheircentralbanks. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |20 Howare long-termrateslikelytoevolve? So, how arelong-termrateslikelytoevolveovercomingyears? Itisworthpausingtonotethat,notthatlongago,centralbankerswould havecarefullyavoidedthistopic. However,itisnow abedrock principleofcentralbankingthattransparencyaboutthelikelypathofpolicy,ingeneral,andinterestrates,inparticular,canincreasetheeffectivenessofpolicy. In thepresentcontext,Iwouldaddthattransparencymaymitigaterisksemanatingfromunexpectedratemovements. Thus,letmeturntoprospectsforlong-termrates,startingwiththeexpectedpathofratesandthenturningto deviationsfromtheexpectedpaththatmayarise. If,astheFOMCanticipates,theeconomicrecoverycontinuesatamoderatepace,withunemploymentslowlydecliningandinflationexpectationsremainingnear2percent,thenlong-terminterestrateswouldbeexpectedtorisegraduallytowardmorenormallevelsoverthenextseveralyears. Thisrisewouldoccurasthemarket’sviewoftheexpecteddateatwhichtheFederalReservewillbegintheremovalofpolicy accommodationdrawsnearerandthenasaccommodationisremoved. Somenormalizationofthetermpremiummightalsocontribute to ariseinlong-termrates. Toillustratepossiblepaths,Chart4displaysfourdifferentforecastsoftheevolutionofthe10-yearTreasuryyieldovercomingyears. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |21 TheblacklineistheforecastreportedintheDecember2012BlueChipFinancialForecastssurvey. ThegreenlinegivestheCongressionalBudgetOfficeforecastpublishedinFebruary,andthebluelinepresentsthemedianfromtheSurveyofProfessionalForecasters,asreportedinthefirstquarterofthisyear. Finally,thepurplelineshowsaforecastbasedonthe termstructuremodelusedforthedecompositionofthe10-yearyieldin chart2. Whiletheseforecastsembodyawiderangeofunderlyingmodelsandassumptions,thebasicmessageisclear– long-terminterestratesareexpectedtorisegraduallyoverthenextfewyears,rising(atleastaccordingtotheseforecasts)toaround3percentattheendof2014. Theforecastsinchart4implyatotalincreaseofbetween200and300basispointsinlong-termyieldsbetweennow and2017. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |22 Ofcourse,theforecastsinchart4arejustforecasts,andrealitymightwellturnout tobedifferent. Chart5providesthreecomplementaryapproachestosummarizingtheuncertaintysurroundingforecastsoflong-termrates. ThedarkgraybarsinthechartarebasedontherangeofforecastsreportedintheBlueChipFinancialForecasts,thebluebarsarebasedonthehistoricaluncertaintyregardinglong-terminterestratesasreflectedintheBoardstaff’sFRB/USmodeloftheU.S.economy,andtheorangebarsgiveamarket-basedmeasureofuncertaintyderivedfromswaptions. Thesethreedifferentmeasuresgiveabroadlysimilarpictureabouttheupsideanddownsideriskstotheforecastsoflong-termrates. Rates100basispointshigherthantheexpectedpathsinchart4by2014arecertainlyplausibleoutcomesasjudgedbyeachofthethreemeasures,andthisuncertaintygrowsto asmuchas175basispointsby2017. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |23 Note,though,thatwhiletherisk ofanunexpectedriseininterestrateshasdrawnmuchattention,theleveloflong-terminterestratesalsocould provetobelowerthanforecast. Indeed,bythemeasuresshowninchart5,theupsideanddownsideriskstothelevelofratesareroughlysymmetricasof2017. Wealsohavesomehistoricalexperiencewithincreasesin ratesduringtighteningcycles toconsider. Forexample,in1994,10-yearTreasuryyieldsroseabout220basispointsoverthecourseofayear,reflectinganunexpectedquickeninginthepaceofeconomicgrowthandsignsofbuildinginflationpressures. Thisincreasein long-termratesappearsto havereflectedamixofapronouncedriseintheexpectedpathofthepolicy interestrateandsomeincreaseinthe termpremium. Ariseofmorethan200basispointsinayearisattheupperendofwhatisimpliedbythemeanpathsanduncertaintymeasuresshownincharts4and5,butthesemeasuresstilladmitasubstantialprobabilityofhigher– andlower– paths. Overall,then,weanticipatethatlong-termrateswillriseastherecoveryprogressesandexpectedshort-termrealratesandtermpremiumsreturntomorenormallevels. Theprecisetimingandpaceoftheincreasewilldependimportantlyonhow economicconditionsdevelop,however,andissubjecttoconsiderabletwo-sideduncertainty. Managingrisks associatedwiththefuturecourseoflong-terminterestrates AsInotedwhenIbeganmyremarks,onereasontofocusonthetimingandpaceofapossibleincreasein long-termratesisthattheseoutcomesmayhaveimplicationsforfinancialstability. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |24 Commentatorshaveraisedtwobroadconcernssurroundingtheoutlookforlong-termrates. Tooversimplify,thefirstriskisthatrateswillremainlow,andthesecondisthattheywillnot. In particular,inanenvironmentofpersistentlylow returns,incentivesmaygrowforsomeinvestors to engageinanunsafe “reachforyield”eitherthroughexcessiveuseofleverageorthroughotherformsofrisk-taking. MyBoardcolleagueJeremySteinrecentlydiscussedhowthisbehaviormayarisein somefinancialmarkets,includingcreditmarkets. Alternatively,wefaceariskthatlonger-termrateswillrisesharplyatsomepoint,imposingcapitallossesonholdersoffixed-incomeinstruments,includingfinancialinstitutions. Ofcourse,thetworisksmayverywellbemutuallyreinforcing: Takingondurationrisk isonewayinvestorsmayreachforyield,andthelossesresultingfromasharpriseinlonger-termrateswillbegreaterifinvestorshavedoneso. Onemightarguethattherightresponseto theserisksistotightenmonetarypolicy,raisinglong-terminterestrateswiththeaimofforestallinganyundesirablebuildupofrisk. Ihopemydiscussionthiseveninghasconvincedyouthat,atleastineconomiccircumstancesofthesortthatprevailtoday,suchanapproachcouldbequitecostlyandmightwellbecounterproductivefromthestandpointofpromotingfinancialstability. Long-terminterestratesinthemajorindustrialcountriesarelowforgoodreason:Inflationislow andstableand,givenexpectationsofweakgrowth,expectedrealshortratesarelow. