Download

1 / 15

150 likes | 247 Views

Rating Initiative. AMT Microfinance Investor ´s Fair Nairobi 21-22 October 2009. Introduction.

E N D

Rating Initiative AMT MicrofinanceInvestor´s Fair Nairobi 21-22 October 2009

Introduction • The Rating Initiative is managed by ADA and was launched in Sept 2008 with the support of Luxembourg Cooperation, SDC, MIL, Oxfam Novib, the Principality of Monaco, the Development Bank of Austria, SPTF, BlueOrchard and ResponsAbility. • The Rating Initiative is designed to encourage at least 800 new MFIs to engage in regular financial and social ratings. Over 140 ratings fundedsinceSeptember 2008 !!

Rating Initiative objectives • Objective 1: Promote and contribute to the establishment of a financially viable, sustainable microfinance rating market by co-funding: • Financial ratings (and mini-ratings) • Social ratings (standard and SR with client survey) • Integrated ratings (whenestablished) • Objective 2: Address in the long term the lack of available, transparent information for MFIs, funders and stakeholders • Objective 3: Ensure the availability of market studies on the microfinance rating sector in general.

Global co-funding results Total number of ratings approved as of September 30th 2009

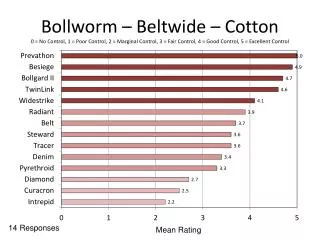

Distribution of products • In 2008, approved financial ratings (peformance and mini-ratings) were considerably higher than social ratings. • In 2009, approved social ratings are almost two times higher than financial ratings.

Geographical distribution • For financial ratings, the Initiative approved the majority of co-funded ratings in Africa (59%). • For social ratings, the Initiative approved 47% of co-funded ratings in LAC and 29% in Africa.

Whocanapply?Eligibilitycriteria for AfricanMFIs • Eligibilitycriteria for all products(except mini-ratings) • Over 3 years of financialoperations (2 years for social ratings) • Averageloan size of lessthan €3,200 • Total assetsbetween €200,000 and €10,000,000 (no maximum assetceiling for social ratings) • No mandatoryexerciserequired by local regulation • Eligibilitycriteria for mini-ratings • Over 2 years of financialoperations • Averageloan size of lessthan €3,200 • Total assetsbetween €150,000 and €10,000,000 • No mandatoryexerciserequired by local regulation

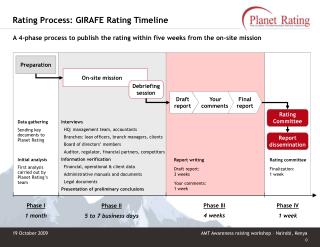

The MFI identifies its needs and chooses a product and then selects a suitable rater and negotiates a price 2 1 The MFI applies to the Rating Initiative. The Rating Initiative pays the amount agreed upon to the MFI How to Apply 1 2 3 5 The Rating Initiative reviews the application on the basis of MFI eligibility criteria and issues a co-funding commitment to the MFI The Rating Initiative pre-approves a number of firms to ensure a basic level of quality in the rating services purchased by the MFIs 4 After the rating/assessment, the MFI submits required rating documentation for reimbursement to the Rating Initiative

Step 1: Select a rating agency The MFI should: - contactseveral rating agencies and learnabouttheirproducts. -negociate and askforanestimate of the total cost of the rating exercise. - selectthe final rating agency. SpecialisedRaters • M-CRIL • Microfinanza Rating • MicroRate • PlanetRating Mainstream Raters • Fitch Ratings • CRISIL • JCR-VIS Rating agencies operating in Africa.

Step 2: Apply to the Rating Initiative • Rating Initiative co-fundingscales for Africa • The Rating Initiative reviews applications on a first-come, first-served basis. • The grantamountisdeterminedaccording to the principle of cost-sharing and the followingco-funding table:

Apply to the Rating Initiative (continued) • A complete applicationconsists of the following items: • The Rating Initiative application form • The Rating Initiative certification letter. • A copy of yourmostrecentfinancialstatements, including the externalauditor´s report (if any). • A copy of any ratings or evaluationswithin the past 12 months (if any). • A proposal for the total cost of carrying out the exercisefromtwo rating agencies.

Step 3: Reimbursementprocess • Uponreceipt of the final rating report and other relevant reimbursement documents, the Rating Initiative willpublish the report and reimburse the fundsdirectly to the MFI. • For a first rating you are encouraged but not obliged to publishyour full report on the Rating Initiative website.

For more information All the requiredapplication and reimbursementformscanbedownloadedfrom the website (www.ratinginitiative.org – availablesoon) or requested by email. The completedformsshouldbe sent, preferably by email, to: admin@ratinginitiative.org Or to the following postal address: The Rating Initiative c/o ADA 21, Allée Scheffer L-2520 Luxembourg Tel: (+352) 45 68 68 25 Fax: (+352) 45 68 6868

Contacts Benjamin Mackay, Administrator admin@ratinginitiative.org Phone: 00 352 45 68 68 25 Rating Initiative partners: • Luxembourg Development Cooperation • Swiss Development Cooperation (SDC) • OesterreichischeEntwicklungsbank (OeEB), Development Bank of Austria • The Principality of Monaco • The Microfinance Initiative Liechtenstein (MIL) • Oxfam-Novib • The Social Performance Task Force (SPTF) • BlueOrchard • ResponsAbility