Download

1 / 25

280 likes | 468 Views

2004 Casualty Loss Reserve Seminar Paul J. Struzzieri, FCAS Milliman, Inc. September 14, 2004. Reserving for Title Insurance. Outline. Introduction to Title Insurance Financial Reporting Issues Actuarial Challenges & Methods. I) Introduction to Title Insurance. Types of Policies

E N D

2004 Casualty Loss Reserve Seminar Paul J. Struzzieri, FCAS Milliman, Inc. September 14, 2004 Reserving for Title Insurance

Outline • Introduction to Title Insurance • Financial Reporting Issues • Actuarial Challenges & Methods Milliman

I) Introduction to Title Insurance • Types of Policies • Coverage • Unique Issues • Markets • Distribution • Reinsurance Milliman

Types of Title Insurance Policies • Purchase Mortgages • Lender Policy – based on $ amount of loan • Owners Policy – based on $ amount of purchase • Refinance Mortgages • Lender requires new policy • Owners keep original policy Milliman

Purchase vs. Refi Mortgages Milliman

Coverage • Lender’s and owner’s interests are protected • Cost to cure the defect; plus defense costs • Common title problems: • Defects, liens, easements – catch during search • Hidden hazards – undisclosed heirs, forged deeds • Unmarketability of title • Defalcations Milliman

Coverage Example #1 • Young couple buys home from widow (whose husband died without a will). • Widow’s son shows up and claims a share of the home. • Title insurance pays the missing heir the value of his share. Milliman

Coverage Example #2 • Just prior to closing, a prior lien is discovered. • For example, a paid but unreleased mortgage. • Purchaser can decide not to close based on this discovery. • Title insurance policy will respond if unmarketable. Milliman

Issues Unique to Title Insurance • Loss is “incurred” prior to policy issuance • No policy expiration date how to earn premium? • Goal of title search & examination = loss elimination • High expense ratios (90%+); low loss ratios (4-10%) Milliman

U.S. Market Share Milliman

International Markets • Canada • Australia • Europe Milliman

Distribution Channels • Agency Business (86%) • Independent Agents – including attorneys (59%) • Owned Agencies (27%) • Direct (14%) Milliman

Reinsurance • Typically excess of loss • Larger title insurers reinsure the others • Assumed and ceded = offset each other Milliman

II) Financial Reporting Issues • Financial Reporting • Form 9 • Statement of Actuarial Opinion • Categories of Statutory Reserves • Reserve Testing Milliman

Financial Reporting • Form 9 = Statutory Annual Statement • Schedule P • By Policy Year • By Report Year • Statement of Actuarial Opinion – since 1996 Annual Statement • Opine on Schedule P reserve, NOT booked reserve Milliman

Categories of Booked Reserves • Known Claims Reserve • Statutory Premium Reserve (SPR) = “Unknown” Claims • SPR Functions as Unearned Premium Reserve • Formula = Amount & Take-down Pattern • Supplemental Reserve Milliman

Reserve Testing • Compare Schedule P Reserve against Known Claims Reserve + SPR • Schedule P includes Known Claims, so really testing SPR vs. IBNR • If SPR > IBNR, book SPR • If IBNR > SPR, book SPR + Supplemental Reserve Milliman

Industry Reserves@ 12/31/03 • Known Claims = $556M • SPR = 3,258M Total = $3,814M • Schedule P = $2,741M Milliman

III) Actuarial Challenges • Title insurers do not know the number of policies in-force! • Correlation between calendar year loss emergence and mortgage rates • Refi policies have lower loss ratios than original title policies • Commercial vs. residential policies • New products Milliman

Actuarial Methods – Loss Development • Paid and incurred loss development triangles from Schedule P • Industry composite data available • Historical patterns can be distorted • Drop in interest rates leads to refi’s • When lender policy is refinanced, original policy is extinguished. • Try to adjust pattern Milliman

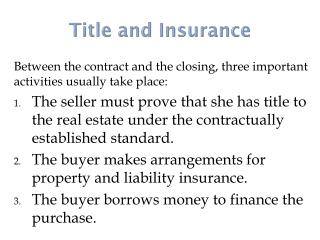

Actuarial Methods – Expected Loss Ratio • Expected Loss Ratio for refinance policy is lower than original policy • Policy Year with high refinance % expected to have lower loss ratio Milliman

Refi Percentage vs. Title Loss Ratio Milliman

Actuarial Methods – Expected Loss Ratio • Econometric modeling of Expected Loss Ratio – variables could include: • Mortgage rates • Refinance percentage Milliman

Actuarial Methods – Cape Cod or Bornhuetter-Ferguson • Combines Expected Loss Ratio and Development Methods. • To calculate Expected Losses, can use: • Premium • Amount of Insurance • Counts & Averages Milliman