Download

1 / 29

290 likes | 445 Views

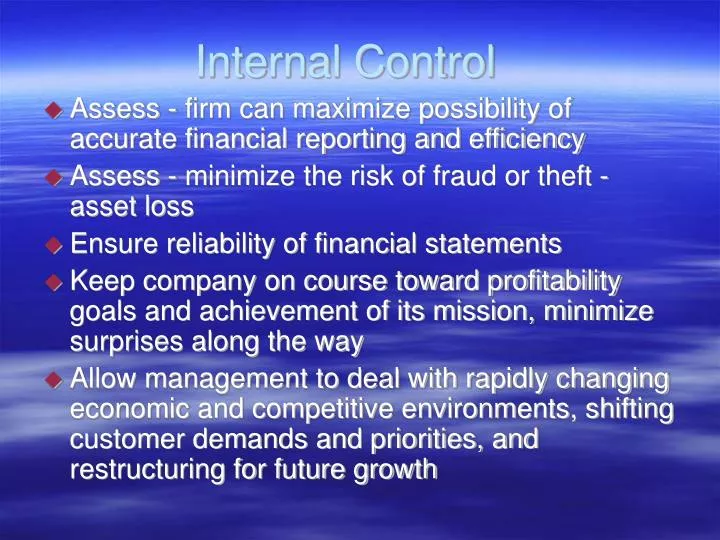

Internal Control. Assess - firm can maximize possibility of accurate financial reporting and efficiency Assess - minimize the risk of fraud or theft - asset loss Ensure reliability of financial statements

E N D

Internal Control • Assess - firm can maximize possibility of accurate financial reporting and efficiency • Assess - minimize the risk of fraud or theft - asset loss • Ensure reliability of financial statements • Keep company on course toward profitability goals and achievement of its mission, minimize surprises along the way • Allow management to deal with rapidly changing economic and competitive environments, shifting customer demands and priorities, and restructuring for future growth

Internal Control - defined • Process - provide reasonable assurance regarding achievement of objectives • Effectiveness and efficiency of operations - basic business objectives, performance and profitability goals and safeguarding of resources • Reliability of financial reporting - published financial statements • Compliance with applicable laws and regulations • Can do: help an entity achieve performance and profitability goals, prevent loss of resources, reliable financial reporting, comply with laws and regulations, help get to where it wants to go, avoid pitfalls and surprises along the way

Analyzing internal control Bemis Company is a rapidly growing start-up business. Its recordkeeper, who was hired one year ago, left town after the company’s manager discovered that a large sum of money had disappeared over the past six months. An audit disclosed that the recordkeeper had written and signed several checks made payable to her fiancé and then recorded the checks as salaries expense. The fiancé, who cashed the checks but never worked for the company, left town with the recordkeeper. As a result, the company incurred an uninsured loss of $84,000. Evaluate Bemis’s internal control system and indicate which principles of internal control appear to have been ignored. HELP!

Five interrelated components - how run business - integrated with the management process • Control Environment - tone of organization, control consciousness of employees - discipline, structure, integrity, • Risk Assessment - internal and external sources of risk to achievement of objectives • Control Activities - policies and procedures - management directives are carried out, actions are taken • Information and Communication - pertinent information - identified, captured and communicated - people carry out responsibilities • Monitoring - assess quality over time

Control Environment • Integrity and ethical values • Commitment to competence • Participation of board of directors or audit committee • Management’s philosophy and operating style • Organizational structure • Assignment of authority and responsibilities • Human resource policies and practices

Risk Assessment • Changes may occur in the operating environment • New personnel may become involved • Information systems may change • Rapid growth • New technologies • New products or services • Restructuring • Foreign operations • New accounting pronouncements

Control Activities • Segregation of duties • Proper authorization • Assets safeguarded • Compare actual to books • Employees of integrity • Record properly and on a timely basis

Information and Communication • Identify and record all valid transactions • Provide timely description of transactions • Properly measure transactions • Record transactions in a timely manner

Monitoring • Assess controls on a timely basis and make modifications when appropriate. • Use internal auditors to review • Test controls

