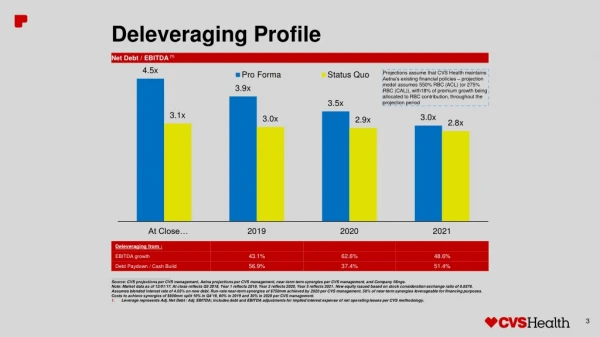

Download

1 / 14

140 likes | 269 Views

April 9, 2008. | The Great Deleveraging . In the Beginning there was Commercial Paper. 1869

E N D

1. The Great Deleveraging how the subprime crisis became a run on the bank

2. April 9, 2008 | The Great Deleveraging In the Beginning there was Commercial Paper 1869 � Marcus Goldman starts the company that will become Goldman Sachs and invents Commercial Paper.

From 1869 to 1975 the commercial paper market grew slowly and as late at 1975 there was only 48 billion outstanding.

It was primarily used by corporations to provide working capital.

Until the 1950�s most CP holders were banks.

In the 1950�s and 1960�s industrial firms began to hold CP as an alternative to bank deposits.

In the 1970�s money market funds were created by the 199o�s had become the dominant player in the CP market.

Because of the 1970 default by the Penn Central Transportation Company, the market insisted that almost all CP hold a short term rating by the rating agencies.

In order to obtain this rating commercial paper issuers had to obtain backup liquidity lines from banks.

Once money market funds, ratings, and liquidity lines had been institutionalized, commercial paper use grew rapidly

1980: 122BB, 1985: 294BB, 1990: 558BB and 2007: 1.3 trillion.

In 1983 the first Asset Backed Commercial Paper (ABCP) conduit was created.

This allowed firms to finance assets in a bankruptcy-remote entity.

SIV�s (structured investment vehicles) are a variant on ABCP conduits

By 1999 there was over 500BB of ABCP outstanding

3. April 9, 2008 | The Great Deleveraging Then, Wall Street Created the Asset Backed Security Before 1970, investors could only trade whole loans

1970: GNMA guaranteed the first mortgage pass through securities

They were quickly followed by FNMA and FRE (Freddie Mac)

1983: The first collateralized mortgage obligations were issued (CMO�s)

1985: Sperry Lease Finance Corporation creates the first asset backed security (ABS)

It was backed by computer equipment leases

Since 1985 the banks and investment banks have rushed to securitize any asset they can find with a cash flow that is easy to describe

CMBS, student loans, home equity loans, credit card receivables

Aircraft

Commodities

Insurance products, e.g. catastrophe bonds

By 2003 there was over 6 trillion dollars of asset backed paper outstanding

There have been periodic blow-ups in this market, usually involving securitizations of securitizations

CMO�s

CLO/CDO � squared

CDO of ABS

4. April 9, 2008 | The Great Deleveraging Finally, Bank Regulatory Standards were Codified Before Basel I banks were required to hold capital equal to a fixed percentage of assets

In the early 1980�s the United States began to adopt more sophisticated bank capital rules

In 1989 it adopted the Basel I accord

Capital requirements are defined based on simplified risk-based rules

Different financial institutions were regulated (or not) by different bodies, the rules for banks, investment banks, insurance companies, mutual funds, hedge funds, etc are all different and are not necessarily consistent

The capital rules tried to segregate risk into different types

Credit Risk

Interest Rate Risk

Market Risk

Insurance Risk

Liquidity Risk

5. April 9, 2008 | The Great Deleveraging Wall Street Abhors a Vacuum By the 1980�s the tools were in place for an explosion in financial product development

The commercial paper market made it possible to separate financing from asset ownership

The securitization market, and its child the derivatives market, made it possible to transform risk at will. By passing cash flows through a series of legal entities or transferring risk via contract one could change

The legal form

The accounting

The tax treatment

The regulatory treatment

An influx of quantitative and legal talent, coupled with cheaper computers, made it possible to create and model increasingly complex transactions

With the ability to separate financing, legal ownership, and risk taking a number of companies sprang up to play specialized roles such as

Origination

Warehousing

Structuring and Sales

Risk Taking

Financing

6. April 9, 2008 | The Great Deleveraging The Players Originators � banks, savings and loans, and mortgage companies that made the original mortgage loans.

