Download

1 / 19

190 likes | 205 Views

Learn about the home buying process, including advantages like building equity and disadvantages such as repair costs. Explore steps like financial discussions, sale agreements, earnest money, inspections, and closing costs. ####

E N D

The Home Buying Process • * The most common type of housing bought is the • ??? • Free standing single family home.

People choose to rent or buy a home for many different reasons… • Personal and financial goals; • Personal values, needs, and wants; • Amount of money available for housing costs; • Credit history • Location preference; • Expected length of stay in a particular place, etc.

Advantages of Buying a house… • Build equity which can be borrowed against if necessary; • Pride of ownership; • Feel more comfortable and have more privacy; • Stable mortgage payments; • More room and storage; • Improvement of buyer’s credit rating; • Income tax deductions for property taxes and mortgage interest; • Property may increase in value; • Free to make home improvements and have pets (items typically not allowed in rentals).

Disadvantages of Buying a house… • Large down payment; • Move-in costs; • Insurance costs; • Possible for property to decrease in value; • Time, money, and energy commitment; • Repair and maintenance costs; • Property taxes can raise substantially; • Money is tied up in the home; • May take several months to sell a home if trying to relocate. • Foreclosure is a possibility- homeowner doesn’t make monthly payments; Lender takes house back and sells it. • Limited mobility - Long term investment now; costly to sell after buying