Other factors to consider • Size of organization • Ownership characteristics • Nature of business • Diversity and complexity of activities • Data processing methods • Legal and regulatory environment of the business

Under Sarbanes Oxley Act • CEO and CFO certification • CEO - ultimately responsible - ownership of system, sets tone at top, provide leadership, direction • Board of directors - provide governance, guidance, oversight • Management - accountable - board of directors • Responsibility of everyone - part of job description • Internal control report • Document system so others can review • SEC will review every 3 years

CEO, CFO Certification • Explicitly must evaluate and report on effectiveness of internal control • Disclose to audit committee any material deficiencies in financial controls • Report any changes in IC • Report any corrective actions

CEO, CFO Report • Assess effectiveness within 90 days of filing dates • Design disclosure controls and procedures “ ..are intended to cover a broader range of information than is covered by internal controls related to financial reporting.. They are intended to ensure that an issuer maintains commensurate procedures for gathering, analyzing and disclosing all information that is required to be disclosed…”

Internal Control Report • A part of annual report • Management responsible for internal control • States a conclusion on the effectiveness of IC • External auditor has to attest to company’s internal control under PCAOB rules (Public Company Accounting Oversight Board)

Capital Budgeting • Planning process used to determine a firm’s long term investments • Insure that firms have assets that will be profitable • Before purchase asset - analysis, using estimates of performance - earn some minimum return • Does not want new asset to dilute ROI, ROE

Capital Budgeting • Methods - not consider time value of money: • Payback period - length of time to recover the cost of an investment • Using estimates of yearly profits • = cost of project/annual cash inflows • I.e. - if a project costs $100,000 and was expected to return $20,000 annually, the payback period would be $100,000/$20,000, or five years • ROI - using estimates of sales, costs, etc. - determine if the return on investment is higher than cost of capital • Ratio of money gained or lost on an investment relative to the amount of money invested • I.e. - $1,000 investment earns $50 profit = 50/1,000 = 5%, compared to $100 investment earns $20 profit = 20/100 = 20%

Capital Budgeting • If appears to be profitable - more complex capital budgeting analysis is done • NPV - net present value - using expected returns and cost of capital, add value to firm after making the required cost of capital • Measures excess or shortfall of cash flows • Year 1 - Interest: $100 * 10% = $10 + $100 = $110 • NPV: $110 / 1.1 = $100 • Year 2 – Interest: $110 + ($110 * 10 %) = $11 + $110 = $121 • NPV: $121/(1.1 * 1.1) = $100 • IRR - internal rate of return - equates the estimated profits to the cost to see what rate of return actually is • Annualized effective compound return rate earned on invested capital - yield on investment • Good investment if greater than alternative investment

Capital Budgeting • What needed to compute either NPV or IRR • Expected revenues • Expected cash outflow for costs • Salvage values, if any • Cost of capital or required rate of return • Tax rate • Tax shield from depreciation expense • Layout each year’s profit and lost, discount to the present and see if the value added is more than cost of project • Discount rate? • Actual cost of financing • Agreed upon rate of return • Weighted average cost of capital • Current return on assets amount

Read Introduction to Internal Control Process, • Download Cap. BudgProb.xls - print all tabs, • Download Capital Budgeting Problems.doc - print, • Assign #5 - Internal Control Report - 3-4 pages, (due 2/24, 2/25) – include firm, interview date, observation time, name of person and title interviewed, how effective? Opinion, suggestions – include headings • Assign #6 - Turnover ratios - Target - Asset Turnover, Inventory Turnover, Days in Inventory, A/R Turnover, Days in Receivable, Accounts Payables Turnover, Days in Payables, Operating Cycle – 07-05 (due 2/8-W, 2/4-R).

Assign #7 - Solvency Ratios for Target, Inc - Debt/Assets, L/T Debt/Assets, Debt/Equity, Times Interest Earned, Leverage for years 07-05 (due 2/17, 2/18); • Leverage ratio = total liability and equity/ total equity • Download - Financial Leverage worksheet • Download – Capital Budgeting Problem