Loan officers at these firms were viewed as salesmen and not as risk takers

Compensation was commission based

Loans were sold on as quickly as possible

Warehouse providers � loans were kept in warehouse facilities while enough volume was accumulated for a securitization. There were several types of warehouse

ABCP conduits

The balance sheets of banks

The balance sheets of mortgage companies

Usually financed via a total return swap with the bank that would ultimately create and distribute the bonds

Structurers � banks and investment banks that created securities

Large financial institutions that created the legal vehicles to

Own the loan pools

Service the loans

Segregate the cash flows into the appropriate bonds

Once the bonds were created, the structures sold them on to various risk takers and finance providers

7. April 9, 2008 | The Great Deleveraging More Players Equity Providers � banks and hedge funds

These people took the risk of the lowest (equity) tranche of the securitization

It was viewed as an equity investment and they required equity-like returns

Essentially, the investment is a leveraged purchase of the underlying loans with non-recourse financing

Senior Risk Takers � banks, insurance companies, mutual funds, and monoline insurance companies

These players are buying highly rated assets for cash flow.

Banks and insurance companies, they provide both the financing and the risk transfer

Monoline insurance companies provides only risk transfer and need a third party to finance the assets

Leverage providers � banks, insurance companies, mutual funds and conduits

All of these parties provide the cash needed to finance the assets.

They assume that there is little or no risk to repayment of cash and that they are only providing liquidity

The rating agencies

In exchange for a fee, these companies opine on the relative credit worthiness of borrowers.

A borrower may be an institution or it may be a special purpose vehicle

A borrower may not even borrow money. It may just be somebody who has to pay money out under certain circumstances.

All of the bonds, as well as the CP conduits and monoline insurance companies all required ratings to play the game

8. April 9, 2008 | The Great Deleveraging Risk and Reward Originators lend money to borrowers

Because they are selling the assets on very quickly, they have little or no incentive to make sure that the assets are of good quality.

As long as they follow the rules set by the warehouse provider and the rating agencies they know that the assets will quickly move off of their books

Warehouse providers earn carry off the assets while providing initial financing

Again, the primary risk management tool of these players is velocity.

As long as the assets are securitized quickly, there is no time for anything to go wrong

Structurers take only legal and compliance risk

They create the bonds and sell them

They earn structuring and underwriting fees

The primary risks that they take are either mis-selling or poor structuring which would result in them retaining risk that they thought was gone

Equity providers take the largest slice of the risk

In theory these players have the greatest incentive to do a full analysis of the terms

Senior Risk Providers and Leverage Providers rely on agency ratings to protect them

They generally do not have the capacity to analyze collateral in great detail

They use the rating agency analysis, sell side analysis and diversification as their primary tools for decision making

Rating agencies take a fee for an unbiased estimate of the credit risk in a transaction

9. April 9, 2008 | The Great Deleveraging The Game Originators make loans to unqualified borrowers

Usually done by making no income verification or no appraisal loans

Warehouse providers are happy to accept no-doc loans as they know that these loans are allowable collateral for securitizations

Structurers rely on their knowledge of rating agency and regulatory capital rules to create securitizations. For example:

An asset rated AAA requires only 1.6% capital on a bank�s balance sheet. While an asset rated below BBB requires 8% capital.

If you can get a rating agency to rate a bond AAA with less than 8% subordination then when you create the securitization you have freed up capital.

