Download

1 / 7

70 likes | 273 Views

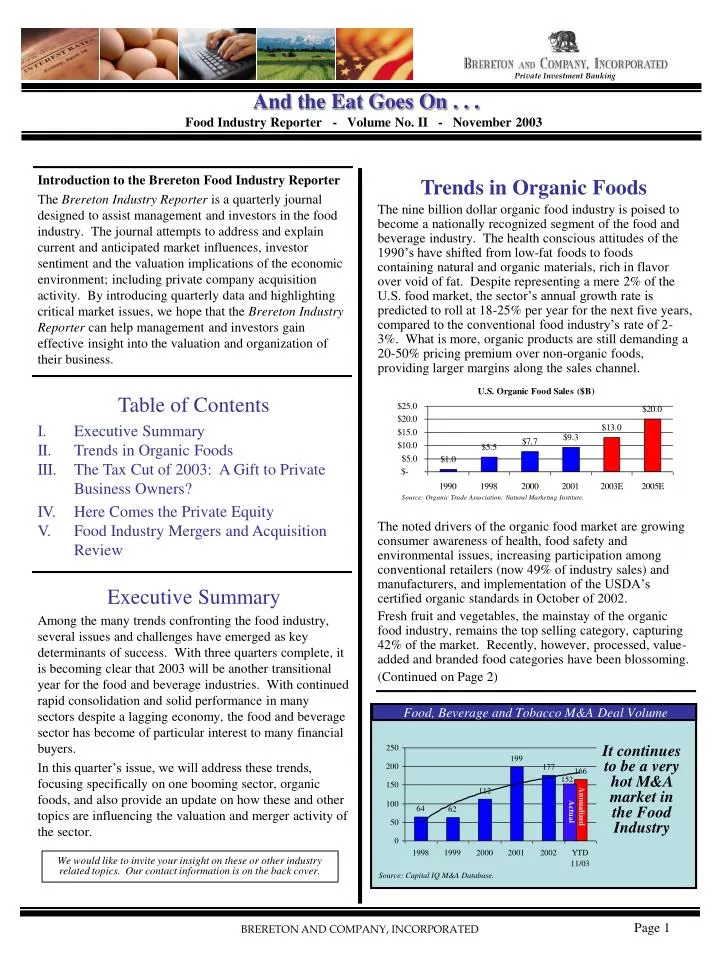

Private Investment Banking. And the Eat Goes On . . . Food Industry Reporter - Volume No. II - November 2003. Trends in Organic Foods

E N D

Private Investment Banking And the Eat Goes On . . .Food Industry Reporter - Volume No. II - November 2003 Trends in Organic Foods The nine billion dollar organic food industry is poised to become a nationally recognized segment of the food and beverage industry. The health conscious attitudes of the 1990’s have shifted from low-fat foods to foods containing natural and organic materials, rich in flavor over void of fat. Despite representing a mere 2% of the U.S. food market, the sector’s annual growth rate is predicted to roll at 18-25% per year for the next five years, compared to the conventional food industry’s rate of 2-3%. What is more, organic products are still demanding a 20-50% pricing premium over non-organic foods, providing larger margins along the sales channel. The noted drivers of the organic food market are growing consumer awareness of health, food safety and environmental issues, increasing participation among conventional retailers (now 49% of industry sales) and manufacturers, and implementation of the USDA’s certified organic standards in October of 2002. Fresh fruit and vegetables, the mainstay of the organic food industry, remains the top selling category, capturing 42% of the market. Recently, however, processed, value-added and branded food categories have been blossoming. (Continued on Page 2) Introduction to the Brereton Food Industry Reporter The Brereton Industry Reporter is a quarterly journal designed to assist management and investors in the food industry. The journal attempts to address and explain current and anticipated market influences, investor sentiment and the valuation implications of the economic environment; including private company acquisition activity. By introducing quarterly data and highlighting critical market issues, we hope that the Brereton Industry Reporter can help management and investors gain effective insight into the valuation and organization of their business. Table of Contents I. Executive SummaryII. Trends in Organic Foods III. The Tax Cut of 2003: A Gift to Private Business Owners? IV. Here Comes the Private EquityV. Food Industry Mergers and Acquisition Review Executive Summary Among the many trends confronting the food industry, several issues and challenges have emerged as key determinants of success. With three quarters complete, it is becoming clear that 2003 will be another transitional year for the food and beverage industries. With continued rapid consolidation and solid performance in many sectors despite a lagging economy, the food and beverage sector has become of particular interest to many financial buyers. In this quarter’s issue, we will address these trends, focusing specifically on one booming sector, organic foods, and also provide an update on how these and other topics are influencing the valuation and merger activity of the sector. Food, Beverage and Tobacco M&A Deal Volume It continues to be a very hot M&A market in the Food Industry 152 Annualized Actual We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. Source: Capital IQ M&A Database. BRERETON AND COMPANY, INCORPORATED

