Download

1 / 45

450 likes | 476 Views

Learn how to calculate future and present value with compound interest for single sums and annuities. Includes formulas, examples, and practical applications.

E N D

A D ppendix Compound Interest

Objectives 1. Understand simple interest and compound interest. 2. Compute and use the future value of a single sum. 3. Compute and use the present value of a single sum. 4. Compute and use the future value of an ordinary annuity. 5. Compute and use the future value of an annuity due.

Objectives 6. Compute and use the present value of an ordinary annuity. 7. Compute and use the present value of an annuity due. 8. Compute and use the present value of a deferred ordinary annuity. 9. Explain the conceptual issues regarding the use of present value in financial reporting.

Simple Interest Simple interest is interest on the original principal regardless of the number of time periods that have passed. Interest = Principal x Rate x Time

Compound Interest Compound interest is the interest that accrues on both the principal and the past unpaid accrued interest.

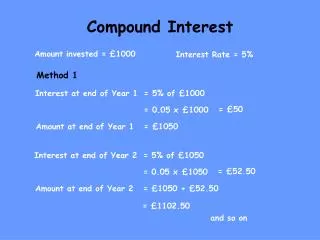

Compound Interest Value at End of Quarter Value at Beginning of Quarter Compound Interest Period x Rate x Time = 1st qtr. $10,000.00 x 0.12 x 1/4 $ 300.00 $10,300.00 2nd qtr. 10,300.00 x 0.12 x 1/4 309.00 10,609.00 3rd qtr. 10,609.00 x 0.12 x 1/4 318.27 10,927.27 4th qtr. 10,927.27 x 0.12 x 1/4 327.82 11,255.09 5th qtr. 11,255.09 x 0.12 x 1/4 337.65 11,592.74 Compound interest on $10,000 at 12% compounded quarterly for 5 quarters………………………... $1,592.74

How much will be in the savings account (the future value) on this date? $1,000 is invested on this date Dec. 31, 2001 Dec. 31, 2003 Dec. 31, 2000 Dec. 31, 2002 Dec. 31, 2004 Future Value of a Single Sum at Compound Interest One thousand dollars is invested in a savings account on December 31, 2000. What will be the amount in the savings account on December 31, 2004 if interest at 14% is compounded annually each year?

Future Value of a Single Sum at Compound Interest (1) (2) (3) (4) Annual Future Value Value at Compound at End Beginning of Interest of Year Year Year (Col. 2 x 0.14) (Col. 2 + Col. 3) 2001 $1,000.00 $140.00 $1,140.00 2002 1,140.00 159.60 1,299.60 2003 1,299.60 181.94 1,481.54 2004 1,481.54 207.42 1,688.96

Future Value of a Single Sum at Compound Interest Formula Approach n ƒ= p(1 + i) where ƒ = future value of a single sum at compound interest i and n periods p =principal sum (present value) i = interest rate for each of the stated time periods n = number of time periods

Ƒn=4, i=14 = (1.14) 4 f= $1,000(1.688960) = $1,688.96 Future Value of a Single Sum at Compound Interest Formula Approach f=p(1 + i) n

Future Value of a Single Sum at Compound Interest Table Approach This time we will use a table to determine how much $1,000 will accumulate to in four years at 14% compounded annually.

Future Value of a Single Sum at Compound Interest Table Approach Using Table 1 (the future value of 1) at the end of Appendix D, determine the table value for an annual interest rate of 14 percent and four periods.

Future Value of a Single Sum at Compound Interest Table Approach n 8.0% 9.0% 10.0% 12.0% 14.0% 16.0% 1 1.080000 1.090000 1.100000 1.120000 1.140000 1.160000 2 1.166400 1.188100 1.210000 1.254400 1.299600 1.345600 3 1.259712 1.295029 1.331000 1.404928 1.481544 1.560896 4 1.360489 1.411582 1.464100 1.573519 1.688960 1.810639 5 1.469328 1.538624 1.610510 1.762342 1.925415 2.100342 6 1.586874 1.677100 1.771561 1.973823 2.194973 2.436396 1.688960

Future Value of a Single Sum at Compound Interest Table Approach One thousand dollars times 1.688960 equals the future value, or $1,688.96.

$1,000 (the present value) must be invested on this date $1,688.96 will be received on this date Dec. 31, 2001 Dec. 31, 2003 Dec. 31, 2000 Dec. 31, 2002 Dec. 31, 2004 Present Value of a Single Sum If $1,000 is worth $1,688.96 when it earns 14% compounded annually for 4 years, then it follows that $1,688.96 to be received in 4 years from now is worth $1,000 now at time period zero.