In the simplest case (which is not allowed), a bank could hold the equity and the senior piece of a securitization and hold less capital than it did if it just held the loans.

The extra income produced by the freed capital can be spread around to multiple players

As long as defaults don�t pass the equity layer of the structures everybody makes a higher return on capital.

10. April 9, 2008 | The Great Deleveraging The Problem Over time, money rushed into the sector to earn the excess returns.

As returns dropped investors required more and more leverage to make enough money

In order to get this leverage the ABS CDO was created

This took low rated tranches of ABS securitizations, threw them into a trust and re-securitzed them.

This created new equity and new AAA debt

This whole process relied on two key assumptions

The loan originators were making loans that were just as creditworthy as past loans had been

The system took away all incentive for this.

They got paid if the loans were good or bad

Acceptance of no-doc loans meant that they didn�t even need to ask the questions.

The rating agencies were correct about the ratings of the bonds and of the various parties

In order to rate the bonds they needed to get the default rates right within the original collateral class

They were wrong, but losses stayed within stressed parameters

In order to rate the CDOs they needed to get the correlations right among the various bonds in the trust

They got this horribly wrong and massively underestimated the correlation

11. April 9, 2008 | The Great Deleveraging What Went Wrong? The rating agencies were providing the tools to use less and less capital to support asset purchases

Each time the assets were re-securitized, this leverage went up.

In the end there were two highly leveraged classes of player that had massive exposure to any rating errors, the CP conduits and the monoline insurers

When defaults occurred in excess of prior experience, market players recognized this and began to mark down BBB rated ABS securities.

Because the BBB rated ABS securities were the collateral for ABS CDOs this mark-down led to losses in the junior tranches of the CDOs.

The correlations turned out to be much higher than those used in the ratings and the losses spread to AAA tranches

As soon as it became apparent that AAA assets were going to be downgraded in large numbers, we had the makings of a liquidity crisis

12. April 9, 2008 | The Great Deleveraging Out of Liquidity When it is likely that enough assets owned by monoline insurance companies will default, it causes their ratings to come into question and they get downgraded

Once an asset is downgraded below a minimum threshold, CP conduits have to liquidate that asset.

CP conduits were hit by a double whammy

They had to liquidate assets that were experiencing losses

They had to liquidate assets wrapped by monoline companies

Over 500BB dollars worth of assets had to be liquidated or taken back onto bank balance sheets

Because taking an asset back onto a balance sheet requires more regulatory capital than financing it, the banks had to liquidate other assets to make sure that they had enough capital

Because many assets were being liquidated at once, this had to be done at fire-sale prices

Because banks have to mark newly consolidated assets to market they had to take even bigger losses into earnings

The market for these securities ground to a halt

In order to restore their capital position, banks had to stop making loans or sell assets, often at a loss

Because nobody knew who owned which pieces of risk, trust broke down leading to general unwillingness to lend � even when capital was available.

13. April 9, 2008 | The Great Deleveraging The Great Deleveraging Every time an asset is moved onto a balance sheet or marked down it removes capital from the system.

In order to shore up capital, banks have been selling assets or taking back credit previously provided

Asset holders who can no longer obtain financing must sell those assets

There may be nothing wrong with the asset holder

There may be nothing wrong with the asset

There is simply no liquidity

Every time one person sells at a fire sale price, everyone else has to mark down their position and the cycle starts again

Eventually it stops because you get enough irrational pricing or because people go bankrupt

We have what appears to be irrational pricing now but we still have a lack of trust

This is why the Federal Reserve engineered the Bear Stearns takeover and allowed investment banks to borrow. They need to restore trust

Deleveraging has real world consequences

Our economy is built on credit. If people and businesses can�t get credit, they don�t invest

An asset bubble can create a realworld slow down.

14. April 9, 2008 | The Great Deleveraging What Can We Do? We need to take our medicine quickly.

The economy can�t rebuild until people are done taking their losses

This is the lesson of the Japanese bubble economy

We may need more government intervention

Left alone, each market participant, may, while acting in their own self interest, act in such a way as to exacerbate the problem.