Private Investment Banking Trends in Organic Foods (Continued) M&A activity has accompanied growth in the natural and organic industry, at relatively high multiples. However, preserving the established equity, image and unique characteristics of newly acquired organic brands poses unique issues. Reflecting the fact that the national brands of large food conglomerates do not carry influential selling power with buyers of organic foods, some of the product’s packaging is void of the acquirers’ nationally recognized brands. The Tax Cut of 2003: A Gift to Private Business Owners? Basic Tenets of the New Tax BillNarrowly passed by the Senate, President Bush has called the tax cut "a vital action" that will stimulate the economy and create jobs. Just how big a cut is it? The new tax bill contains a 10-year, $350 billion tax cut, making it the third-largest tax cut in the nation's history. While there are many components of the Bill, ranging from marriage penalty reductions to child credit increases, business owners will likely be most affected by two provisions relating to the sale of their business: 1. The capital gains tax rate cut. 2. The rate cut on shareholder dividends. Among other provisions, the Bill temporarily reduces the rate on both corporate dividends and capital gains. The Bill lowers the rate on income from dividends and net long-term capital gains to just 15% for individuals. The new Bill marks the first time in at least the past 60 years that we can enjoy a capital gains tax rate below 20%. In addition, it is the first time that dividends are taxed at rates below income tax rates. But, these benefits are temporary. Both rates are subject to a sunset clause. The reduced rates are due to expire after 2008 and revert to current levels in 2009. The tax cuts could affect the private business owner on several levels. At a macro level, if the tax bill does its job, businesses and M&A could benefit from a boost in the economy. The tax changes also produce direct financial benefits when selling a business. We estimate that under the new capital gains tax rate, most business owners will see a 5%-8% increase in their after-tax proceeds following a sale. There is also the potential for tax savings from the change in the dividend income tax rate. Under the new bill, the rate is dropping from a maximum of 38.6% (personal income tax) to 15%, a 61% decline in the rate for eligible dividends. Private business owners looking to partially cash-out may be able to initiate a self-recapitalization so that the returns are treated as dividends and are taxed at the new, lower tax rate. Whether a company is structured as an S-Corp or a C-Corp and initiates a traditional recapitalization, a self recapitalization or an outright sale, the bottom line is that this tax bill creates new opportunities for the private business owner to partially or fully exit his company in a tax advantaged manner. (Continued on Page 3) Food Industry Reporter - Volume No. II - November 2003 We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. BRERETON AND COMPANY, INCORPORATED

