Download

1 / 24

240 likes | 379 Views

Precautionary Saving and the Marginal Propensity to Consume. Risk and Choice Conference in Honor of Louis Eeckhoudt. The 5 th and 6 th derivatives.

E N D

Precautionary Saving and the Marginal Propensity to Consume Risk and Choice Conference in Honor of Louis Eeckhoudt

The 5th and 6th derivatives Whenever I see Larry Summers, he asks me “How is the 6th derivative doing?” or sometimes “How is the 5th derivative doing?” In my work, I have been detained by the 1st, 2nd, 3rd, and 4thderivatives and haven’t had a chance to deal with the 5th or 6th in any significant way. But thanks to the work of Louis and Harris, and others they have inspired, next time I see Larry I can report that the 5th and 6th derivatives are doing very well.

Christening Negativity of the 6th Derivative • As one of the few economists who also has a Linguistics degree, I have taken a great interest in terminology. I apologize if as a referee I have been too bossy on that front. In any case, I am not going to stop now. • In honor of Louis, I want to christen the sign of the 6th derivative on this Friday the 13th, 2012.

Christening Negativity of the 6th Derivative • A big enough negative 6th derivative ought to mean that a background risk will make two other risks interact more negatively—that is a background risk would tend to raise temperance. • Alternatively, a negative enough 6th derivative suggests that two background risks working together will have a more than additive effect on a third risk.

Christening Negativity of the 6th Derivative • Both of these ways of talking about the meaning of a negative 6th derivative make me think of someone being bowed down by the risk(s) he or she already has and not wanting to take on more. • A negative 6th derivative also tends to give the utility function a more kinked look, in a rounded off way.

Bent Utility • Therefore, I propose calling a utility function with a negative 6th derivative a “bent” utility function, and the property of having a negative 6th derivative “bentness.” • If you all agree, given the group here, it will be so, and we will remember that the 6th derivative was named at a moment to honor Louis.

The 4th Derivative and Multiperiod Models • My paper today is about the 4th derivative. • I have been working in other areas such as business cycle theory, the economics of happiness, and empirical studies of survey measures of risk aversion, but I haven’t abandoned mathematical studies of the economics of risk. • My main efforts in the last few years have been on how to extend 1- and 2-period results to the multiperiod case, as Fama did for a negative second derivative of the value function Sibley and Miller did for a positive third derivative and decreasing absolute risk aversion.

The 4th Derivative and Multiperiod Models • In this paper, I want to extend decreasing absolute prudence (DAP) to the multiperiod case, at least in spirit. • The result is the only 4th-order inequality result for unconstrained multiperiod random income and asset returns that I know of.

The 4th Derivative and Multiperiod Models • It is hard to get multiperiod results for higher order differential inequalities because multiperiod models leave more devilish ways to construct counterexamples. • Indeed, decreasing absolute prudence itself is not inherited from the utility function to the value function, as a counterexample in the paper shows. • And the result is not about inheritance of a property by a multiperiod value function at all.

What I want to prove (1): • In the 2-period model of “Precautionary Saving in the Small and in the Large,” at a given level of consumption, there is a reasonable property guaranteeing that the introduction of risk raises the marginal propensity to consume out of wealth, regardless of the shape of the income risk. • In the multiperiod model of this paper, at a given level of consumption, I want to find a reasonable property guaranteeing that the introduction of risk raises the marginal propensity to consume out of wealth, regardless of the stochastic process of income risk.

What I want to prove (2): • In a less well remembered result in “Precautionary Saving in the Small and in the Large,” the endogenous adjustment of the holdings of a risky asset lower the marginal propensity to consume out of wealth (at a given level of consumption) relative to no adjustment. • In the multiperiod model of this paper, I want to show that the endogenous adjustment of the holdings of risky assets lowers the marginal propensity to consume out of wealth (at a given level of consumption) for any joint stochastic process of labor income and asset returns.

Why to care (1) • The consumption stimulus from tax rebates depends on the effect of the permanent income hypothesis on the marginal propensity to consume. The only hope for the MPC being big is something like risk or liquidity constraints. And if it is liquidity constraints, you are better off working on the liquidity constraints directly (my recent National Lines of Credit Proposal in “Getting the Biggest Bang for the Buck in Fiscal Policy”)

Why to care (2) • -V’’(w)/V’(w) =c’(w) [-u’’(c(w))/u’(c(w)] • That is, the absolute risk aversion of the value function is equal to the absolute risk aversion of the underlying utility function at the relevant level of consumption times the marginal propensity to consume. • So, showing that c’(w) goes up is a key tool for showing that background risk crowds out (at least small) risks in a multiperiod model.

Proof Strategy • Show with complete asset markets and “strong DAP” that the introduction of risk raises the MPC at a given level of consumption. • Show that anything less than complete markets raises the MPC at a given level of consumption even more, all the way down to the case when there is only one asset, the safe asset. • Since before the introduction of risk, markets are ipso facto complete(as long as there is the one safe asset) that then proves that the introduction of risk raises the MPC at a given c.

Why Strong DAP Implies that the Introduction of Risks Raises the MPC at a given consumption under complete markets divide the 2nd by the 1st to get

Why Strong DAP Implies that the Introduction of Risks Raises the MPC at a given consumption under complete markets

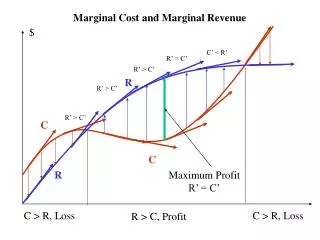

Intuition: Why more complete markets lead to a lower MPC and less complete markets lead to a higher MPC (1) • The le’Chatelier principle means that more margins of adjustment tent to make a maximized function less concave. • This applies to the value function, which is maximized over many future consumption levels and levels of asset holding.

Intuition: Why more complete markets lead to a lower MPC and less complete markets lead to a higher MPC (2) • The consumption-saving problem is like the basic consumer problem in intermediate micro where consumption is one good and saving to provide resources for the value function is another good. • The more margins of adjustment in the future, the slower the marginal value of saving declines

Intuition: Why more complete markets lead to a lower MPC and less complete markets lead to a higher MPC (3) • Start by equating the marginal utility of a dollar of consumption with the marginal value of saving a dollar. • Now consider an extra dollar, and equate the marginal utility of consumption to the marginal value of saving again. • The slower the marginal utility of consumption goes down, the more of the dollar goes to consumption and the less to saving (higher MPC). • The slower the marginal value of saving goes down, the more of the dollar goes to saving and the less to consumption (lower MPC). • So the ability to adjust asset holdings lowers the MPC. • An inability to adjust asset holdings (as in efficient markets where the holding is stuck at zero) raises the MPC.

Other fun things in the paper • My attempts to justify exotic 4th-order properties, back when I worried that people would resist them. • Lots of cool math, including matrix algebra for the proof about the effects of incomplete markets and stochastic calculus for a numerical example of what risk does to the MPC in an interesting case.

Story of my one paper with Louis • Chapter on the effect of background risk on optimal insurance: Eeckhoudt, L. and Kimball, M., 1992: “Background Risk, Prudence and Insurance Demand,” G. Dionne (ed.) Contributions to Insurance Economics, Kluwer Academic Press, 239–254. • What I learned from working on that paper with Louis helped me finally crack what was then my holy grail of figuring out how to do what I did in “Standard Risk Aversion.” So I owe that to Louis.