Download

1 / 117

1.17k likes | 1.2k Views

Understand the importance of accounting, financial data vs. information, and the accounting process stages to assist small business owners in decision-making. Learn to collect, record, report, and provide advice based on financial information.

E N D

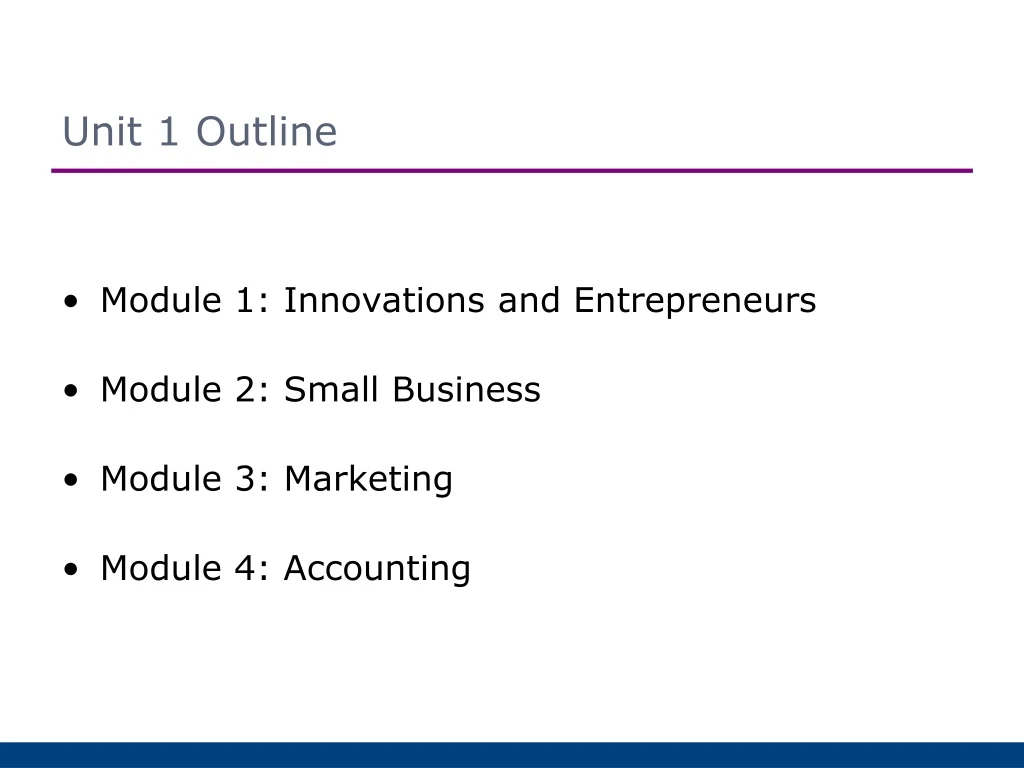

Unit 1 Outline • Module 1: Innovations and Entrepreneurs • Module 2: Small Business • Module 3: Marketing • Module 4: Accounting

Session 1: Role of accounting • Define accounting, financial data, financial information, source documents, recording, reporting, and advice. • Explain why accounting is important for businesses.

Why is accounting important? • Business is not just about making and selling; it is about managing – managing people, managing stock, managing customers and suppliers – and, last but not least, managing cash. • If a business owner is to manage their business effectively, then they will need accurate information that can be relied upon to assist them in the decisions they make. • The purpose of accounting then is to provide business owners with financial information that will assist them in making decisions about the activities of their firm.

What is accounting? Accounting is the collection, recording and reporting of financial information to assist business owners in decision-making

Financial data and financial information Accounting is about providing info; but that info has to come from a source and actually begins its life as raw facts (source documents) before being transformed into a form that is useful for decision-making (financial reports). Therefore we need to distinguish between financial data and financial information. Financial Data Financial Information financial data which has been sorted, classified and summarised into a more usable and understandable form • raw facts and figures upon which financial information is based

What are the 4 stages of the accounting process? The process of turning financial data into financial information is facilitated by what is known as the accounting process.

Accounting Process Stage 1: Collect source documents • Business collects the source documents relating to its transactions. • Source documents are the pieces of paper that provide both the evidence that a transaction has occurred, and the details of the transaction itself. Examples include: • Receipts, provide evidence of cash received by the business • Chequebutts, provide evidence of cash paid by the business • Invoices, provide evidence of credit transactions • Memos, provide evidence of transactions within the firm itself

Accounting Process Stage 2: Recording • Recording involves sorting, classifying and summarising the information contained in the source documents so that it is more usable. • Common accounting records include: • journals, which record daily transactions of a common type (such as all cash paid, all cash received, or all stock purchased on credit) • stock cards, which record all the movements of stock in and out of the business.

Accounting Process Stage 3: Reporting • Reporting involves the preparation of financial statements that communicate financial information to the owner, so that decisions can be made. • There are three general-purpose reports that all businesses should prepare: • a Statement of Receipts and Payments to report on the cash the firm has received and paid, and the change in its bank balance over a period • an Income Statement to report on the firm’s revenues and expenses over a period • a Balance Sheet to report on the firm’s assets and liabilities at a particular point in time.

