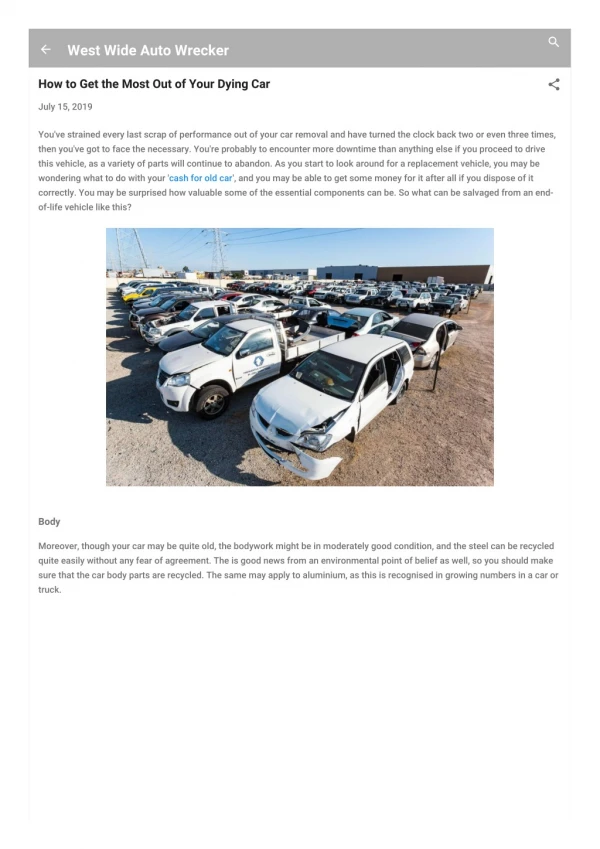

Download

1 / 13

130 likes | 142 Views

Get the most out of life with John Hancock Life Insurance Company's long-term care rider. Protect your loved ones, assets, and health with this comprehensive coverage. Explore the benefits today.

E N D

LIFE INSURANCE WITH THE LONG-TERM CARE RIDER Get the most out of LIFE John Hancock Life Insurance Company (U.S.A.) ICC17 LIFE-2537 9/17 MLI081517063

Investing involves risk including possible loss of principal. Information is current as of the date of this material. Any opinions expressed herein are from a third party and are given in good faith, are subject to change without notice, and are considered correct as of the stated date of their issue. Merrill Lynch, Pierce, Fenner & Smith Incorporated is not a tax or legal advisor. Clients should consult a personal tax or legal advisor prior to making any tax or legal related investment decisions. Bank of America Corporation (“Bank of America”) is a financial holding company that, through its subsidiaries and affiliated companies, provides banking and investment products and other financial services . Merrill Lynch makes available products and services offered by Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”), a registered broker-dealer and Member SIPC, and other subsidiaries of Bank of America Corporation. Merrill Lynch Life Agency is a licensed insurance agency and a wholly owned subsidiary of Bank of America Corporation. Merrill Lynch offers a broad range of brokerage, investment advisory and other services. There are important differences between brokerage and investment advisory services, including the type of advice and assistance provided, the fees charged, and the rights and obligations of the parties. It is important to understand the differences, particularly when determining which service or services to select. The views and opinions expressed in this presentation are not necessarily those of Bank of America Corporation; Merrill Lynch, Pierce, Fenner & Smith Incorporated; or any affiliates. Merrill Lynch has not participated in preparing this presentation and accepts no responsibility for the accuracy of the information contained herein. For more information about these services and their differences, speak with your Financial Advisor. Nothing discussed or suggested in these materials should be construed as permission to supersede or circumvent any Bank of America, Merrill Lynch, Pierce, Fenner & Smith Incorporated policies, procedures, rules, and guidelines. Investment products offered through MLPF&S and insurance and annuity products offered through Merrill Lynch Life Agency Inc.: ML 19-000949 Expires 12/1/2019 Slide 2 of 13

What keeps you up at night? Protecting your loved ones Protecting your assets Protecting your health Slide 3 of 13

What could be the greatest threats to your financial security? • Caring for a sick parent or loved one • Becoming ill or getting injured • Dying too soon or living too long 70% of people aged 65 and over will need some level of long-term care at some point in their lives1 1. U.S. Department of Health and Human Services, National Clearinghouse for Long-Term Care Information, February 2017. https://longtermcare.acl.gov/the-basics/who-needs-care.html Slide 4 of 13

