Download

1 / 6

60 likes | 175 Views

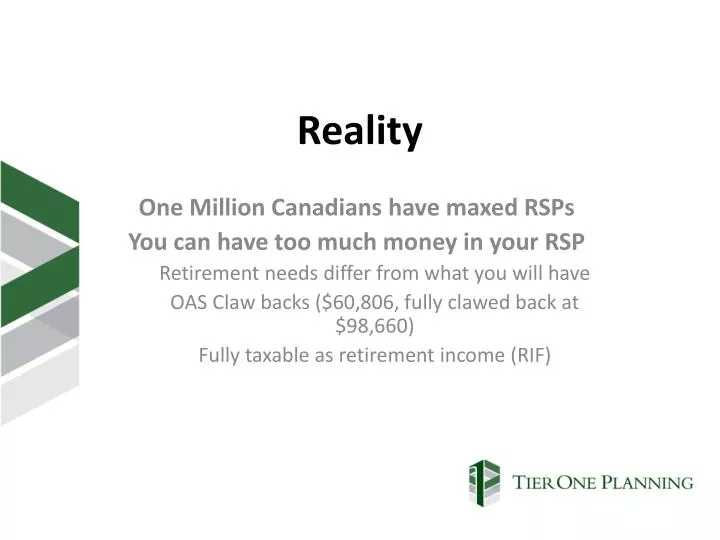

Reality. One Million Canadians have maxed RSPs You can have too much money in your RSP Retirement needs differ from what you will have OAS Claw backs ($60,806, fully clawed back at $98,660) Fully taxable as retirement income (RIF). The RSP Meltdown . Stop Contributing

E N D

Reality One Million Canadians have maxed RSPs You can have too much money in your RSP Retirement needs differ from what you will have OAS Claw backs ($60,806, fully clawed back at $98,660) Fully taxable as retirement income (RIF)

The RSP Meltdown Stop Contributing • RSP will be over funded • Desired Income will mean OAS claw backs Start Withdrawing • Determine over funded amount • What can be withdrawn per year to get to desired RSP amount? Use Withdrawals to pay for Investment Loan • Determine what size loan can be serviced with proceeds from RSP • Try to match Interest Exp with RSP withdrawal

Things to Consider Converting Registered into Non Registered • Slows down growth inside RSP • Non reg. not subject to minimums or maximums • Allows more control of income stream • Tax Advantaged • Potentially better tax treatment (Cap Gains/Div Income) • Complete Flexibility • Corporate Class is a perfect solution

Things to Consider Assuming leverage on accumulated funds • Leverage is NOT for everyone • Borrow less than investor can afford • Interest Only works best for this strategy • Be conservative with Investments • Make sure client has consistent, predictable cash flow • Benchmark for leverage – 30 - 50% of net worth

Things to Consider Tax Advantages • Interest Income – 100% inclusion • Cap Gains – 50% inclusion • Interest exp on loan tax deductible • Proceeds from RSP fully taxable • Tax deduction from interest wipes out tax obligation of RSP withdrawal

Summary • Great strategy when client has a lot of $$$ in RSP • Small RSP investor assuming big leverage doesn’t make sense • Client must understand risks of leveraging • Client must fit profile – steady cash flow • If loan is subject to margin calls client must have funds to cover it • Home Equity line of credit may work best • Borrow less than investor can afford • Can create significantly more after tax dollars for investor • A great idea to bring to clients – establish a planning relationship