Accounting Process Stage 4: Advice • Advice is the provision to the owner of a range of options appropriate to their aims/objectives, and recommendations as to their suitability. • This is where the real skill of an accountant comes into play! Without proper advice, the information in the reports is as good as useless, but if the reports are explained carefully and the accountant provides the owner with a range of options, a more informed decision – and a better outcome for the business – should occur.

Practice Exam Questions 1. Reorder the following stages of the accounting process: • recording transactions in journals and stock cards • collecting source documents like receipts and cheque butts • providing advice to the owner of the business • preparing financial reports. 2. Identify which stage of the accounting process is performed by each of the following actions: • preparing an Income Statement • filing sales invoices • entering transactions in a cash journal • presenting the owner with alternative sources of finance.

APs vs QCs APs QCs Qualitative characteristics are the qualities we would like our accounting reports to possess, and include. • Accounting principles are the generally accepted rules governing the way accounting information is recorded MCCHERG Red Rooster’s Ugly Chickens

Accounting Principles •Monetary Unit – all items must be recorded and reported in a common unit of measurement; that is, Australian dollars • Consistency – accounting methods should be applied in a consistent manner to ensure that reports are comparable between periods • Conservatism – losses should be recorded when probable but gains should only be recorded when certain. This is so liabilities and expenses are not understated and assets and revenues are not overstated.

Accounting Principles • Historical Cost – the recording of a transaction at its original cost or value, as this value is verifiable by reference to the source document •Entity – the business is assumed to be separate from the owner and other businesses, and its records should be kept on this basis • Reporting Period – the life of the business must be divided into periods of time to allow reports to be prepared • Going Concern – the life of the business is assumed to be continuous, and its records are kept on that basis.

Qualitative Characteristics • Relevance - Reports should include all information that is useful for decision-making. • Reliability - Reports should contain information verified by source document evidence so that it is free from bias. • Understandability - Reports should be presented in a manner that makes it easy for the user to comprehend their meaning. • Comparability - Reports should be able to be matched up to each other over time through the use of consistent accounting procedures.

Activity • Complete the AP and QC mix and match!

Session 2: Accounting equation • Describe the accounting equation. • Identify and define assets, liabilities and owners’ equity. • Explain the relationship between elements of the accounting equation. • Calculate owner’s equity using the accounting equation.

These are absolutely critical to understand. If you misclassify something, you will record it incorrectly, which will throw out your reports and render your results incorrect. Each element has particular ‘criteria’ to be met to be classified as a given element. Accounting Elements

5 Accounting Elements: Assets Liabilities Owner’s Equity Revenues Expenses For now, we will focus of A, L + OE Accounting Elements

Asset = a resource controlled by an entity, as a result of a past event, that is expected to provide a futureeconomic benefit to the entity. For an item to be recognised as an asset, it must meet all parts of the definition: Resources Control Future economic benefits 1. Assets

RESOURCE = items capable of generating economic gain for a business. What are some examples of resources? 1. Assets • Bank (cash held there, not the building) • Stock • Vehicles • Premises

CONTROL= firm must be in a position to determine how and when the item is used. This is NOT NECESSARILY the same as owning something. Control is broader (so it includes, but is not restricted to, what the firm owns) What is an example of something NOT under the firm’s control? 1. Assets

What is an example of something NOT under the firm’s control? 1. Assets • The business owner’s home cannot be classified as a business asset because it is not under business control. • This is where the ENTITY principle comes into play!

APs vs QCs APs QCs Qualitative characteristics are the qualities we would like our accounting reports to possess, and include. • Accounting principles are the generally accepted rules governing the way accounting information is recorded MCCHERG Red Rooster’s Ugly Chickens

APs Monetary unit Conservatism Consistency Historical cost Entity Reporting period Going concern The entity principle states that the BUSINESS is separatefrom its OWNER. Essentially, if you own a business, those records are kept separate to your own personal records.

FUTURE ECONOMIC BENEFIT = some sort of benefit that is yet to be received. Think-pair-share: Which principle does this relate to? 1. Assets Going Concern principle Example: • Cash in the bank = asset b/c it can be spent at some point in the future. • Cash paid for this month’s wages ≠ asset b/c there is no future benefit (the benefit has already been received).

Liability = Future sacrifice in economic benefits (outflow)that the organisation has the present obligation to make. For an item to be recognised as a liability, it must meet all parts of the definition: Future sacrifice in economic benefits Present obligations 2. Liabilities

Future sacrifice in economic benefits (outflow) FUTURE = the sacrifice has not yet occurred, but the liability is “expected to result in” this sacrifice. SACRIFICE / OUTFLOW = giving up something for the sake of something else. ECONOMIC BENEFITS = usually a future cash payment, but not necessarily (eg. unearned accounts) 2. Liabilities

So, what does a future sacrifice / outflow in economic benefits actually look like? Cash as the economic benefit Eg. cash, the expected outflow (sacrifice) occurs when Luke’s Tournament Masters pays its debts. Non-cash economic benefit Luke’s Tournament Masters has just received cash in advance for a job (a summer riding camp) which will not occur for another 2 weeks. It is not a cash payment that is required to extinguish this liability, it is the completion of work. 2. Liabilities

PRESENT OBLIGATION = a legal responsibility (obligation) to settle a debt. Debt = something (money, goods or services) owed to someone else. If Luke’s Tournament Masters has a legal obligation to settle a debt, it is very likely that this debt is a liability. 2. Liabilities Think about it … if a business has a present obligation to settle a debt then they will likely have to make a future sacrifice of economics benefits in order to settle this debt.

