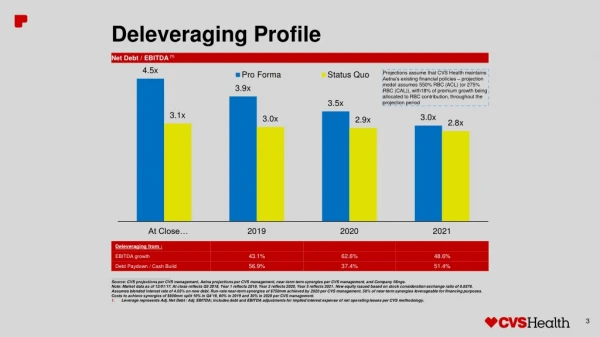

Download

1 / 9

90 likes | 294 Views

Eggertsson and Krugman Debt, Deleveraging, and the Liquidity Trap. All debt is not created equal. Borrowers want to spend more now than savers do That’s why they’re borrowers/debtors A deleveraging shock hits – a Minsky moment.

E N D

Eggertsson and KrugmanDebt, Deleveraging, and the Liquidity Trap All debt is not created equal. Borrowers want to spend more now than savers do That’s why they’re borrowers/debtors A deleveraging shock hits – a Minsky moment

Eggertsson and KrugmanDebt, Deleveraging, and the Liquidity Trap All debt is not created equal. Borrowers want to spend more now than savers do That’s why they’re borrowers/debtors A deleveraging shock hits – a Minsky moment Acceptable level of indebtedness falls Debtors must reduce spending…but creditors won’t spend enough to keep aggregate demand up The “natural rate of interest” corresponding to full employment becomes negative …but there’s a zero lower bound If interest rate could fall enough, savers would spend more The economy would expand, debtors would earn more and spend more too (a familiar IS relation) …but there’s a zero lower bound

Enter Fisher’s Debt Deflation Depression • Debtors must deleverage firesale price decline • Negative real interest rate would aid recovery • For real interest rate to become negative, people must expect inflation…for price level to recover from its low • Recall Temin-Wigmore/Eggertsson on New Deal and Reflation • Drop in prices increased burden of debt Now comes Upside-Down Demand Lower Price Increased burden Less spending by debtors …but with i = 0, savers won’t spend enough

“Backward bending” Aggregate DemandPrice down Burden of debt up Spending down P AD AS Y

Zero Lower Bound Paradoxes • Paradox of thrift • Additional saving can’t reduce interest rate below zero lower bound • Investment won’t increase when saving increases • Additional saving – less spending Output down • Reduced output Reduced income Reduced saving • So saving doesn’t increase after all

Zero Lower Bound Paradoxes: Paradox of toilPeople want to work more Aggregate Supply shifts outPrice Level Declines Burden of debt increasesOutput declines P AD AS0 AS1 Y

Zero Lower Bound Paradoxes: Paradox of flexibilityDeleveraging Shock Decrease in Aggregate DemandReduced Price Increased burden of debtOutput declines more when price is flexible than when it’s sticky P AD0 ASflexible ASsticky AD1 Y Recall Eggertsson’s defense of New Deal / NIRA Sticky wages and prices are “good”

Policy Implications • Monetary policy: raise inflationary expectations • Adopt a higher inflation target … lower real interest rate … but is this credible? (Time consistency problem) • Higher price lowers debt burden … thus it helps • Fiscal policy: more public debt can be solution to too much private debt • Ricardian equivalence doesn’t bind at zero lower bound • Liquidity constrained debtors’ spending depends on current income, not expectations of future income • They will spend to the limit • Keynesian multiplier increases when price increases • Stimulus is highly effective when AD slopes backwards