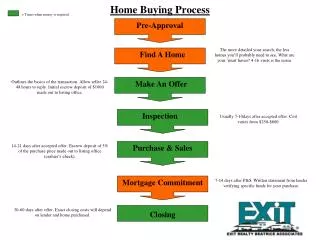

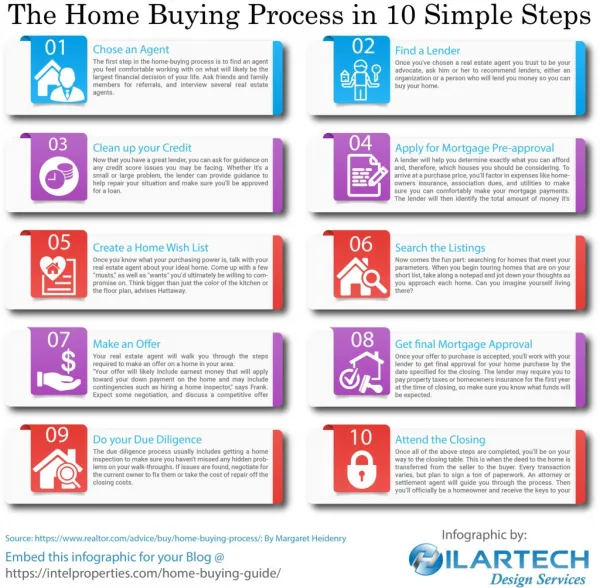

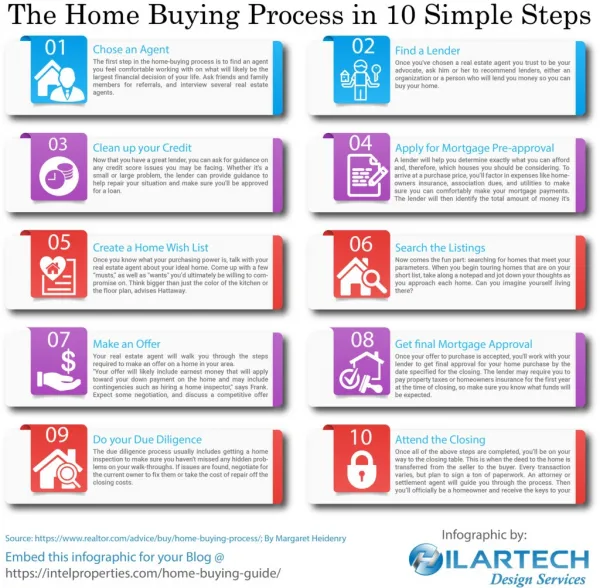

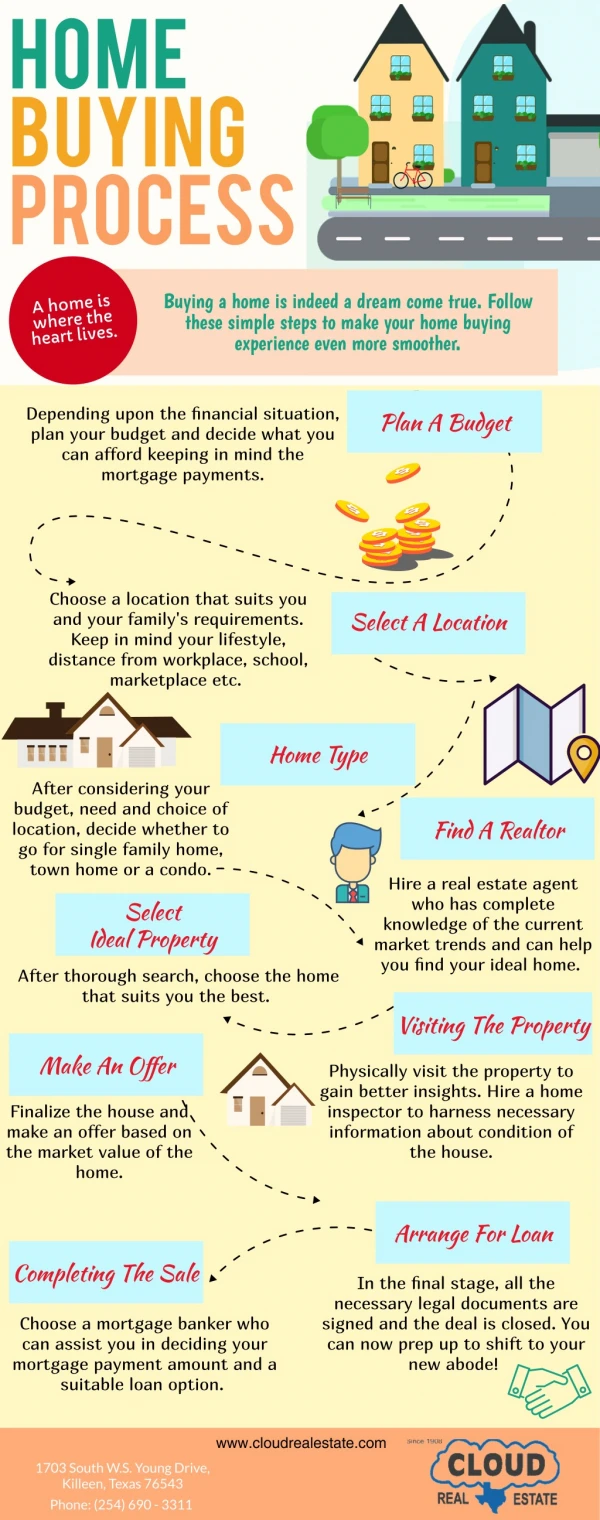

Steps In The Buying Process • 1) Discuss Finances– How much house can you afford? How much in savings? How much debt do you have? • 2) Have lender pre-qualify you. When you know how much you can pay per month, you can shop more efficiently. • 3) Agreement of Sale- A legally binding contract that the buyer and seller signs that states all of the conditions and specific terms of the sale. Includes detailed description of property, purchase price, amount of down payment, any items to be included in the sale (refrigerator, drapery, etc), how taxes are divided.

The Buying Process, Cont’d.. • 4) Earnest Money- Money that is given by the buyer to the seller that shows he/she is serious about buying the property ( can range from $100- thousands). The money is held until the closing and applied toward the final price of the home. • The buyer can lose the earnest money if he/she backs out of the agreement. • Survey – Must be completed before the sale in order to establish that the building on the land is actually the same as in the legal description, and what the correct boundary lines are.

The Buying Process, Cont’d • 6) Inspections- Several may be required by the lender or state, others are optional. • We have 2 main inspections… • General and termite. • General Home: Certified home inspector checks for structural soundness and insures that the plumbing, electrical and heating systems are working correctly. May also check roof, exterior/interior walls.