Private Investment Banking The Tax Cut of 2003: A Gift to Private Business Owners? (Continued) Let’s examine the effect of the capital gains rate reduction on a business sale. The maximum capital gains tax rate will fall from 20% to 15%, resulting in greater after-tax proceeds following the sale of a business. The following example shows the effect of the new tax rate on a hypothetical business sale. In this example, the company sells for $8 million (on a debt-free basis). Because of the difference in tax structures between an S-Corp and a C-Corp, the capital gains tax reduction will have a varying degree of impact on individual companies. Let us assume that the two companies in our example are identical, with the exception that one was a C-Corp, and the other an S-Corp, from inception. Both companies were started with an initial investment of $100,000 and no additional outside capital was invested thereafter. Both companies have book equities of $2 million (with neither company using accelerated depreciation) and $2 million in debt. Because of their different tax structures, the taxable basis for the two companies is different. For the S-Corp, the basis in the company's stock is equal to the firm's equity, $2 million (the basis in the company's assets is $4 million). For the C-Corp, the basis in the company's stock is simply equal to the initial investment, $100,000 (the basis in the company's assets is $4 million). The following example shows the effect of the change in the capital gains tax rate on our hypothetical business sale, whether the company is structured as an S-Corp or as a C-Corp. In the above example, under the new tax rate, the net due owner to our S-Corp seller increases 3.9%. The net due owner gain for our C-Corp seller is even more dramatic, 6.2%. In other words, in this example, the new capital gains tax rate results in the seller keeping about an additional quarter of a million dollars when he sells his company. This tax bill, while encouraging, is not the final word on taxes. In the case of dividends and capital gains, the rate cuts are effective only through 2008. Whether or not the new rates will be extended beyond that date, or raised before that date, is anyone’s guess. Some believe the cuts will be made “permanent” beyond the sunset date. Others believe the rates will rise again, citing the narrow margin by which the Act passed, and considering that the Fed will soon be wrestling with a way to fully fund Social Security retirement and Medicare benefits for the baby boom generation. The new Bill marks the first time in at least the past 60 years that we have enjoyed a capital gains tax rate below 20%. In addition, it is the first time that dividends are taxed at rates below income tax rates. Because it can take anywhere from 6-18 months to sell a business (on average, one year), business owners thinking of selling should prepare for market now, so they can take advantage of what we believe to be a unique and probably impermanent opportunity. Food Industry Reporter - Volume No. II - November 2003 We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. BRERETON AND COMPANY, INCORPORATED

Private Investment Banking Merger and Acquisitions Review 2003 is proving to be a a challenging period for mergers and acquisitions (“M&A”) activity. A broad list of pressures including continued corporate scandals, continued volatility in the capital markets, concerns surrounding the strength of the economy and the uncertainty surrounding the war are several factors that have effectively depressed activity and pricing throughout the market. According to Thomson Financial Securities, the number of reported M&A transactions in all industries through 9/30/03 declined by 8.8% in 2003 vs. 2002 for middle market deals (deals < $250mm), while aggregate deal value decreased 12.8%, demonstrating a trend towards smaller acquisitions. In addition to the overall market, M&A activity has varied significantly by industry. M&A activity among food and beverage companies has proven to be significantly more resilient than the overall market. Although the food processing sector experienced a decline in deal activity for the last two years, declining 11% in 2002 and an estimated 6% in 2003, the overall market declined 20% and a projected 13% in 2002 and 2003 respectively. This drastic difference in M&A activity is due in large part to the continued stability of the food industry. Food and beverage companies continue to generate more acquisition interest than the market as a whole. What is more, the 2003 deal volume still represents the third highest level of deal volume recorded. (See chart on page 1) Factors Affecting Activity There are several factors that may assist in the resurgence of deal activity within the sector. Some of these factors include: Rebounding Credit Market The credit markets remain tight, but they appear to have bottomed out, as average total debt/EBITDA leverage ratios in transactions held at 3.7x year to date in 2003. Acquisition financing continues to be predominantly through asset-backed loans as a majority of the debt component, however recently lenders are showing increasing support for cash flow lending, which should help stimulate deal activity. (See chart on page 5) Increased Activity from Private Equity Groups As detailed in “Here Comes the Private Equity”, financial acquirers are aggressively looking for opportunities in the food and beverage sector. This should stimulate activity. Here Comes the Private Equity Private equity firms are proving to be particularly active buyers in today’s market. During the first half of 2003, they invested $33.2 billion in buyout capital, the highest first-half investment total ever recorded. Furthermore, these buyers are paying premium prices for strong companies, in part because of the competition for deals among private equity groups. Despite a decline in fundraising in 2002, analysts confirm that there is no shortage of capital in the hands of private equity groups, who still have an estimated $100 billion, raised during the golden fundraising years of 1998–2001, to invest. In fact, the abundance of uncommitted capital has become an issue for private equity firms, many of which are behind their forecast investment pace. As a result, they are scrambling to make investments in quality companies. Private Equity Groups are actively looking for attractive food and beverage companies with stable cash flows to invest in. This is exemplified by the recent barrage of deal activity. Additionally, the chart below illustrates, equity sponsored deals rebounded from 2001 reaching pre-2000 levels for both number of deal and aggregate deal value. Food Industry Reporter - Volume No. II - November 2003 Source: Capital IQ M&A Database, Mergerstat. We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. BRERETON AND COMPANY, INCORPORATED

