Download

1 / 10

100 likes | 275 Views

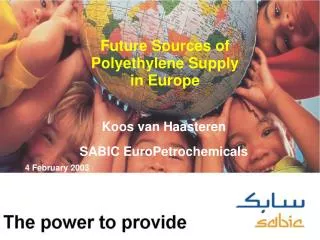

Future Sources of Polyethylene Supply in Europe. Koos van Haasteren SABIC EuroPetrochemicals 4 February 2003. SABIC EPC: positioned for leadership …. SABIC’s headquarters in Riyadh. SABIC’s Geleen site. SABIC … … is number 3 global PE player … markets almost 5 million tons of PE/PP

E N D

Future Sources of Polyethylene Supply in Europe Koos van Haasteren SABIC EuroPetrochemicals 4 February 2003

SABIC EPC: positioned for leadership … SABIC’s headquarters in Riyadh SABIC’s Geleen site SABIC … … is number 3 global PE player … markets almost 5 million tons of PE/PP … is now established in Europe … has technical centres in KSA, USA, India and The Netherlands … accelerates its expansion

Houston Yanbu … with the Power to Provide 4 highly integrated sites direct access to low cost feedstock world-scale facilities direct market access multiple lines per technology Gelsenkirchen Geleen Al Jubail Vadodara Riyadh Kerteh

Despite ME producers’ cash cost advantage over WE … ME producer NWE producer Typical ranges for gas and naphtha Structural delta in cash cost Low High Low High Gas price ($/mmBTU) Naphtha (EUR/t) Delta depends on oil price and co-product values

… WE capacity has outpaced demand, kton contributing to deterioration of margins … Margin as C4 LL -/- C2 (EUR/t) … and resulting in poor profitability; even for WE leaders!

Structure of typical projects are different Take into consideration: Cracker feedstock License cost Infrastructure Marketing and Sales cost Research and Development Other business cost Working capital … … LLDPE gasphase 350 kta HDPE slurry 300 kta Europe PP gasphase 2*200 kta Co-products extensionnaphtha cracker650 kta HDPE gasphase 350 kta LLDPE gasphase 2*350 kta Middle East Ethane cracker 1050 kta

ME re-investment level is lower than average WE level ME producer NWE producer Re-investment level required for IRR of 20% Delta in re-investment level Delta in cash cost Low High Low High Gas price ($/mmBTU) Naphtha (EUR/t) Within WE players differ in site scale and integration, portfolio, … Only strong WE super sites (cost leaders) remain

Pricing in Europe will be affected Re-investment level WE ME Middle East attracts investment at lower levels than Europe

Conclusions No rationale for investment in additional integrated ethylene and PE capacity in Europe • Potential for scrap and build • Little further improvement of cost position All cost laggards in Europe will disappear • Central and Eastern Europe have the same future as WE • European cost leaders will be able to compete Future PE source for West Europe • WE super sites • Growth will come from Middle East

Drivers for European industry: We enter a new era Period ’95 – ’02 • Scale and cost • Site integration and M&A • Technology and Catalyst Development Period ’02 – ’09 • Cost & Rationalisation • Bottomline cashflow Invest and grow scale cash flow Re-establishment of sustainable profit levels