Who pays for long-term care? Medicare • Only pays for a medically necessary skilled nursing facility or home health care services • Maximum benefit: 100 days Medicaid • Pays for certain health services and nursing home care for people with low income and limited assets • Assets must be spent down to qualify You • How much of your income can be used? • Which of your expense are discretionary? • Which assets would you deplete first to cover this cost? ? DID YOU KNOW: The national average cost of a nursing home is $102,900 A YEAR2 2. John Hancock Cost of Care Survey, conducted by LifePlans, Inc., 2016. Slide 5 of 13

What impact would this have if you covered the cost? • Will you have enough saved to pay your daily expenses and care at the same time? • Which of your assets could be liquidated to make up any shortfall? • Would your children or a loved one have to help care for you? ? DID YOU KNOW: The average stay in a nursing home is 2-3 YEARS.3 3. Life Happens, Startling Facts About Long-Term Care. Bill O’Quin. March 11, 2015. http://www.lifehappens.org/blog/startling-facts-about-long-term-care/ Slide 6 of 13

Combination life insurance and long-term care coverage • If you never need long-term care, your entire death benefit will be paid to your beneficiaries on a tax-favored basis. • If you need long-term care, your death benefit can be accelerated to help pay long-term care expenses • And any residual death benefit remaining in your policy will be paid to your beneficiaries on an income tax-favored basis Slide 7 of 13

Hypothetical Case study: Susan Harris Background • Age 55 • Married for 25 years • Two college-aged children • Mother in a nursing home for 2+ years Assets • Substantial 401(k) balance • Other investments Susan wants to protect her assets and her independence from a potential long-term care event. 67% OF NURSING HOME RESIDENTS are WOMEN.4 Example is hypothetical and shown for illustrative purposes only. 4. AARP Fact Sheet. Women and Long-Term Services and Supports. Ari Houser. April 2017. http://www.aarp.org/ppi/info-2017/women-and-long-term-services-and-supports.html Slide 7 of 12 Slide 8 of 13

Hypothetical Case study: Susan Harris By purchasing a permanent life insurance policy with a LTC Rider, Susan has access to: If the actual monthly long-term care expenses are less than the maximum monthly benefit amount, coverage will last even longer! Tax Free Death Benefit if she never needs long-term care Long-Term Care Benefit Pool if she needs long-term care Slide 9 of 13

Accessing your Long-Term Care rider benefits Eligibility • Unable to perform two of six activities of daily living: bathing, dressing, eating, continence, transferring and toileting. • Demonstration of severe cognitive impairment that requires professional care, e.g., Alzheimer’s disease, dementia Elimination Period • 100-day waiting period before benefits begins • Needs to be satisfied only once Choice of Setting • Skilled, intermediate or custodial care • At home, in a residential care facility, nursing facility, or adult day care center Slide 10 of 13

Life insurance with John Hancock’s Long-Term Care rider is one of the most affordable ways to protect your assets and your independence. Slide 11 of 13

QUESTIONS? Slide 12 of 13

Important Disclosures The purpose of this communication is the solicitation of insurance. Contact will be made by an insurance agent or insurance company. All guarantees and benefits of the life insurance policy are backed by the claims-paying ability of the issuing insurance company. Policy guarantees and benefits are not obligations of, nor backed by, the broker/dealer and/or insurance agency selling the policy, nor by any of their affiliates, and none of them makes any representations or guarantees regarding the claims-paying ability of the issuing insurance company. Life insurance death benefit proceeds are generally excludable from the beneficiary’s gross income for income tax purposes. There are few exceptions such as when a life insurance policy has been transferred for valuable consideration. Comments on taxation are based on John Hancock’s understanding of current tax law, which is subject to change. No legal, tax or accounting advice can be given by John Hancock, its agents, employees or registered representatives. Prospective purchasers should consult their professional tax advisor for details. The Long-Term Care (LTC) rider is an accelerated death benefit rider. The Maximum Monthly Benefit Amount is $50,000. When the death benefit is accelerated for long-term care expenses, the death benefit is reduced dollar for dollar, and the cash value is reduced proportionally. The policy account value is also reduced proportionally. There are additional costs associated with this rider. Rider is subject to underwriting and a medical exam may be required to determine eligibility. This rider has exclusions and limitations, reductions of benefits, and terms under which the rider may be continued in force or discontinued. Please contact the licensed insurance producer or John Hancock for more information, cost, and complete details on coverage. John Hancock’s Long-Term Care rider is not a Partnership Qualified product. For more information on Partnership Qualified products, please contact your state department of insurance. Insurance products issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA 02210.Rider Form Series: ICC13 14LTCR Slide 13 of 13