1 (1 + i) n Present Value of a Single Sum Formula Approach p = f Where p = present value of any given future value due in the future ƒ = future value i = interest rate for each of the stated time periods n = number of time periods

pn=4, i=14 = = 0.592080 p= $1,688.96(0.592080) = $1,000.00 1 (1 .14) 4 Present Value of a Single Sum Formula Approach

Present Value of a Single Sum Table Approach Find Table 3, the present value of 1, at the end of Appendix D. Use 14% and four periods to obtain the table value.

Present Value of a Single Sum Table Approach n 8.0% 9.0% 10.0% 12.0% 14.0% 16.0% 1 0.925926 0.917431 0.909091 0.892857 0.877193 0.862069 2 0.857339 0.841680 0.826446 0.797194 0.769468 0.743163 3 0.793832 0.772183 0.751315 0.711780 0.674972 0.640658 4 0.735030 0.708425 0.683013 0.635518 0.592080 0.552291 5 0.680583 0.649931 0.620921 0.567427 0.519369 0.476113 6 0.630170 0.596267 0.564474 0.506631 0.455587 0.410442 0.592080

Present Value of a Single Sum Table Approach $1,688.96 times 0.592080 equals $1,000.

Dec. 31, 2001 Dec. 31, 2003 Dec. 31, 2000 Dec. 31, 2002 Future Value of an Ordinary Annuity Debbi Whitten wants to calculate the future value of four cash flows of $1,000, each with interest compounded annually at 14%, where the first cash flow is made on December 31, 2000. The future value of an ordinary annuity is determined immediately after the last cash flow $1,000 $1,000 $1,000 $1,000

n (1 + i) - 1 = C F o Future Value of an Ordinary Annuity Formula Approach i Where F =future value of an ordinary annuity of a series of cash flows of any amount C = amount of each cash flow n =number of cash flows i =interest rate for each of the stated time periods o

4 (1 .14) - 1 = 4.921144 = n=4, i=14 = F F o o 0.14 = $1,000(4.921144) = $4,921.14 Future Value of an Ordinary Annuity Formula Approach

Future Value of an Ordinary Annuity Table Approach Using the same data--four equal annual cash flows of $1,000 beginning on December 31, 2000 and an interest rate of 14 percent. Go to Table 2, the future value of an ordinary annuity of 1. Read the table value for n equals 4 and i equals 14%.

Future Value of an Ordinary Annuity Table Approach n 8.0% 9.0% 10.0% 12.0% 14.0% 16.0% 1 1.000000 1.000000 1.000000 1.000000 1.000000 1.000000 2 2.080000 2.090000 2.100000 2.120000 2.140000 2.160000 3 3.246400 3.278100 3.310000 3.374400 3.439600 3.505600 4 4.506112 4.573129 4.641000 4.779328 4.921144 5.066496 5 5.866601 5.984711 6.105100 6.352847 6.610104 6.877135 6 7.335929 7.523335 7.715610 8.115189 8.535519 8.977477 4.921144

Future Value of an Ordinary Annuity So, cash flow of $1,000 each at 14% at the end of 2000, 2001, 2002, and 2003 will accumulate to a future value of $4,921.14. $1,000 x 4.921144 = $4,921.14

How much will be in the fund on this date, which is 1 period after the last cash flow in the series? Future Value of anAnnuity Due Solutions Approach $1,000 $1,000 $1,000 $1,000 Dec. 31, 2001 Dec. 31, 2003 Dec. 31, 2000 Dec. 31, 2002

Future Value of anAnnuity Due Solutions Approach Step 1: In the ordinary annuity table (Table 2), look up the value of n + 1 cash flows at 14% or the value of 5 cash flows at 14%.

Future Value of anAnnuity Due Solutions Approach n 8.0% 9.0% 10.0% 12.0% 14.0% 16.0% 1 1.000000 1.000000 1.000000 1.000000 1.000000 1.000000 2 2.080000 2.090000 2.100000 2.120000 2.140000 2.160000 3 3.246400 3.278100 3.310000 3.374400 3.439600 3.505600 4 4.506112 4.573129 4.641000 4.779328 4.921144 5.066496 5 5.866601 5.984711 6.105100 6.352847 6.610104 6.877135 6 7.335929 7.523335 7.715610 8.115189 8.535519 8.977477 6.610104

Step 2: Subtract 1 without interest. (1.000000) 5.610104 Future Value of anAnnuity Due Solutions Approach Step 1: In the ordinary annuity table (Table 2), look up the value of n + 1 cash flows at 14% or the value of 5 cash flows at 14%. 6.610104

Fd = $1,000(5.610104) = $5,610.10 Future Value of anAnnuity Due Solutions Approach Step 3: Multiply the amount of each cash flow ($1,000) by the table value.

