Download

1 / 9

90 likes | 245 Views

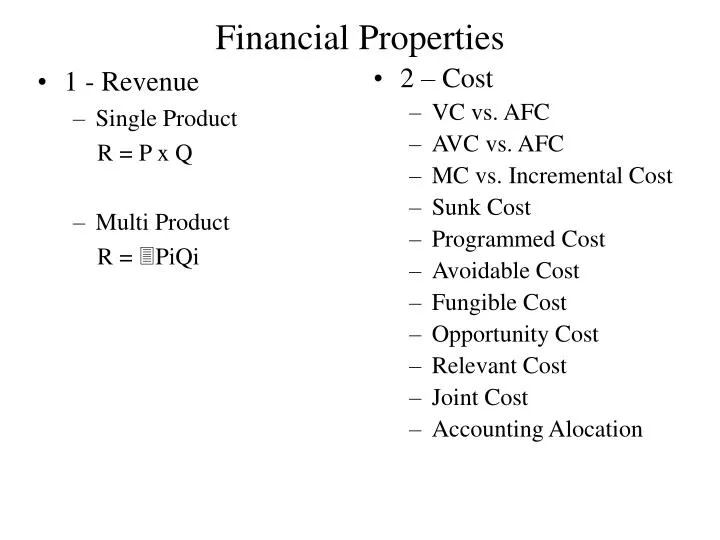

1 - Revenue Single Product R = P x Q Multi Product R = PiQi. 2 – Cost VC vs. AFC AVC vs. AFC MC vs. Incremental Cost Sunk Cost Programmed Cost Avoidable Cost Fungible Cost Opportunity Cost Relevant Cost Joint Cost Accounting Alocation. Financial Properties. 3 – Margins

E N D

1 - Revenue Single Product R = P x Q Multi Product R = PiQi 2 – Cost VC vs. AFC AVC vs. AFC MC vs. Incremental Cost Sunk Cost Programmed Cost Avoidable Cost Fungible Cost Opportunity Cost Relevant Cost Joint Cost Accounting Alocation Financial Properties

3 – Margins Gross Trade Net Profit A: Gross Margin (Profit) Total GM = R – CGS Unit GM = P – Unit CGS Four Factors Q P Cost Product Mix B: Trade Margin MfgrWholesalerRetailier For a Single Channel: Pm = P x (1-%Discount) Ex: Pc = $2.00 % Discount = 0.03 $1.40 = 2.00 x 0.70 Also Pc = Cost/(1-%Discount) For N Channels Pc = Cost/(1-%Discount) Cost = Pc(1-%Discount)

C: Net Profit Margins (before taxes) R -CGS_______ GPM -Other VC -FC_________ Net Profit Margin (NPM) % of NPM = NPM R 4 – Contribution Analysis BEQ = FC / (P-AVC) % CM = (P-AVC) / P BER = _FC = BEQ x P % CM Note BER = P x BEQ = P x FC / (P-AVC) Divide by PP x [FC / P – AVC]=FC P P %CM

Applications Sensitivity Analysis: Vary P or AVC or FC to determine BEQ Calculate Q to achieve Profit Objective () Qp = FC + P P – AVC Suppose objective is to achieve a profit of X% on sales R – C = % R PQ-AVC(Q)-FC = % PQ Q (P-AVC) – FC = % PQ Example: P=$25; AVC=$10; FC=$200,000; % = .20 Q(25-10) – 200,000 = .20 25Q Q = 20,000 5 – Cannibalization Assume: X X+ P 1.00 1.10 AVC .20.40 CM .80 .70 Qx = 1,000,000if X+ is not introduced; = 5,000,000 if X+ is introduced Qx+ = 1,000,000 if X+ is introduced Assume no incremental FC

Query: Should X+ be introduced? Solution: Method A X+Gain 1,000,000x.70 = 700,000 Cannibalization Loss 500,000 x .81 = 400,000 300,000 Method B Contr: w/o X+1,000,000x.80=800,000 Contribution with X and X+: X 500,000 x .80 = 400,000 X+ 1,000,000 x .70 = 700,000 Total Contr. Of X + X+= 1,100,000 Contr of X alone = 800,000 Net Gain from Add. of X+ =300,000 6 – Financial Concepts and Ratios A –Liquidity Working Capital = Current Assets – Current Liabilities Current Assets = Cash, Accounts Receivable, Inventory, Prepaid Expenses Current Liabilities = Accounts Payable, Income Taxes Operating Leverage = FC/VC Current Ratio = Assets Liabilities Quick Ratio =Assets-Inventory Liabilities

Asset Management • Inventory Turnover = Sales / Inventory • Asset Utilization = Sales / Total Assets • Profitability Ratios • Profit Margin in Sales = Profitability Before Taxes / Sales • Return on Assets = Profitability Before Taxes / Total Assets • Return on Investment = Net Income / Investment (Investment = Total Assets) Net Sales X Net Income Investment Net Sales • ROI = f (Stockturn, ratio of CGS to Net Sales)

Net Present Value Illustration Calculating Net Cash Flows GI = Sales – CGS = 1,000,000 – 700,000 = 300,000 Taxable Income = GI – Depreciation = 300,000-60,000 [(700,000 – 100,000) x .10] = 240,000 Net Income = Taxable Income – Tax = 240,000 – 120,000 (240,000 x .5) = 120,000 Net Cash Flow = Net Income + Depreciation = 120,000 + 60,000 = 180,000