Download

1 / 9

90 likes | 108 Views

Explore the nature of supply and the law of supply in economics, focusing on how producers determine quantity offered, maximize profits, and respond to price changes. Dive into the concepts of supply schedules, curves, elasticity, and different types of supply in various markets.

E N D

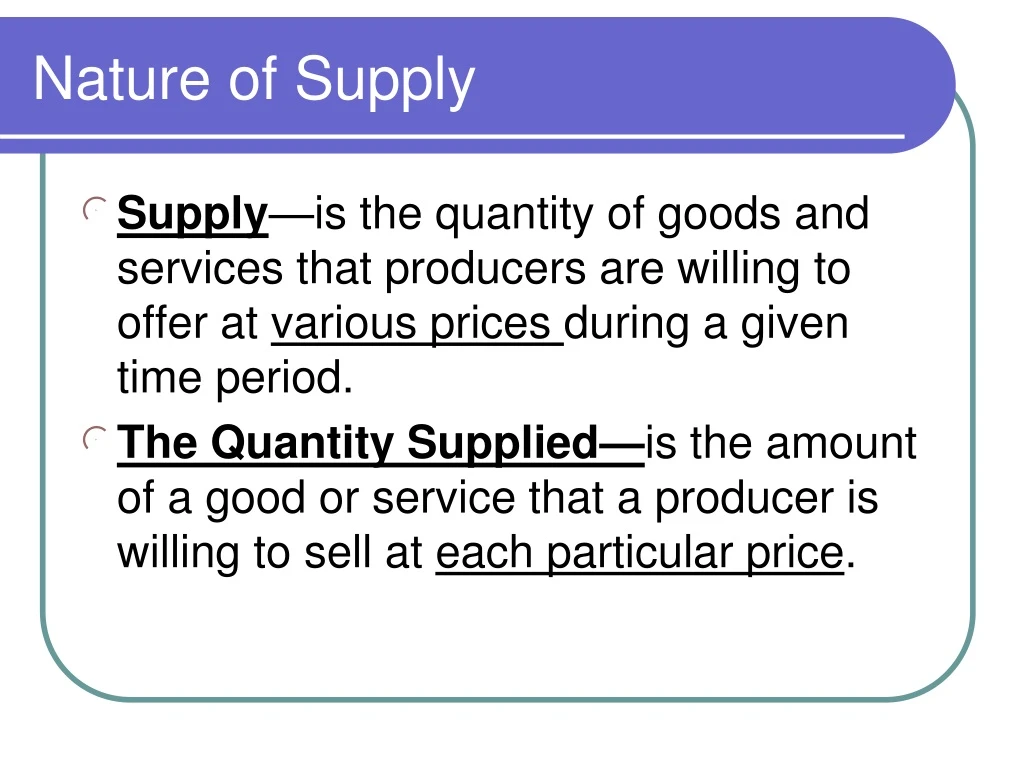

Nature of Supply • Supply—is the quantity of goods and services that producers are willing to offer at various prices during a given time period. • The Quantity Supplied—is the amount of a good or service that a producer is willing to sell at each particular price.

The Law of Supply • Law of Supply—States that producers supply more goods when they can sell them at higher prices and fewer goods when they must sell them at lower prices. • Why?

Profit • Profit—The amount of money remaining after producers have paid for all their costs. • Costs of Production—Include wages, rent, interest on loans, utility costs, raw materials, used to manufacture a product.

Profits and Markets • Profit motive helps direct the use of resources in the entire market. • Ex. Sell bicycles for $150 and company increases production(supply). • Encourages competition to increase its supply of $150 bikes. • Encourages new companies to start up. • All are pursuing profits!

Supply Schedules and Curves • Supply Schedule—Tool that shows the relationship between the price of a good and the quantity producers will supply. • Supply Curve--Plots on a graph the relationship between the price of a good supplied and the quantity producers will supply. • Note: Supply curve always slopes upward. • Note: Demand curve always slopes downward.

Elasticity of Supply • Elasticity of Supply—is the degree to which price changes affect the quantity supplied. • Elastic Supply—Exists when a small change in price causes a major change in the quantity supplied.

Elastic Supply • Products with elastic supply can be: • Made quickly • Inexpensively • Use a few readily available resources • Sports teams apparel—tee shirts,hats • Ex. Super Bowl championship • Demand soars, prices rise, supply increases.

Inelastic Supply • Inelastic supply—exists when a change in a goods price has little impact on the quantity supplied. • Inelastic supply if production requires: • Time • Money • Resources not readily available Ex. Gold, fine art, space shuttles, etc.

Inelastic Supply • Perfect inelastic supply exists when producers, regardless of price, cannot increase the quantity supplied. • Ex. Ocean front lots • 10 lots to sell—regardless of price • Can charge more $ but cannot produce more ocean front lots.