Download

1 / 39

390 likes | 413 Views

This informative presentation offers insights into the dynamics of the international insurance industry, particularly from the UK standpoint. It discusses developments in the UK market, including perspectives on Lloyd's, actuarial involvement, and changes in the operating and accounting environments. The emergence of major industry players, the role of Equitas, and shifts in Lloyd's capital base are highlighted. Additionally, the presentation touches on the complexities of converting to US GAAP, acquisition considerations for London Market companies, and practical issues in insurance reserving. The text sheds light on key factors influencing the insurance landscape and provides valuable knowledge for industry professionals.

E N D

International Insurance Reserving An Ocean of Difference

International Insurance • Attitudes • Legal Environments • Income Tax Laws • Evaluation Dates • Nationalism

Issues • Currency Conversion/ Devaluation • Data Differences • Environmental & Toxic Tort

International IssuesThe UK Perspective Peter Copeman PricewaterhouseCoopers

The UK Perspective • Developments in the UK market • Lloyd’s - an update • Actuarial involvement - including Lloyd’s opinions • Differences in operating environment • Differences in accounting basis • International standardisation

UK Market Developments • Consolidation of insurance industry • High level of M&A activity • Lloyd’s corporate capital • Emergence (and dominance?) of a few major players • Foreign ownership • Soft market • Increases in UK bodily injury awards

Equitas • Equitas established on 4 September 1996 • Reinsured 1992 and prior year liabilities of Lloyd’s syndicates • Largest ever reinsurance transaction • Proportionality conditions • Transition from 400 + syndicates to one company

Equitas - changes • Centralised claims handling • Administration being rationalised • Managing assets and liabilities

Changes in Lloyd’s Capital Base • Capital requirements for individual “names” increasing • Contribution of “names” to central fund increasing (0.6% è 1.5% of premiums) • Introduction of risk-based capital • Future of unlimited liability names? • General expectation that corporate capital share will increase

Lloyd’sOwnership and structural changes • Development of Integrated Lloyd’s Vehicles (“ILVs”) • US influence [50% + US/Bermuda ownership] • Future of “annual venture” under consideration • Currently Lloyd’s self-regulated • Lloyd’s to be regulated by new Financial Services Authority in the future

Actuarial involvement at Lloyd’s • Historically quite limited • Recent expansion of involvement • “problems of the past” • Equitas • Pressure from capital providers • Checks and balances for underwriters • Part of professionalism drive • Pricing involvement developing

Actuarial opinions at Lloyd’s 31 December 1996 • Opinions for syndicates writing US business • Submitted to NAIC and New York Insurance Department • Net reserves (total) • US situs trust funds

Actuarial opinions at Lloyd’s 31 December 1997 • UK solvency opinion for Corporation of Lloyd’s • > “best estimate” for UK solvency • “reasonable” for NAIC/NYID • Each economic entity (year) has separate opinion

Actuarial opinions at Lloyd’s 31 December 1998 • UK opinion extended to include:- • Bad debts • ULAE • Year 2000 comment required • Practising certificate to be introduced (effective 12.31.99)

Different Operating Environments London Market (incl. Lloyd’s) • “Subscription market” - risks shared widely • But, trends towards convergence and larger “lines” • Central administration • Historically, data poor…… but improving • Underwriter was king, now somewhat more balanced

Different Accounting Basis • Lloyd’s syndicates and some London Market companies on “funded” basis • Funded basis of accounting • result deferred for 3 years • data reported on an underwriting year basis • Conversion to US GAAP now required more often - can be a difficult task

Conversion to US GAAP • Data may not be immediately available • Requires different way of thinking for syndicates/companies • financial information required on accident year basis, split by underwriting year and currencies

Conversion to US GAAP • Identification of earnings patterns • Need for proper assessment of “open years” • Different conditions for “transfer of risk” on reinsurance • Various other differences of accounting treatment

Acquisition of London Market/ Lloyd’s Companies What to watch out for ! • Rapid changes in mix of business • Changes in underwriters • Opportunistic use of “cheap” reinsurance • Complex reinsurance programmes • Whole account covers • Unusual risks • Quality of data/management information

International Insurance Reserving: Some Practical Issues Mark Scully Tillinghast-Towers Perrin

Overview of Presentation • Data issues • Exchange rates • Varying definitions of a triangle • Clean-cut business • Latent claim exposures • Approach to reserving in Germany • Reserving standards in Europe

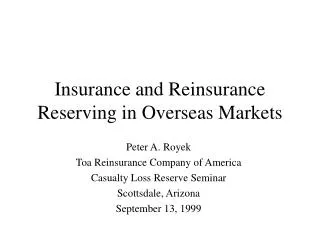

Exchange rate movements distort loss development data • Comparable to excessive inflation • Occur whenever triangles contain data • in different underlying currencies and • converted at historical exchange rates • Possible solutions are: • separate triangles by currency or • conversion using a single exchange rate • if development is similar or • volume too low to analyze separately

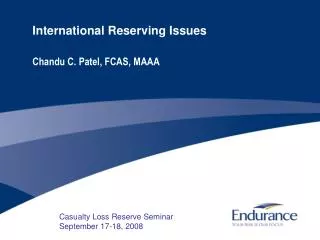

An Example of the Distorting Effect of Exchange Rate Changes • Business written in two countries: UK and Country A • Each country writes in local currency • Loss development features of business are identical in both countries

Cumulative Paid Losses and LDFs: Country A Business in Currency A

Conversion at a Single Exchange Rate Removes this Distortion

Exchange Rates: Final Observations • Actuaries not in business of predicting future exchange rates • Important to match liabilities with assets in same currency

Loss Development Triangles Must be Exactly Defined • “Moving triangles”, where claims are coded to year of original notification/cession • French construction liability business has three possible dimensions are possible (year of construction, accident year, report year) • German triangles often split data into two report year cohorts: • Accident year = Report year • Accident year < Report year (“late” claims)

“Clean Cut” Accounting year business cannot be analyzed in Triangles • An underwriting year is typically reinsured after 1 to 7 years into the current U/W year • Common in Europe with short tailed reinsurance business • When the cedent is in runoff, business reverts to normal • U/W years develop down not across the triangle

Material latent claim exposures have not yet emerged outside the US • Some asbestos claims in UK (through employers liability policies) • Large potential exposure to asbestos claims in France • Key latent claim risk is to U.S. exposures (e.g., through foreign subsidiaries, reinsurance)

Material latent claim exposures have not yet emerged outside the US • Some asbestos claims in UK (through employers liability policies) • Large potential exposure to asbestos claims in France • Key latent claim risk is to U.S. exposures (e.g., through foreign subsidiaries, reinsurance)

Claims Reserving in Germany • Minimal actuarial involvement (e.g., typically no annual review) • IBNR is formula driven; judgmental adjustments made to (large) case reserves • distorts incurred triangles • Industry is over-reserved in the aggregate

German runoff gains appear to correlate with accident year loss results Note: Runoff gain = Favorable development on prior loss reserves (here as % of premium)

German reserve levels vary substantially by segment (and company)

Reserving Standards in Europe • Currently no statutory requirement, minimal actuarial involvement • Stimuli for change: • European solvency regulations • National tax authorities • Actuarial organizations involved • Direction/Solution not yet clear but it’s “on the radar screen”

International Insurance Reserving An Ocean of Difference