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |25 Prematurerateincreaseswouldcarryahighrisk ofshort-circuitingtherecovery,possiblyleading– ironicallyenough– toanevenlongerperiodoflow long-termrates. Onlyastrongeconomycandeliverpersistentlyhighrealreturnstosaversandinvestors,andtheeconomiesofthemajorindustrialcountriesarestillintherecoveryphase. Sohowcanfinancialstabilityconcerns–whichtheFederalReservetakesveryseriously–beaddressed? Ourstrategy,undertakenincooperationwithotherregulatorsandcentralbanks,hasanumberofelements. First,wehavegreatlyincreasedourmacroprudentialoversight,withaparticularfocusonpotentialsystemicvulnerabilities,includingbuildupsofleverageandunstablefundingpatternsaswellasinterestraterisk. UndertheumbrellaofourinterdisciplinaryLargeInstitutionsSupervisionCoordinatingCommittee,wepayspecialattention todevelopmentsatthelargest,mostcomplexfinancialfirms,makinguseofinformationgatheredin oursupervisionoftheinstitutionsanddrawnfromfinancialmarketindicatorsoftheirhealthandsystemicvulnerability. Wealsomonitortheshadowbankingsector,especiallyitsinteractionwithregulatedinstitutions;inthiswork,welookforfactorsthatmayleavethesystemvulnerable to anadverse“firesale”dynamic,inwhichdecliningassetvaluescouldforceleveragedinvestors to sellassets,depressingpricesfurther. Weexchangeinformationregularlywithotherregulatoryagencies,both directlyandundertheauspicesoftheFinancialStabilityOversightCouncil. ThroughouttheFederalReserveSystem,work in theseareasisconductedbyexpertsinbanking,financialmarkets,monetarypolicy,andotherdisciplines,andattheFederalReserveBoardwehaveestablished InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |26 ourOfficeforFinancialStabilityPolicyandResearchtohelpcoordinatethiswork. FindingsarepresentedregularlytotheBoardandtotheFOMCforuseinitsmonetarypolicydeliberations. Second,recognizingthatourmonitoringofthefinancialsectorwillalwaysbeimperfect,weareusingregulatoryandsupervisorytoolstohelpensurethatfinancialinstitutionsaresufficientlyresilienttoweatherlossesandperiodsofmarketturmoilarisingfromanysource. Indeed,reflectingexpectationsembodiedinthenewBaselIIIand Dodd-Frankstandards,thelargestandmostcomplexfinancialfirmshavesubstantiallyincreasedboththeir capitalandtheirliquidityinrecentyears. Ourcurrentroundofstresstestingofthelargestbankholdingcompanies,tobecompletedearly thismonth,examineswhetherthelargestbankingfirmshavesufficient capitalto comethroughaseriouslyadverseeconomicdownturnandstillhavethe capacitytoperformtheirrolesasprovidersofcredit. In arelatedexercise,wearealsoaskingbankstostress-testthe adequacyoftheircapitalinthefaceofahypotheticalsharpupwardshiftintheterm structureofinterestrates. Third,ourapproachto communicatingandimplementingmonetarypolicyprovidestheFederalReservewithnewtoolsthatcouldpotentiallybeused to mitigatetherisk ofsharpincreasesininterestrates. In 1994–theperioddiscussedearlierinwhichsharpincreasesin interestratesstrainedfinancialmarkets– theFOMC’scommunicationtoolswereverylimited; indeed,ithadjustbegunissuingpublicstatementsfollowingpolicy moves. Bycontrast,inrecentyears,theFederalReservehasprovidedagreatdeal ofadditional information aboutitsexpectationsforthepathoftheeconomyandthestanceofmonetarypolicy. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |27 Mostrecently,asImentioned,theFOMCannouncedunemploymentandinflationthresholdscharacterizingconditionsthatwillguidethetimingofthefirstincreaseinthetargetforthefederalfundsrate. Further,theFOMCstatedthatahighlyaccommodativestanceofmonetarypolicy islikely to remainappropriateforaconsiderabletimeafterourcurrentassetpurchaseprogramends. Byprovidinggreaterclarityconcerningthelikelycourseofthe federalfundsrate,FOMCcommunicationshouldbothmakepolicymoreeffectiveandreducetherisk thatmarketmisperceptionsoftheCommittee’sintentionswouldleadtounnecessaryinterestratevolatility. In addition,theFederalReservecould,ifnecessary,useitsbalancesheet toolstomitigatetherisk ofasharpriseinrates. Forexample,theCommitteehasindicateditsintentiontosellitsagencysecuritiesgraduallyonceconditionswarrant. TheCommitteealsonoted,however,thatthepaceofsalescouldbeadjustedupordown in responsetomaterialchangesin eithertheeconomicoutlookorfinancialconditions. In particular,adjustmentstothepaceortimingofassetsalescouldbeused,undersomecircumstances,todampenexcessivelysharpadjustmentsinlonger-terminterestrates. Conclusion Letmefinishwithsomethoughtsonbalancingtheriskswefaceinthecurrentchallengingeconomicenvironment,atatimewhenourmain policytool,thefederalfundsrate,isnearitseffectivelowerbound. Ontheonehand,theFed’sdualmandate hasledustoprovidestrongsupportfortherecovery, both topromotemaximumemploymentandtokeepinflationfromfalling below ourpricestability objective. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |28 Onepurposeofthissupportistopromptareturntotheproductiverisk-takingthatisessentialtorobustgrowthand to gettingtheunemployedbacktowork. Ontheotherhand,wemustbemindfulofthepossibilitythatsustained periodsoflow interestratesandhighlyaccommodativepolicycouldleadtoexcessiverisk-taking insomefinancialmarkets.Thebalancehereisnotaneasyone to strike. Whiletherecentcrisisisvividtestamenttothecostsofill-judged risk-taking,wemustalsobeawareofconstraintsposedbythepresentstateoftheeconomy. Inlightofthemoderatepaceoftherecoveryandthecontinuedhighlevelofeconomicslack,dialingbackaccommodationwiththegoalof deterringexcessiverisk-takinginsomeareasposesitsownriskstogrowth,pricestability,and,ultimately,financialstability. Indeed,asInoted,aprematureremovalofaccommodationcould,byslowingtheeconomy,perverselyserve toextendtheperiodoflowlong-termrates. Forthesereasons,wearerespondingto financialstabilityconcernswiththemultiprongedapproachIsummarizedamomentago,whichreliesprimarilyonmonitoring,supervisionandregulation,andcommunication. Wewill, however,beevaluatingtheseissuescarefullyandonanongoingbasis;wewillbealertforanydevelopmentsthatposerisks totheachievementoftheFederalReserve’smandatedobjectivesofpricestabilityandmaximumemployment;andwewill,ofcourse,remain preparedtouseallofourtoolsasneededtoaddressanysuch developments. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |29 • Re-evaluatingtheuniversalbankingmodel:CantheVolcker,VickersorLiikanenrulesmakebankssafer? • RemarksbyMrPenttiHakkarainen,DeputyGovernoroftheBankofFinland,atthe4thFutureofBankingSummit,organisedbyEconomistConferences,Paris • Thoughtsonthereasonswhytheuniversalbankmodelexists,i.e.whyitisvaluable • “Therearebenefitsfromcombiningdifferentbusinesslinesunderoneroof” • Thereareanumberofreasonswhybankscombineseveralbusinesslinesunderoneroof: • striveforoptimaluseofcapital • diversificationofriskasdistributionofprofitsandlossesofdifferentbusinesslinesarelessthanfullycorrelated • synergiesfromcombinationofdifferentexpertises • servicingthemultipleneedsofclients,especiallyinthecaseofcorporateclients(one-stop-shopping) • Thereisnow onewayofstructuringauniversalbank. • E.g.someuniversalbankshavenumerousbusinesslinesunderonelegalunit,whereasotheruniversalbanksoperateasaholdinggroupofseparatecompanies. • Thebusinesslinesorlegalunits canbedefinedbasedone.g.businessareasorfunctionsand/orgeographicalreach. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |30 • Thewaybanksaimtobestructurediscrystallisedinthestrategy,bute.g.M&Ahistoryandabilitytoachieveorganicgrowthhashadagreatimpactonhowuniversalbanks arestructuredtoday. • “However,somebanksalreadyseethevalueofapplyingauniversalbankmodelwherevariousbusinessactivitiesareclearlystructuredand businesslinesarelegallyseparated” • Evenwithoutregulationrequiringso,manybanksalreadymanagedifferentbusinesslinesseparately,whichcloselyresemblesastructurewithdifferentlegalunits. • Banksfindmanagement,riskmanagementandHR/recruitingeasierifthebusinessisseparatedalonglogicalunits,i.e.functions/activitieswhichfallnaturallytogether. • Fromarisk managementperspective,portfoliosarealreadymanagedseparately. • In some casesanimportantdriverforlegalseparationofbusinessesis“Disastermanagement”,i.e.keepingparticularlyriskyorvulnerablebusinessinaseparatelegalunitthusmakingiteasiertodivest/withdrawwithoutexposingtherestoftheoperationsforcontagionbycuttinglinkagesrapidly. • Therearealsobenefitsofbeingorganisedalongseparatedbusinesslines. • Thepricingofinternalfundingofbusinessunits canbearrangedatarm’slengthwithrisk-adjustedtransferpricing. • Allocationofeconomiccapitalcanbedonebybusinesslineandevenat thelevelofindividualcustomers,whichsupportdecisionmakingandcarryingoutthebusinessinanoptimalway. • “Makingthestructureofuniversalbanksclearerwouldsimplifythegovernanceofbanksandimproveriskmanagement.” InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |31 • Ihavesomeinsightsfrompracticeonwhattheconsequencesoflegalseparationofbusinesslinescouldbe. • In myviewlegalseparationwouldbenefitinparticularthegovernanceandriskmanagementofbanks. • AstheHLEGreportstates,Ihavealsoexperiencedthattheculturesoftraditionalretailbankingandinvestmentbanking/tradingactivitiesareverydifferentandblendedculturescancauseproblems. • Thenatureofthebusinessandtheattitude towardsrisk-takingaredifferent. • In investmentbankingandtradingactivitiesprofitsaregeneratedbyactivelyseekingrisk-takingopportunitiesbyopeningriskypositions. • Whethertheserisk exposureshadgoodrisk-adjustedreturnprospects,hasoftenbeenofsecondaryimportance. • Modelsandwarningsignsflaggedbyriskmanagementwereoftendisregarded;highrisks weretakeneveniftheprobabilityofsuccesswaslow andthepotentialdownsidewassignificant. • In traditionalretailbanking,profitsaremainlyearnedfrominterestratemarginincomefromlongtermcustomerrelationshipsinamorestablemanner. • Creditqualityassessmentandpricingpolicy lieatthecoreofthebusiness. • Alsothetimehorizondiffersmarkedly. • In thetradingactivitytheresultssettledandassessedeverysingleday.Inretailbankingprofitsaregeneratedoverseveralyearstimeperiod. • Theresponsibilityandindependenceofthemanagementisenhancedifbusinesslinesareseparatedtolegalentities. