Download

1 / 44

440 likes | 581 Views

Chapter 24. Norton Media Library. Chapter 24. Taxes and Spending. Nariman Behravesh Edwin Mansfield. Government Spending as a Share of the Economy, 1930-2006. The following slide shows total government spending (federal, state, and local) as a share of the economy.

E N D

Chapter 24 Norton Media Library Chapter 24 Taxes and Spending Nariman Behravesh Edwin Mansfield

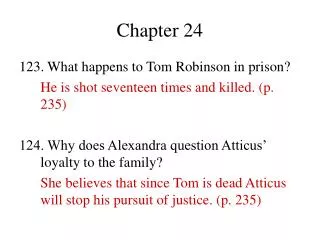

Government Spending as a Share of the Economy, 1930-2006 • The following slide shows total government spending (federal, state, and local) as a share of the economy. • Total government spending accounted for only 9.4% of GDP in 1930, and only one third of this spending was at the federal level. • Government spending, particularly at the federal level, soared from 1930 to 1970. • Total government spending rose from 9.4%of GDP in 1930 to 30.2% of GDP in 1970. • Since 1970, government spending has been relatively constant at about one-third of the U.S. economy.

3.0 6.5 9.4 8.4 7.3 15.7 14.7 6.3 21.1 24.1 16.5 7.6 30.2 19.4 10.9 32.8 21.0 11.8 34.2 21.6 12.6 31.9 19.0 12.9 33.8 20.3 13.5 The Size of Government Government Expenditures as a Share (%) of GDP Federal 1930 State & local 1940 1950 1960 1970 1980 1990 2000 2006

Social Security 20.7% Defense 19.7% NetInterest 8.5% Transportation2.6% Other13.3% Income Security 13.3% Medicare and health 21.9% Back to slide 29 How the Federal Government Spends (2006) Sources: Economic Report of the President, 2007, and Statistical Abstract of the United States, 2007.

Insurance trusts 8.9% Education28.8% Public welfare & Health 19.5% Administration & other 21.9% Police &Fire Protection 4.9% Transportation 5.5% Interest on debt 3.6% Utilities &liquor stores 6.9% How State and Local Governments Spend Sources: Economic Report of the President, 2007, and Statistical Abstract of the United States, 2007.

Financing the Public Sector: Taxation In order to make available public and correct inequity, government must free up resources from the production of private goods. • Taxes shift resources from private to public use • Taxing households and businesses reduces their incomes and spending, the private demand for products decreases, as does the private demand for resources. • This is known as Deadweight Loss

THE U.S. TAX STRUCTURE Collection of Taxes • Federal Government • Personal Income Tax • Corporate Income Tax

THE U.S. TAX STRUCTURE Collection of Taxes • State Governments • Personal Income Tax • Sales Tax • County and City Governments • Property Taxes

TAXES Tax Incidence The Tax Incidence or Tax Burden is the determination of who actually pays the tax. Government must determine how to appropriate taxes from the citizens.

THE U.S. TAX STRUCTURE INCIDENCE OF U.S. TAXES • Personal Income Tax • Individual • Corporate Income Tax • Stockholders – Consumers • Sales Taxes • Consumers • Property Taxes • Owner or Renter

TAXES • Tax Incidence • Benefits-Received Principle • Ability-to-Pay Principle

Benefits Received versus Ability to Pay • The benefits-received principle is the idea that people who receive the benefit from government-provided goods and services should pay the taxes required to finance them. • The ability-to-pay principle is the idea that people who have greater income should pay a greater proportion of it as taxes than those who have less income.

THE TAX BURDEN • Progressive Tax • Regressive Tax • Proportional Tax • Flat Tax

Progressive, Proportional, and Regressive Taxes • A progressive tax is one whose average tax rate increases as the taxpayer’s income increases. • A regressive tax is a tax whose average tax rate decreases as the taxpayer’s income increases. • A proportional tax is a tax whose average tax rate remains constant as the taxpayer’s income increases. • A flat tax is a tax which takes the same monetary amount regardless of income.

Progressive, Proportional, and Regressive Taxes • In general, progressive taxes fall relatively more heavily on high-income households while regressive taxes are those that fall relatively more heavily on the poor.

Progressive, Proportional, and Regressive Taxes • Taxes are classified as progressive, proportional, or regressive, depending on the relationship between • average tax rate (total tax paid as a percentage of income) and • marginal tax rate (the rate paid on each additional dollar of income).

TAX APPLICATIONS: Identify whether progressive, regressive, or proportional • Personal Income Tax • Progressive • Sales Tax • Regressive • Corporate Income Tax • Proportional • Payroll Taxes • Regressive • Property Taxes • Regressive

Tax Progressivity in the U.S. • The majority view of economists is as follows: • The Federal tax system is progressive. • The state and local tax structures are largely regressive. A general sales tax and property taxes are regressive with respect to income. • The overall U.S. tax system is slightly progressive.

THE TAX ISSUE The Liberal Position

THE TAX ISSUE The Conservative Position