What does a present obligation look like? 2. Liabilities • Demi’s Beauty Studio has a mortgage on the premises of the recording studio. • The contract with the bank means that Demi’s Beauty Studio is obligated to repay the bank the amount owing on the premises.

2. Liabilities What is not a present obligation? • Demi’s business expects to pay for advertising in 2015. • This cannot be reported as a liability b/c right now there is no obligation to pay for the ads. • The obligation only occurs once the firm has signed a contract or the advertising itself has been provided.

Recall • Assets = resources controlled by an entity, from which future economic benefits will flow to the entity. • Liabilities =present obligations of the entity, the settlement of which is expected to result in an outflow of resources embodying economic benefits.

Activity • Research and provide a definition for each of the following items • Classify the items as an asset or a liability • Creditors • Equipment • Bank overdraft • Vehicle • Furniture • Stock of supplies • Mortgage • Cash at bank • Debtors • Loan • Premises

Activity: Answers ASSETS LIABILITES Mortgage Bank overdraft Creditors Loan • Stock of supplies • Cash at bank • Debtors • Premises • Equipment • Vehicle • Furniture

Owner’s Equity = the Residual Interest in the assets of the entity after deducting liabilities How else can we think of this concept? 3. Owner’s Equity 3 ways: • What’s left over for the owner once the firm has met all its obligations (liabilities). • The amount the business ‘owes the owner’ • Owner’s equity = Assets – Liabilities

So, owner’s equity is the amount the business ‘owes the owner’. How can a business owe its owner? Think-pair-share: What principle does this relate to? 3. Owner’s Equity • Recall the entity principle – the business and the owner are separate. So, the assets and liabilities of the firm are not the owner’s they are the firm’s. • BUTassets > liabilities (b/c of the accounting equation), so there must be something left over! This left over (i.e. residual) is what the firm owes to the owner.

The accounting equation • Both LIABILITIES and OE represent CLAIMS on the ASSETS of the business • Liabilities are what the business owes to external parties • OE is what the business ‘owes’ the owner • This relationship between assets, liabilities and owners equity is what is described as the ACCOUNTING EQUATION.

The Accounting Equation A beautiful (and easy) thing about Accounting is that the Accounting Equation must always balance.

The Accounting Equation Why does it have to balance? Consider this … We have $30,000 leftover. This means $30,000 has not been claimed by liabilities or the owner! It is not possible for an amount to remain unclaimed.

The Accounting Equation Who would be entitled to the unclaimed amount? The owner! So, owner’s equity would have to be $40,000 not $10,000.

Activity For each of the following examples, use the accounting equation to calculate the value of owner’s equity: Mark’s Dog Washing Service has $4500 in assets, but owes $500 to the local newspaper for advertising. Bianca owns and operates Bianca for Hair. The firm has $5 600 in assets, but owes a supplier $250.

Activity 1: Answers • Mark’s Dog Washing Service has $4500 in assets, but owes $500 to the local newspaper for advertising.

Activity 2: Answers • Bianca owns and operates Bianca for Hair. The firm has $5 600 in assets, but owes a supplier $250.

Activity For each of the following examples, use the accounting equation to calculate the value of owner’s equity: Andrew is the owner of an accounting firm. He owns a car worth $1 500, a stereo worth $800, clothing worth $750 and other assets worth $1 000. His firm owns office equipment worth $15 000 and a vehicle worth $20 000, but owes $600 to an employee. Sasha Enterprises has $4 500 in the bank, but owes $1 000 on a loan it took out to buy equipment. The equipment is worth $1 500, and a company car is worth $17 000. A client still owes $500 for work done by the firm, and Sasha owes $150 on her Visa card.

Activity 3: Answers • Andrew is the owner of an accounting firm. He owns a car worth $1 500, a stereo worth $800, clothing worth $750 and other assets worth $1 000. His firm owns office equipment worth $15 000 and a vehicle worth $20 000, but owes $600 to an employee.

Activity 4: Answers • Sasha Enterprises has $4 500 in the bank, but owes $1 000 on a loan it took out to buy equipment. The equipment is worth $1 500, and a company car is worth $17 000. A client still owes $500 for work done by the firm, and Sasha owes $150 on her Visa card.

Activity For each of the following examples, use the accounting equation to calculate the value of the assets. • John knows that his equity in his firm is $3000, and that his firm owes $600 to a supplier. • Ella has equity of $10 000 in her business, and has $5 000 worth of personal assets. She owes Branko $500, and the firm has debts of $3 000.

Activity 1: Answers • John knows that his equity in his firm is $3 000, and that his firm owes $600 to a supplier.