Private Investment Banking Merger and Acquisitions Review (Continued) One of few growth alternatives for strategic acquirers As a result of the slow growth environment in the overall food and beverage market (U.S. food sales overall have increased approximately 2% per year for the last few years), large food and beverage companies are consummating strategic acquisitions to grow their top line. Such strategies are typically looking to acquire companies with differentiated products, unique brands or valued distribution. In general, while deal activity remains somewhat depressed in the overall market, the market remains attractive for quality food and beverage companies to pursue strategic alternatives. Given the level of interest from PEGs coupled with the continued pressure on large food companies to grow their top line value, valuations are rebounding and deal activity should continue to improve. Food Industry Reporter - Volume No. II - November 2003 Source: Portfolio Management Data and Fleet Capital Corp. Represents multiples of all LBOs less than $250 million. Source: Portfolio Management Data and Fleet Capital Corp. Source: CapitalIQ. We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. BRERETON AND COMPANY, INCORPORATED

Private Investment Banking Brereton and Company is a boutique investment bank dedicated to maximizing the value and liquidity of closely held businesses. Attention • Strategic and Financial advisors to businesses seeking value Maximization • Hands-on attention from experienced senior dealmakers who stay with your deal to closing • Founded in 1995 drawing from prior investment banking experience • Empathetic professionals who have acquired, operated and divested businesses for their own account • Broad industry experience in middle market Mergers & Acquisitions • Strategic planning framework for evaluation of financial alternatives • Structured timelines and processes for multiple bidder-based value maximization Expertise Process • If you are: • Undercapitalized and experiencing explosive demand for your product • Facing a difficult transition after many years at the helm • Unsure about how to best maximize the value of your business for your heirs • Ready to harvest your business investment to diversify your net worth • Please give us a call. Our initial discussions and analysis are strictly confidential and complimentary. Brereton and Company, Inc.1860 South Tenth StreetSan Jose, CA 95112www.brereton.net Brandt Brereton, Managing Director E-Mail: brereton@brereton.netTelephone: (408) 938-9255 Facsimile: (408) 938-9259 Member: International Network of Mergers and Acquisitions Partners (www.imap.com) BRERETON AND COMPANY, INCORPORATED

Private Investment Banking Brereton and Company, Inc.1860 South Tenth StreetSan Jose, CA 95112www.brereton.net • Food Industry ReporterAddition / Correction / Deletion Notice • Please Check All Appropriate Boxes • I would like to CONTINUE RECIEVING my complimentary Food Industry Reporter from Brereton and Company by: • E-Mail • Regular Mail • Please CORRECT my contact information on your distribution list • Please ADD my colleague’s name to your distribution list • Please REMOVE my name from your distribution list. Name Title Company Address City, State, Zip Phone Fax E-Mail Contact Information: E-Mail: info@brereton.netTelephone: (408) 938-9255 Facsimile: (408) 938-9259 Member: International Network of Mergers and Acquisitions Partners (www.imap.com) BRERETON AND COMPANY, INCORPORATED