Download

1 / 8

80 likes | 342 Views

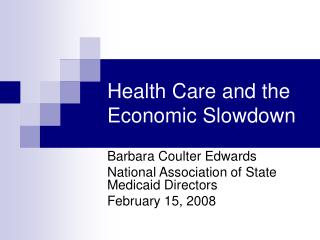

Economic Scenarios and Health Care. National Optometric Conference 5 November 2010 Roger Martin-Fagg. Chart 1.16 Broad money and nominal GDP.

E N D

Economic Scenarios and Health Care National Optometric Conference 5 November 2010 Roger Martin-Fagg

Chart 1.16 Broad money and nominal GDP (a) Recessions are defined as at least two consecutive quarters of falling output (at constant market prices) estimated using the latest data. Recessions are assumed to end once output began to rise. (b) The series is constructed using M4 growth prior to 1998 Q4, and growth in M4 excluding intermediate OFCs thereafter. For the definition of intermediate OFCs, see footnote (a) in Table 1.C. (c) At current market prices. The latest observation is 2009 Q4.

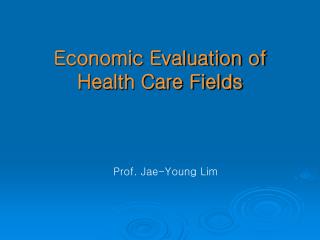

06 02 82 90 94 98 86 The UK Savings Ratio, source: NOS Latest data point 2nd Q 2010 Year on year 10pc 8pc 6pc 4pc 2pc 0pc -2pc -4pc 12 10 14 08

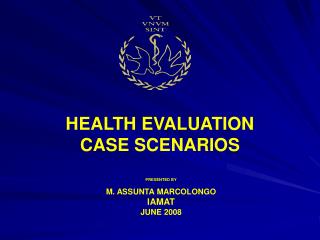

UK GDP 3rd Quarter 2010 Source: NOS Oct27 2010

5 4 3 2 1 0 -1 -2 -3 -4 -5 -6 -7 UK Real GDP The RMF View Percentages 2004Q4 2005Q4 2006Q4 2007Q4 2008Q4 2009Q3 2010Q1 2010Q3 2011Q1 2011Q3 2005Q2 2007Q2 2009Q2 2010Q2 2011Q2 2004Q2 2006Q2 2008Q2 2009Q4 2010Q4 2011Q4 4q 1q

Chart 2.7 Financial balances by sector (a) Recessions are defined as in Chart 2.5. (b) Includes non-profit institutions serving households. (c) Excludes public corporations.

Conclusions The Banking system in the West needs another three years to stabilise its balance sheets. The availability of Bank finance will continue to be limited. The USA will experience double-dip from November . Next year its GDP will shrink by 1% The UK will experience double-dip from March 2011, shrinking by 1% Europe will also contract next year, the south by more than the north, on average 1.5% Interest Rates: central bank rates, no change but market rates, will drift upwards. Inflation: this will not be a problem, deflation is more likely. Property prices in the West will fall by another 10%.

The Central Spending Review The NHS budget is not really protected. The internal rate of health care inflation is around 6%, the Treasury will allow a 1.15% yoy increase in real terms , but this uses their inflation figure of 2.25%. In effect the NHS will have to ‘find’ around 3.3Bn each year of cost saving over the next 4 years. This out of a total budget of £110 Bn. I would expect the NHS to look to their suppliers to increase the value they offer, with more for less. I would expect too, that internal processes could be made more cost effective. Expect at least 5 years of relative austerity.