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |32 • Separationalsofacilitatesmanagement,risk managementandHR/recruiting,astheobjectiveandneedsareclearerinaseparatelydefinedbusinessunit. • Aligningincentivestothestrategyofthebusinesslinebymeansoftargetsincludedin remunerationschemeswillalsobe easier. • Iftheoperationstobeseparatedarelogicalunitsthenitismostprobablethatrequiredreportingsystems to supportgovernancearealreadyinplace. • Separationwillalsofacilitatemonitoringbyexternalstakeholdersthusimprovingmarketdiscipline,which canbeseenasanextensiontotheinternalcorporategovernancemechanisms. • Specifically,separationmayimprovetransparencyandreduceuncertaintyaboutthequalityofbanks asaninvestmentopportunity thusfacilitatingpricingoftheseparatedparts. • This,ontheotherhand, wouldimprovetheaccess tomarketfundingamongaboveaveragequalitybanks • Moreovermakingthestructureofuniversalbanksclearerthroughseparationofbusinessesalsofacilitatesthetask ofsupervisorsandauthoritiesresponsibleforresolution. • Separationwillcertainlyfacilitatetheapplicationofrecoveryandresolutionmeasureshencereducingthelikelihoodofpublicbail-outs,whichwouldinturnhavedramaticimplicationsfore.g.fundingcosts. • DifferencesbetweentheproposalsofIndependentCommissiononBankingandHighlevelExpertGroup • “The differenceinthelocationofthering-fenceisimportant,...” InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |33 • JohnVickershasmadeveryinsightfulcommentsonthecompatibilityoftheproposalofhisgroup,theIndependentCommissionofBankingwiththeproposaloftheHigh-levelExpertGroup. • Ihaveafewcommentsonthis theme: • ICBandHLEGproposalsstartedfromdifferentdirections;theapproachtakenbyICBstartedfromthenarrow bankingphilosophy,whereasHLEGfocusedonthemostvolatilepartsofbankingbusiness. • However,thegroupsendedupwithqualitativelysimilarproposals. • AsJohnVickershasstatedalready,themainquestionasregardsthepositionofthering-fenceis“Whereshouldsecuritiesunderwritingbe;intheinvestmentbank(suchasin ICB)or in thedepositbank(asinHLEG)?” • AnotherdifferenceisthatICB’sproposalincludesgeographicalrestrictionsasnon-EEAcustomerscannotbeservedbythedepositbank. • ThishighlightsthefocusontheviabilityoftheUKbankingsectorintheICB. • HLEGisbasedontheviewthatunderwritingiscloselyconnectedwithcorporatebankingandthusnaturallybelongs tothedepositbank. • Fromthecorporateclient’sperspective,issuingabondisanalternativewayoffinancingto takingabankloan. • Fromthebank’sperspective,therearesimilarelements inboth,becausebothinvolveacustomercreditqualityassessment,althoughinunderwritingthebank’sownpositiontakingisnormallyquitelimited. • Itistruethatapromiseofmarketmakingcanbeanimportantcomplementtoasuccessfulunderwritingofabond. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |34 • However,separateentitieswithinthebankgroupcanwellprovidetheunderwritingandmarketmakingserviceswithoutanyadditionalcost tothecustomer. • HLEGdidemphasisetheimportancethatauthoritiesrequireadditionalseparationifthatisneeded tomaketherecoveryandresolutionplanscredible,ameasurethatwouldbringtheHLEGseparationproposalclosertotheICBring-fencingproposal. • Theproposalsarealsosomewhatdifferentwithrespect to theheightofthering-fence. • TheICB includedrestrictionsoncross-ownership,forexample. • AssuggestedbytheParliamentaryCommissionofBanking,taskedwiththepre-legislativereviewofthebill,the ring-fencewillnowbe“electrified”bygivingauthoritiesreservepowers to requirefullseparation. • “...butthe difference incapitalrequirementsimposedonretailbankingmayhavegreaterimplicationsforbanks.” • However,in myview thefundamentaldifferencebetweenthetwoproposalsisthedifferencein capitalrequirements. • ICBimposesanextracapitalrequirementonthering-fencedretailbank(~depositbank). • TheHLEGwasmoreconcernedofstrengtheningthecapitalisationofthetradingentityandthereforesuggestedareviewofcapitalrequirementsontradingbookrequirements. • Italsosuggestedareviewoncapitalrequirementsonrealestaterelatedlending. • HLEGdid, however, notmakeanyexplicitrequirementonimposinghighercapitalrequirements. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |35 – Idorecognisethattherequirement to issuedesignatedbail-in instrumentscanbeinterpretedashighercapitalrequirements. Thesewould,however,applyacrossbusinesslinesnotonlytothedepositbank. Somebanks mightbeable to implementseparationwithoutsignificantcostsasmanybanksalreadyhavetheneededgovernancesysteminplace,whereassuggestedchanges tothefundingstructure(toughercapitalrequirements)couldentailadditionalcosts. Itend to agreewiththecritiquesthatitcanbechallengingforthering-fencedbanks toremainviableastherelativelynarrowlydefined operationsmightnotbesufficient to generatetheprofitsneededtobuild uptherequiredlevelofcapital. Ontheotherhand,theHLEGproposalwouldnotseparatemore activitiesthanmandated,andthismightbethevoluntaryoutcomeinsomebanks. Itwouldalsobeveryimportant toensurethatcapitalrequirementsarealignedgloballytoensurethelevelplayingfield ofbanks. NowICBproposalwillsettheUKbanksandforeignsubsidiariesinadisadvantagedpositionincomparisontoforeignbanks’non-subsidiaryoperationsintheUKandwithnon-UKbankswhich canprovideUKcustomerswithfinancingelsewhere. Finally,Iwouldliketohighlighttheimportanceofsufficientlossabsorption capacityacrossbusinessareas. AshighlightedinrecentworkbyAnatAdmatiandMartinHellwig,imposinghighercapitalrequirementshasapositiveimpactonbankincentivesandbehaviour. Amongotherthings,well-capitalisedbanks maintaintheirlendingalsoduringdownturns. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |36 • Proprietarytradingandmarketmaking–isthequestionwhethertheyareseparableorwhethertheyshouldbeseparated? • ThefirstargumentfortheapproachtakenbyHLEGisbasedonthedesiredscopeofthesafetynet. • – Itisimportanttonotethatintheproposedseparation,thequestionisnotwhethercertaintypeofmarketmakingsupportstherealeconomyornot;asastartingpoint,allbankingactivitiessupporttherealeconomy. • Instead,thequestioniswhetherthereisamarketfailureofsomedegreeincertainbankingactivitiessothatthoseactivitiesneed tobepubliclysupportedbygivingthemaccesstoinsureddepositsasafundingbase. • I.e.,isitsothatmarketmakingcannotbecarriedoutinaprofitablemannerwithoutcheapfundingfromdeposittaking? • Ifthatisthecase,thenitmeansthatmarketmakingiscross-subsidized. • TodrawonarecentcommentbyDarrellDuffie“themorelimitedthetypesofrisksthatarelegallypermittedbythosewithinthesafetynet,thelessopportunityformoralhazard”Iwouldlike to highlighttheimportanceofensuringthatassmallafractionofbankingactivityaspossible,preferablyonlythe activitiesessentialtothefunctioningofthe society,i.e.thedeposittaking,paymentsystem,andperhapslendingtohouseholdsandSMEs,ought tobenefitfromagovernmentsafetynet. • Whendecidingwhatactivitiesareallowedtobefundedwithinsureddeposits,theremayofcoursebeaquestionoflevelplayingfieldbetweendifferentjurisdictions. • Butthatshouldbeaddressedviasufficientharmonisationofthestructuralmeasurestaken,notbybeingtoolaxaboutextendingtheuseof deposits. • In short,thereappears tobenoclearcasethatmarketmaking,excludingfewexceptions,oughttobenefitfromexplicitorimplicitgovernmentguarantees. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |37 • So,marketmakingshouldnothave accessto insureddeposits. • ThesecondargumentunderlyingtheHLEGproposalrelates towhetheritispossibletomakethedistinctionbetweenproprietarytradingandmarketmaking. • – Fromaregulatoryandsupervisoryperspectiveitisverychallengingtodrawaclearlinebetweenproprietarytradingandmarketmaking. • E.g.intheUStheimplementationoftheVolckerrulehasbeendelayedasaresultandwhenimplementedthesupervisorswillhave torelyontedioustransaction-by-transactionsupervision. • In itspureform,marketmakingisnotabouttakingopenpositionsandthepricespreadsgivenreverynarrow. • Onlywhenthingsdonotgoasplannedinventoryisbuildingupandthisiswhen wegetclosertothe territoryofproprietarytrading. • Atthelevelofthetradingfloor,itisrelativelyeasytodistinguishtheproprietarytradingandmarketmaking. • However,thingscanalsobehiddenifsodesired,hencemakingthesupervisionpotentiallyverydifficult. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |38 Reflectionsonreputationand itsconsequences Speechby MsSarahBloomRaskin,MemberoftheBoardofGovernorsoftheFederalReserveSystem,atthe2013BankingOutlookConference,FederalReserveBankofAtlanta,Atlanta,Georgia Goodafternoon.IwanttothanktheFederalReserveBankofAtlantaforinvitingmetojoinyoufortoday’s2013bankingoutlook discussion. Thereareanumberofinterestingandveryrelevant topicsonyouragenda,mostofwhicharerightlyfocusedonthefinancialandregulatoryenvironment. Iwouldlike tosharesomethoughtsthisafternoononabroadertopic,however,thatmaybedueforarefreshedlook:therelevanceofabank’sreputation. Let’sstartinanelementaryway inconstructingaconceptofreputation:Weknowthatreputationisnotentirelyamoraltrait. Weunderstandthatthereisadistinctionbetweencharacterandreputation. Whenwesaythatsomeoneshowsgoodcharacter,weareusuallyreferringtosomethingatthecoreoftheirbeingorpersonality. Ontheotherhand,whenwerefertoaperson’sreputation,werecognizethatreputationisourperceptionoftheperson,thatitisexternallyderivedandnotnecessarilyintrinsic to thatindividual. In otherwords,weunderstandthatapersonmaynothavecompletecontrolovertheperceptionthathasbeencreated. Reputation,throughnofaultofone’s own,canbetarnished. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |39 In thesameway,one’sreputationcanbegolden,eventhoughnothingwasdonetoearnit. Butlike thenotionofcharacter,reputation canbeearnedandit canbeatypeofstoredvalueforwhenchallengestoone’sownreputationcomelater. Nowlet’sbringthisdistinctionintothecontextofbanks: Manybankershaveasterlingcharacter,andtheyoperatefinancialinstitutionswithsterlingreputationsthatreflectthatbasiccharacter. Atthesametime,therearebankerswho,regardlessoftheirpersonalcharacter,managefinancialinstitutionswithreputationsthathavebeentarnished. Theirbanks’reputationscouldhavebeentarnishedbyalmostanything,butlikelymosttarnishisattributable to thesubprimemortgagemeltdownandtheensuingfinancialcrisisthatcosttheeconomytrillionsofdollars;leftmillionsofAmericansbankrupted,jobless,nderemployed,orhomeless;triggeredmassivelitigation;andshooktheconfidenceofournationtothecore. Manyofthedarkestmanifestationsofthefinancialcrisishavefinallybegun todiminish:theboarded-uphomeswithovergrownlawns,thehalf-builtskyscrapers,the“WeBuyHousesCheap”signsplantedatexitramps,theevictionnoticesnailed to frontdoors. Butevenastheeconomycomesbacktolife, ourmemoryoftheseeventsisstillsharpandthereputationaldamagesufferedbyU.S.financialinstitutionsduringthecrisisendures. Tobeblunt,alotofpeoplehavenegativefeelingsaboutbanks,whichtheydistrustandblameforthehugeinfusionsoftaxpayermoneyintothefinancialsystemthatweredeemednecessaryduringthecrisis. Thesereputationalconsequences– whetherjustifiedornot–aretobeexpected. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |40 Sociologistsandeconomistshavelongremarkeduponthecentralrolethatsocialtrustplaysinhealthymarkets. Markettransactionsdependonawholeseriesofassumptionsthatpeoplemustbeabletorelyon,includingthesoundnessofmoney,theenforceabilityofcontracts,thegoodwilloftheirpartners,theintegrityofthelegalsystem,andthecommonmeaningsoflanguage. Socialtrustisthegluethatholdsmarketsandsocietiestogether. Inthecontextofbanking,socialtrustandreputationarerelatedconcepts. Banksthemselves–incrisisornot– areparticularlyvulnerable toreputationalconsequencesbecauseoftheirpublicrole. Theprincipalsocialvalueoffinancialinstitutionsistheirabilitytofacilitatetheefficientdeploymentoffundsheldbyinvestors(andentitiesthatpoolthesefunds)toproductiveuses. Thisvalueismaximizedwhenthecosttotheentityputtingcapitaltoworkisclosetothepricedemandedbytheentitythatseeksareturnonitsinvestment. In traditionalbanking,thismeansthatfinancialintermediationoccursmosteffectivelywhentheinterestratechargedforuseoffundsinlendingisclosetotheinterestratepaidfordeposits. Asthedifferencebetweenthetwogrows(whichwouldbeattributabletoamountsextractedbyintermediariesascompensationforessentialintermediation),thecostsofborrowingforthepurposesofcreatingproductiveprojectsbecomehigherthantheyshouldbe,witharguablynegativereputationalconsequences. Giventheseparticularreputationaldimensionsassociatedwithfinancialinstitutions,mightfinancialregulatorshaveaninterestinconsideringreputationalharmsanalytically? InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |41 Couldtherebebenefitstounderstandingthewaysthatanindividualfinancialinstitution’sreputation– orthatofthefinancialindustryasawhole– mighthaveparticulareffectson,forexample,safetyandsoundness,financialinclusion,orfinancialinnovation? In myremarkstoday,Iwanttoconsidervariousaspectsofhowreputationalharmmanifestsitselfinbanksandbeginadialoguewithyouabouthow wemightrefreshourthinkingaboutthiscategoryofrisk. Iwillstartwithadescriptionofsomefactorsthat canaffectabank’sreputation,especiallyin thewakeofthefinancialcrisis. Next,Iwilltalkaboutwaysinwhichreputationmatters,includinghowsupervisorscanusetheiruniqueabilitytoseeinsidetheinstitutionsthattheyexaminetouncoversomeearlyindicatorsofreputationalproblems. Iwillthenturn to otherreasonswhypolicymakersmaywanttothinkaboutreputation. Onereasoninvolvespossibleconsequencesregardingfinancialinclusion;thatis,acustomer’sabilitytohavearelationshipwithhisorherbankthatputsthemintheposition to save,accesscreditinasustainableway,and understandthenatureofthefinancialtransactionsinwhichthey participate. Reputationalsomayhelp orhinderabank’sability to innovate,soIwillintroducethis topicnext. Finally,Iwanttoframeadiscussionaroundtherecentcybersecuritythreatsthatbanksarefacingandplacetheminthecontextofreputationalrisksothattheytoo canbediscussedconstructively. Ofcourse,IprefacetheseremarkswiththeadmonitionthattheseviewsaremyownandmaynotberepresentativeofthoseoftheFederalReserveBoard. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |42 Thefinancialcrisisandthereputationoffinancialinstitutions IthasbeenmorethanfiveyearssincethiscountrybeganexperiencingafinancialcrisisthatreverberatedwellbeyondWallStreet. Thiscrisiswasunique,andmanyofitsmarksonindividualsandcommunitiesremain. Itwasacrisisinwhichsignificantnumbersofbothsubprimeandprimemortgagedefaultsquicklyspreadacrosswholecitiesandregionsuntiltheimpactwasfeltthroughoutthecountry. Thedevastationwasmagnifiedbywavesofforeclosures,significantdropsinhousevalues,joblosses,and,ultimately,significantreductionsinhouseholdwealth,whichhavebeenresponsible,inpart,fortheslowrecoveryweconfront today. Thecausesofthecrisisandthesubsequentdevastationaremyriad,buttolargeswathsoftheAmericanpublicwhohaveexperiencedthedevastation,the causesrestsquarelyontheshouldersoffinancialinstitutions,especiallythelargestinstitutions. Further,manyAmericansdirecttheirangeratnotonlybanks,butpolicymakersaswell. Becausetheeconomypulledbackfromthebrinkofdepressiononlythroughamassiveandunprecedentedinfusionofpublicdollars,Americantaxpayersfeelthattheywereforcedintoapositionofacceptingthatthegovernmenthadtoputalotonthelinetosavethefinancialsystemfromruin. Andmanyofthosetaxpayersarestillunhappyaboutsuchamassivegovernmentinterventionthatseemedtoaidbanksthatwerenotheldtoaccount,whiledistressedhouseholdswereleft topaytheprice. Unfortunately,inthepublic’sview,littlehas happenedtorestoretheir trustandconfidenceinfinancialinstitutions. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |43 • Sincethecrisis,thepublic’sviewsofbanks havebeeninformed– for betterorworse–bytheirexperiencesandthoseoftheirfamiliesand neighbors,whomayhavelosttheirhomes,theirjobs,ortheirhouseholdwealth. • Manyattemptedunsuccessfullytomodifytheirunderwatermortgages,evenwhentheywerecurrentontheirpayments. • Againstthisbackdrop,thepublic’slackoftrustandconfidence hasbeenmagnifiedby,amongotherthings,theOccupyWallStreetmovement,paydayloans,overdraftfees,rateriggingsettlementsinLondonInterbankOfferedRate(LIBOR)cases,executivecompensationandbonusesthatseemtobearnorelationshiptoperformanceorrisk,failuresintheforeclosureprocess,andadrumbeatofcivillitigation. • In theInternetage,theimpactofconsumerdistrustisamplified:anyonecan easily,cheaply,andanonymouslycreate,organize,andparticipateinaprotest. • Participantsdonothave togatherphysically to maketheiractionfelt.Arecentsurveyfoundthat • 60percentofAmericanadultsusesocialmedia,suchas FacebookorTwitter,and • 66percentofthosesocialmediausers(39percentofallAmericanadults)haveusedsocialmedia toengageoncivicandpoliticalissues,includingbyencouragingotherpeopletotakeactiononapoliticalorsocialissue. • Take,forexample,theimpactoftheconsumerbacklashthateruptedinlate2011whenoneofthenation’slargestbanksattemptedtochargea$5monthlyfeeforitsdebitcard. • ACaliforniawoman,frustratedwiththebank’sdecisiontoimposethefee,createdaFacebookevent,dubbed“BankTransferDay,”andinvited herfriendstojoinher intransferringtheirmoneyfromlargebanks tocreditunionsonthatday. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |44 In thefiveweeksleadinguptoBankTransferDay,thisFacebookeventreceivedextensivepresscoverageandresultedinbillionsofdollarsindepositsreportedlyshiftingoutoflargebanks. ThebanktargetedbytheFacebookprotestultimatelyreverseditselfand declined to assessthemonthlyfee. Howreputationalriskmayberelevant Financialinstitutionsofallsizeshavesharedinthefall-out–fairlyorunfairly– fromageneraldeclineintheirindustry’sreputationamongthepublic. Moreover,thesteadystreamoflitigationagainstfinancialinstitutionssincethecrisishasfurtherharmedthereputationsofspecificfirmsamongtheircustomers. Considerthat intoday’sfinancialinstitutionsector,asubstantialportionofabank’senterprisevaluecomesfromintangibleassetssuchasbrandrecognitionandcustomerloyaltythatmaynotappearonthebalancesheetbutareneverthelesscriticaltothebank’ssuccess. Alsoconsiderthatattheendof2012,depositsatcommercialbanksreachedarecord$10trillion. Atthesametime,theshareofeachdepositdollarthatbankslentouthitapost-financialcrisislow inthethirdquarter,whichmeansthatbanks’netinterestmarginshavefallensharply. Across theindustry,loan-to-depositratiosaregoingdown. In 2007,banks’aggregateloan-to-depositratiowas91percent.Thisratiocurrentlystandsat70percent. In suchacontext,achievinghigherearningsisachallenge. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |45 Ifbankprofitabilityisgoingtoimproveinacontextoflow interestratesandhighercompliancecosts,lendingincomemayremainlow. Profitswillneedtocomefromelsewhere. Onesourceofprofitswouldbeproductsthatarenotinterest-ratedependent,butfee-dependent. In otherwords,compressednetinterestmarginsmeanthatmanybanksmaylooktonewfee-generatingproductsandtradingactivitytoenhanceprofits. Thepressure to generateenhancedprofitsthroughhighfeesispalpable,andbanksmaychoosetomoveaggressivelydownthesepaths. Butwhenabankalreadysuffersfromapoorreputation– eitherdeservedlyorasaknock-oneffectofbroaderdiscontentwiththefinancialindustry–itlikelywillfacedifficultiesinintroducingnewfee-generatingproductsoractivitieswithoutinvitingfurthercriticismanddamagetoitsreputation. Soanevaluationoftheeffectsofthenewproductoractivityonthebank’sreputationpriortolaunchisarguablynecessary. Reputationalriskandsupervision Theeffectsofthefinancialcrisis,combinedwiththepoweroftheInternettobroadlyandquicklypublicizeinformation–whetherfactuallyaccurateornot– shouldalertbanks tohowtheyaremanagingtheirreputations. Andsupervisorshaveadutytoseethatallrisksarefullyunderstood,eventhoserisksthat,likereputationalrisk,areunquantifiableorhavenotfullyemerged. Ibelieve thisisanarea wheresupervision canaddvalue. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |46 Totheextentpossible,supervisioncanunveilhiddenlossexposuresthatmaybebuildingupthroughtheaccumulationofreputationalriskelements. Ifwewerebetterable to identifyandmonitorsuchfree-floatingrisk,andinsodoing,topushbankboardsofdirectorsandseniormanagementtopaymoreattentiontoreputationalrisk,wecouldhelpreducetheunderpricingoftheserisks. Manyhaveargued,andIthinkit’sacompellingargument,thatineffectivesupervisionandenforcementofexistinglawsandregulationscontributedtothefinancialcrisis. Bytoleratingreducedtransparencyofrisk inbalancesheetsandincomplexinstitutionalportfolios,aswellasarbitragearoundcapitalrequirementsandotherprudentialmeasures,supervisionmayhaveencouragedtheunderpricingofrisk. Andthesuddencorrectionofthisunderpricingofrisk,inturn,acceleratedthecrisis. Thecrisispunishedinvestorswhoacceptedmoreriskthantheythought theyhadtakenon,itpunishedconsumerswhooverleveragedthemselves,itpunishedAmericanswholosttheirjobsandhomes,anditcontributedtothedeclineofonce-vibrantneighborhoodsandtowns. Tomitigatethechancesofsuchacrisisoccurringagain,supervisorsneedtoredoubletheireffortstowardpromotinggreatertransparencyofrisksandearlyconfrontationofpotentiallossexposures. Weshouldviewtheseeffortsasasetofresponsibilitiesforbothbanksandregulatorsthatarealignedtoassurethepublicandmarketsthatriskscan befullyunderstoodandaccuratelyestimatedandpriced. In someways,thisperspectiveisnotnew territoryforbankregulators. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |47 TheFederalReserve,forexample,issuedsupervisoryguidancein 1995 thatidentifiedthesixprimaryrisksthatremainthefocusofitssupervisoryprogram,andreputationalriskis amongthem. Havingsaidthat,itisstillariskthatbothbanks andsupervisorsshouldlearnhow to identifyexanteratherthanexpost. So,whilereputationalriskisnotanewconceptbyanymeans,itisanareathatisripeforadditionalwork. Forexample,theenterpriseriskmanagementframeworkoftheCommitteeofSponsoringOrganizationsoftheTreadwayCommission–theso-called“COSOstandard”–doesnotaddressreputationalrisk. Likewise,theBaselcapitalframeworksexcludereputationalrisksfromregulatorycapitalrequirements. Accordingly,thecurrentapproachtomanagingreputationalriskislargelyreactiveratherthanproactive. Banksandexaminers tendtofocustheirenergiesonhandlingthethreatstotheirreputationsthathavealreadysurfaced. Thisisnotrisk management;itiscrisismanagement– areactiveapproachaimedatlimitingthedamage. Instead,weshouldthinkaboutasupervisoryapproachthatincentivizesbankmanagers to sufficientlycontemplate,quantifyifnecessary,andcontrolthefactorsthataffectthelevelofsuchrisksbeforetheyfullyemergeinanunmitigatedform. ThewaythattheFederalReservesupervisesbankingorganizationsmayhelpidentifyriskssooner. Forallbankingorganizations,thesupervisoryprogramheredoesnotsimplyrelyonanannualonsiteexamination. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |48 TheFederalReservesupplementsitsregularexaminationactivitieswithaprogramofcontinuousmonitoringbetweenexaminations. Oneofthekeyobjectivesofthisprogramistoidentifyemergingrisksandcommunicatewithotherregulatorsandthebanks anupdatedriskassessmentandsupervisorystrategybasedontheserisks. Whenwecontemplateasupervisoryapproachthatilluminatesreputationalrisk,wemightbeable to morefullyuncovertheinterconnectionofrisksthatcertain activitiescouldimposeoninvestors, creditors,counterparties,andtaxpayers. Inthisapproach,wewouldfirstandforemostneedtoencouragebankstoassessthepotentialriskinessofparticularoperations,investments,products,anddecisionstotheirreputationsand,ultimately,totheirenterprisevalue. Assupervisors,oneobjectiveasweworkwithfinancialinstitutionstoextractsuchinformationwouldbetotrytodevelopwaysofmeasuringthevalueoftherisks thatbanksshiftontothefinancialsafetynet. Reputationandfinancialinclusion Thereisalsoarelationshipbetweenreputationandfinancialinclusion,bywhichImeantheextenttowhichconsumerscanparticipateinafinancialmarketplacethatconsistsofcompetitiveprovidersofcredit,savingsvehicles,andsourcesofenablingfinancialinformation. Aspolicymakers,wemustaddresstheperceivedtrustworthinessofthosefinancialinstitutionsthatinteractwiththepublic andmovethemillionsofAmericanslingeringinthemarginsofthefinancialmarketplaceintorelationshipsthatprovidethemwithsustainableaccesstobankingandcredit,anunderstandingofhow mortgagesandcreditwork,andan understandingofhow to createsavings. DatafromtheFederalReserve’sSurveyofConsumerFinancesandtheFederalDepositInsuranceCorporation’ssurveyoftheunbankedand underbankedshowthatthepercentageoffamiliesearning$15,000per InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |49 yearorlesswhoreportedthattheyhavenobankaccounthasbeenincreasingsteadilyforthepastfiveyears,resulting in morethan28percentofthesefamiliesbeingunbankedasof2011. Familiesslightlyfurtheruptheincomedistributionscale,earningbetween$15,000and$30,000peryear,arealsofinanciallymarginalized:12percentreportedbeingunbankedandalmost26percentreportedbeingunderbankedin2011. Thereareseveralpotentialreasonsfortheseimpedimentstoinclusion. Whenweexaminebarriersthatindividualconsumersfaceinbecomingfinanciallyincluded,weuncovertrustworthinessandreputation. AFederalReserveanalysisofthemostrecentSurveyofConsumerFinancessuggeststhattheprimaryreasonindividualsdonothaveatransactionaccountisasimpledislikeofdealingwithfinancialinstitutions. Ifthatdislikeemanatesfromthereputationoftheparticularbank,orthereputationofthebankingindustryasawhole,policymakersandfinancialinstitutionswillnotbeabletoenhancefinancialinclusionwithoutaddressingthereputationalcontext. Reputationandinnovation I’dlike to imaginehow thepublic’ssenseofwell-beingmightbeenhancedbytheirinteractionswithfinancialinstitutions. Ifwepaidattentiontotheexperiencesofconsumersastheyinteractwithvarioussegmentsofthefinancialmarketplace,whatcouldwelearn? Ifweseerigiditiesorimperfectionsinthatinteractiveexperience,whatinnovationmightweimaginethatwouldnotonlyreducereputationalriskbutcreatesomething newandpotentiallyadvantageous? Technological innovationwasthesubjectofarecentawardceremonyin SanFrancisco. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |50 Thewinnerswerecompanieswithnameslike SoundCloud,GitHub,MakerBot,Techmeme,andSnapchat,allofwhichpresumablydoamazingthings,althoughIdon’tunderstandexactlywhat. But,evidently,therealbuzzattheceremonywasoversomethingmuchmoremundanethatIforonehavenoproblemunderstanding. Thatbuzzwasaroundapedestrianitem–anewandimprovedcoffeecuplid. Thislid,calledFoamAroma,reportedlyprovidesexactlytherightsetofopenings to maximizearomaandrecyclability,whileminimizingtheeffectsofcoffeespurtingouttoofast. Thepointhereisthattheinnovatornoticedsomethingsimplethatothershadnot:manycoffeeshopemployeesdon’tdrinktheircoffeefromcupswithplasticlidsliketheircustomersdo,sotherewasamarketneedthathadnotbeenrecognizedandthenaddressed. HereIamnotjusttalkingaboutthemixedmiracleofmobilebankingandmobilepaymentsorbeingabletotake apictureofacheck withasmartphoneanditappearinginmycheckingaccount. That’satopicthatisamazingin its ownrightandworthyofaseparatespeech. Iamtalkingaboutencouragingbanks topayattentiontothebankingexperiencesoftheircustomersandfindingprocessimprovementsorserviceelementsthatmaylead tosomethingseeminglymundanebutvaluablenonetheless. Someinnovatorsseereputationitselfasnotjustsomethingtobemanaged,butasaproductinandofitself. WithbuyersandsellersrepeatedlyandconstantlyinteractingontheInternet,thereare“reputationtrails”thatarebeingcreatedthat,whencompiled,giveanalternativesetofmarkers abouthowtrustworthya particularbuyerorsellermaybe. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com