**What types of deterioration should a buyer be alert for when looking at an older home? • Answer: Worn wiring, plumbing, interior and exterior surfaces, leaking basement and roof, cracked walls and foundations, other structural problems; infestation by pests. • Termite: The most common required inspection. The seller is usually required to pay for this inspection and any repairs needed.

Closing Costs- vocabulary • Closing Costs: Costs associated with closing of the loan and transferring the property into the name of the buyer. Most are paid by the buyer, but there are fees that the seller is required to pay (ex. His share of taxes, insurance, real estate commission, etc.) • A. Title Search – Search to make sure that the seller actually holds the title to the property and no one else has any claims to the property; Reveals any debts held on the property. The buyer often purchases title insurancefor protection against errors in the title.

Closing Costs, Cont’d • B. Appraisal – Valuation of the property. This can determine how much the lender will loan for a mortgage. • C. Origination Fee: Fee paid to the lender for processing the loan. Usually 1% of the loan amount. • D. Attorney Fee: Money paid to the attorney to represent the buyer at the time of closing.

Financial Terms: Principal and Equity • Principal: It is the amount borrowed. • Interest is calculated on the principal. • In a loanamortization schedule, the principal and interest are separated, so you can see which part of your monthly payment goes to paying off the principal, and which part is used to pay interest. An "interest only" loan payment does not draw down (reduce) the principal. • Examples: • If you get a business loan for $100,000, this is the principal amount. • Equity: Difference between market value (MV) of a piece of property and the principal owed on the mortgage • Example: $150,000(MV)-$100,000 (principal) = 50,000 equity

Financial Terms/Mortgages: • A home loan • Lender agrees to loan money at a specified interest rate. • The Mortgage specifies… • the total amount to be paid, • the amount of interest to be paid • the amount of monthly payment to be paid. • A contract outlining the terms of a loan between the lender and the borrower

Mortgages cont. • 1) Conventional– most common type, usually 15 or 30 yr. term, usually fixed rate. • 2) FHA – insured mortgages: • They are 3 parties contracts that involve the borrower, lending firm and the Federal Housing Administration. This loan is insured by the federal government against the borrower defaulting (failing to pay) on the loan. Usually has a lower down payment, can be fixed or adjustable interest rate, any person can apply for this type loan.

Mortgages: • 3-VA loans-guarantee mortgages: Loans involving the borrower (A Veteran), a lending firm, and the Veterans Administration (VA). Veterans apply and their applications are submitted to a VA office. Congress sets eligibility requirements. • Cost less than other common fixed rate mortgages. • VA requires no down-payment, but the lender may.

Determining The Price Range of a House You Can Purchase: 1) Estimate what you can afford: • A. Multiply 2 ½ times your annualgross income (income before deductions). • This gives you the maximum amount of house you can afford. • Ex. If annual income is $40, 000. You should be able to afford $100,000 for a home (40,000X 2.5=100,000) • A person with many debts may not be approved based on this guideline.

Qualifying For A Loan: 2) Estimate How Much Money You Can Borrow: • Buyer must make down payment (usually 5% of the cost of the home). • Your earnings and your debt will determine the size of the loan. To qualify for a loan, two lender guidelines or ratios must be met: 1) Housing-to-Income Ratio-Your monthly housing costs should total no more than 28% of your gross monthly income. Monthly income 28%= monthly mortgage Housing costs include mortgage payment, property taxes, insurance, utilities (gas, water and electricity).

Qualifying For A Loan, Cont’d 2) Debt- to- Income Ratio-Total monthly debt is compared to total monthly income. • Your monthly housing costsplus otherlong term debts (ones that take 10 or more months to repay), should total nomore than 36 % of your monthly grossincome. • * Both of these ratios must be met for a buyer to be eligible for a loan.

Qualifying For A Loan Cont’d: • * Credit History – is kept by a central agency and includes the past payment record as well as a profile of outstanding debts. (Tells bank whether person is likely to repay the loan). People are considered “high risk” if their credit history indicates frequent late payments and high debt. • Can contact credit bureau (or consumer reporting agency )to obtain a copy of this record. • Escrow : money held in trust by a third party until a specified time