Download

1 / 34

350 likes | 646 Views

Swaps Chapter 7. Nature of Swaps. A swap is an agreement to exchange cash flows at specified future times according to certain specified rules. An Example of a “Plain Vanilla” Interest Rate Swap.

E N D

Nature of Swaps A swap is an agreement to exchange cash flows at specified future times according to certain specified rules

An Example of a “Plain Vanilla” Interest Rate Swap • An agreement by Microsoft to receive 6-month LIBOR & pay a fixed rate of 5% per annum every 6 months for 3 years on a notional principal of $100 million • Next slide illustrates cash flows

---------Millions of Dollars--------- LIBOR FLOATING FIXED Net Date Rate Cash Flow Cash Flow Cash Flow Mar.1, 1998 4.2% Sept. 1, 1998 4.8% +2.10 –2.50 –0.40 Mar.1, 1999 5.3% +2.40 –2.50 –0.10 Sept. 1, 1999 5.5% +2.65 –2.50 +0.15 Mar.1, 2000 5.6% +2.75 –2.50 +0.25 Sept. 1, 2000 5.9% +2.80 –2.50 +0.30 Mar.1, 2001 6.4% +2.95 –2.50 +0.45 Cash Flows to Microsoft(See Table 7.1)

Converting a liability from fixed rate to floating rate floating rate to fixed rate Converting an investment from fixed rate to floating rate floating rate to fixed rate Typical Uses of anInterest Rate Swap

Intel and Microsoft (MS) Transform a Liability(Figure 7.2) 5% 5.2% Intel MS LIBOR+0.1% LIBOR

Financial Institution is Involved(Figure 7.4) 4.985% 5.015% 5.2% F.I. MS Intel LIBOR+0.1% LIBOR LIBOR Dealer spread = .03% evenly split

Intel and Microsoft (MS) Transform an Asset(Figure 7.3) 5% 4.7% Intel MS LIBOR-0.20% LIBOR

Financial Institution is Involved(See Figure 7.5) 4.985% 5.015% 4.7% F.I. MS Intel LIBOR-0.20% LIBOR LIBOR Dealer spread = .03 %

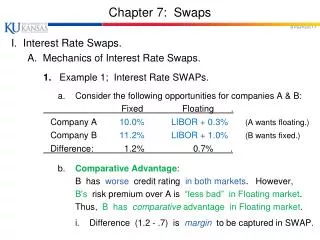

Fixed Floating AAACorp 4.0% 6-month LIBOR + 0.30% BBBCorp 5.2% 6-month LIBOR + 1.00% The Comparative Advantage Argument (Table 7.4) • AAACorp wants to borrow floating • BBBCorp wants to borrow fixed

The Comparative Advantage Argument • AAACorp has absolute advantage in both markets • But a comparative advantage in fixed • BBBCorp has comparative advantage in floating • If AAA borrows fixed, the gain is 1.2% • If BBB borrows floating, the gain is reduced by .7% • Therefore, we have a net gain of 1.2 - .7 = .5% • If the gain is split evenly, we have a gain per party of: G = (1.2 - .7)/2 = .25%

Swap Design • Design the swap so AAA’s borrowing rate equals the comparative disadvantage (CD) rate minus the gain: • LIBOR + .3 - .25 • Do the same thing for BBB • BBB’s rate with swap: • 5.2 - .25 = 4.95 • Now, draw the diagram

The Swap (Figure 7.6) 3.95% 4% AAA BBB LIBOR+1% LIBOR The floating rate leg should be LIBOR

Swap Design with FI • Adjust swap gain for dealer spread • Suppose dealer spread = .04% • Then gain: • G = (1.2 - .7 - .04)/2 = .23% • AAA’s rate with swap: • LIBOR + .3 - .23 = LIBOR + .07 • BBB’s rate with swap: • 5.2 - .23 = 4.97% • Draw swap diagram

The Swap when a Financial Institution is Involved (Figure 7.7) 3.93% 3.97% 4% AAA F.I. BBB LIBOR+1% LIBOR LIBOR Check that dealer spread = .04%