Dec. 31, 2002 Dec. 31, 2004 Dec. 31, 2001 Dec. 31, 2003 Present Value of anOrdinary Annuity Table Approach Kyle Vasby wants to calculate the present value on January 1, 2001 (one period before the first cash flow) of four future withdrawals (cash flows) of $1,000 each, with the first withdrawal being made on December 31, 2001. Assume again an interest rate of 14%. $1,000 $1,000 $1,000 $1,000

Present Value of anOrdinary Annuity Table Approach Using the same data, we have four equal annual cash flows of $1,000 beginning on December 31, 2000. The interest rate is 14 percent. Go to Table 4, the present value of an ordinary annuity of 1. Read the table value for n equals 4 and i equals 14%.

Present Value of anOrdinary Annuity Table Approach n 8.0% 9.0% 10.0% 12.0% 14.0% 16.0% 1 0.925926 0.917431 0.909091 0.892857 0.877193 0.862069 2 1.783265 1.759111 1.735537 1.690051 1.646661 1.605232 3 2.577097 2.531295 2.486852 2.401831 2.321632 2.245890 4 3.312127 3.239720 3.169865 3.037349 2.913712 2.798181 5 3.992710 3.889651 3.790787 3.604776 3.433081 3.274294 6 4.622880 4.485919 4.355261 4.111407 3.888668 3.684736 2.913712

Present Value of anOrdinary Annuity Table Approach One thousand dollars times 2.913713 equals $2,913.71. So, the present value of this ordinary annuity is $2,913.71.

Present Value of an Annuity Due Table Approach Barbara Livingston wants to calculate the present value of an annuity on December 31, 2000, which will permit four annual future receipts of $1,000 each, the first to be received on December 31, 2000. $1,000 $1,000 $1,000 $1,000 Dec. 31, 2002 Dec. 31, 2004 Dec. 31, 2001 Dec. 31, 2003

Present Value of an Annuity Due Table Approach Step 1: In the ordinary annuity table (Table 4), look up the value of n - 1 cash flows at 14% or the value of 3 cash flows at 14%.

Present Value of an Annuity Due Table Approach n 8.0% 9.0% 10.0% 12.0% 14.0% 16.0% 1 0.925926 0.917431 0.909091 0.892857 0.877193 0.862069 2 1.783265 1.759111 1,735537 1.690051 1.546661 1.605232 3 2.577097 2.531295 2.485852 2.402831 2.321632 2.245890 4 3.312127 3.329720 3.159865 3.037349 2.913712 2.798181 5 3.992710 3.889651 3.790787 3.604776 3.443081 3.274294 6 4.622880 4.485919 4.355261 4.111407 3.888668 3.684736 2.321632

Step 2: Add 1 without interest. 1.000000 3.321632 Present Value of an Annuity Due Table Approach Step 1: In the ordinary annuity table (Table 4), look up the value of n - 1 cash flows at 14% or the value of 3 cash flows at 14%. 2.321632

Present Value of an Annuity Due Table Approach One thousand dollars times 3.321632 equals $3,321.63. So, this is the present value of an ordinary annuity due.

Present Value of a Deferred Ordinary Annuity Table Approach Helen Swain buys an annuity on January 1, 2001 that yields her four annual payments of $1,000 each, with the first payment on January 1, 2005. The interest rate is 14% compounded annually. What is the cost of the annuity?

The present value of the deferred annuity is determined on this date $1,000 $1,000 $1,000 $1,000 Jan. 1, 2005 Jan. 1, 2006 Jan. 1, 2008 Jan. 1, 2007 Jan.1, 2001 Jan. 1, 2002 Jan. 1, 2003 Jan. 1, 2004 $1,000 x 2.913712(n=4, i=14) = $2,913.71 Present Value of a Deferred Ordinary Annuity Table Approach

The present value of the deferred annuity is determined on this date $2,913.71 x 0.674972 = $1,966.67 Present Value of a Deferred Ordinary Annuity Table Approach $2,913.71 Jan.1, 2001 Jan. 1, 2002 Jan. 1, 2003 Jan. 1, 2004

Present Value of a Deferred Ordinary Annuity If Helen buys an annuity for $1,966.67 on January 1, 2001, she can make four equal annual $1,000 withdrawals (cash flows) beginning on January 1, 2005.

A D ppendix The End