Criticism of the Comparative Advantage Argument • The 4.0% and 5.2% rates available to AAACorp and BBBCorp in fixed rate markets are 5-year rates • The LIBOR+0.3% and LIBOR+1% rates available in the floating rate market are six-month rates • BBBCorp’s fixed rate depends on the spread above LIBOR it borrows at in the future

Valuation of an Interest Rate Swap • Interest rate swaps can be valued as the difference between the value of a fixed-rate bond and the value of a floating-rate bond

Valuation in Terms of Bonds • The fixed rate bond is valued in the usual way • The floating rate bond is valued by noting that it is worth par immediately after the next payment date

An Example of a Currency Swap An agreement to pay 5% on a sterling principal of £10,000,000 & receive 6% on a US$ principal of $18,000,000 every year for 5 years

Exchange of Principal • In an interest rate swap the principal is not exchanged • In a currency swap the principal is exchanged at the beginning and the end of the swap

Three Cash Flow Components • t = 0: exchange principal based upon current exchange rates Pay: $18 M Rcv: £ 10 M • t = 1, 2, 3, 4, 5: Pay: .05x10 = £.5 M Rcv: .06x18 = $1.08 M • t = 5: Pay: £ 10 M Rcv: $ 18 M

The Cash Flows (Table 7.5) Dollars Pounds $ £ Years ------millions------ 0 –18.00 +10.00 +1.08 1 –.50 2 +1.08 –.50 3 +1.08 –.50 4 +1.08 –.50 5 +19.08 -10.50

Conversion from a liability in one currency to a liability in another currency Conversion from an investment in one currency to an investment in another currency Typical Uses of a Currency Swap

USD AUD General Motors 5.0% 7.6% Qantas 7.0% 8.0% Comparative Advantage Arguments for Currency Swaps (Table 7.6) General Electric wants to borrow AUD Qantas wants to borrow USD

Comparative Advantage • GE has absolute advantage in both markets • But GE has comparative advantage in dollars • Qantas has comparative advantage in Australian dollars • So GE should borrow dollars and Qantas Australian dollars • Then swap cash flows to earn gain from comparative advantage

Comparative Advantage • Gain per party: G = (2 - .4)/2 = .8% • GE’s rate with swap: 7.6 - .8 = AUD 6.8% • Qantas’ rate with swap: 7 - .8 = USD 6.2%

Qantas Assumes Exchange Rate Risk USD 5% USD 5% AUD 8.0% GE Qantas AUD 6.8%

GE Assumes Exchange Rate Risk USD 6.2% USD 5% AUD 8% GM Qantas AUD 8.0%

FI Assumes Exchange Rate Risk • Adjust swap gain for dealer spread • Suppose dealer spread = .2% • Then gain: • Gain per party: G = (2 - .4 - .2)/2 = .7% • GE’s rate with swap: 7. 6 - .7 = AUD 6.9% • Qantas’ rate with swap: 7 - .7 = USD 6.3%

FI Assumes Exchange Rate Risk USD 5% USD 6.3% USD 5% GE F.I. Q AUD 8% AUD 6.9% AUD 8% Check that dealer spread = .2% Pay: 13.0 – 11.9 = AUD 1.1% Rcv: 6.3 – 5.0 = USD 1.3%

Valuationof Currency Swaps Like interest rate swaps, currency swaps can be valued either as the difference between 2 bonds or as a portfolio of forward contracts

Swaps & Forwards • A swap can be regarded as a convenient way of packaging forward contracts • The “plain vanilla” interest rate swap in our example consisted of 6 Fraps • The “fixed for fixed” currency swap in our example consisted of a cash transaction & 5 forward contracts

Swaps & Forwards(continued) • The value of the swap is the sum of the values of the forward contracts underlying the swap • Swaps are normally “at the money” initially • This means that it costs nothing to enter into a swap • It does not mean that each forward contract underlying a swap is “at the money” initially

Credit Risk • A swap is worth zero to a company initially • At a future time its value is liable to be either positive or negative • The company has credit risk exposure only when its value is positive