Download

1 / 64

640 likes | 897 Views

Social Security. America’s largest social welfare program. Medicare and Medicaid combined are as large. Social Security is a self-financing program. It is financed by payroll taxes and has always collected more funds than it spends.

E N D

Social Security • America’s largest social welfare program. • Medicare and Medicaid combined are as large. • Social Security is a self-financing program. It is financed by payroll taxes and has always collected more funds than it spends. • Social Security has never run a deficit or contributed to the federal deficit. • A very large percentage of the population either collects Social Security or lives in a household with a recipient. • Almost half of all elderly American would live in poverty if they did not have SS.

Social Security • While Social Security is currently fiscally sound, it will have problems in the future. • The reason is that a growing percentage of our population is retiring and depending on SS. • In the not too distant future, SS will have to be amended to make it fiscally sound over the next 75 years. • This can be done and we will discuss ways to make the program viable in the future.

Social Security • How It Works and Some Ways to Make it Fiscally Sound For Another Seventy-Five Years

Overview • How Social Security Works • Financing Social Security • How Benefits Are Calculated and Paid • Financial Troubles • Various Ways to Fix The Problems

WHAT IS SOCIAL SECURITY AND HOW DOES IT WORK? • Social Security began in 1935, during the height of the Great Depression. The main motivation was to provide a means of support for the elderly. • Basic structure is that workers (and employers) pay a payroll tax, and the money is used to pay benefits to the current generation of elderly.

Two Programs • The Old Age & Survivors Insurance (OASI) • The Disability Insurance (DI) • Currently about 46 million Americans are receiving OASI and about 10 million are receiving DI. • The costs of both programs in 2011 was $716 billion—20% of all federal expenditures.

How Many People ReceiveSocial Security? • Currently about 56 million people receive benefits from the two programs each month. • 1 in 6 Americans get Social Security benefits. • Nearly 1 in 4 households receives income from Social Security.

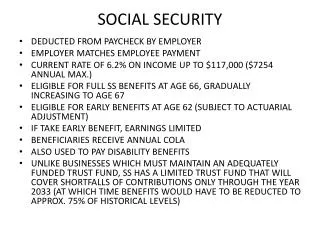

Financing Social Security • Workers and their employers pay with Social Security taxes • Workers pay • 6.2% of their earning up to $113,700 for Social Security, and • 1.45% of their earnings for Hospital Insurance under Medicare (Part A) • Employers pay an equal amount • The total is 12.4% for Social Security and 2.9% for HI (15.3%). • The Medicare tax rate increases by 0.9 for individuals earning $200,000 or more and for couples filing jointly who earn $250,00 or more. The employer does not match this extra tax.

Average Payment: January 2012 was $1230 • How much money would you currently need in Treasury notes (five-year obligations) to yield that amount each month?

Treasury notes currently pay less than 1% interest • You would need at least $1.5 Million • What percentage of retired people have that much investment money?

Retirement date • You can retire early, but it permanently lowers your benefits. • You can also retire later, and it permanently increases your benefits. • You can continue to work after retiring, but if you make very much money, some of your Social Security benefits will be taxed. • This creates a disincentive for some of the elderly to work.

Worker Benefits:Impact of Early or Late Retirement • Indexed for inflation • Actuarial decrease for early retirement • Example: average-wage worker, 62 in 2011 • Will get $1,380 per month at her full retirement age of 66 • or $1,007 per month at 62 • Actuarial increase for later retirement • 8 percent per year • Retirement Earnings Test • In 2013, retirees lose $1 of benefits for each $2 of earnings over $15,120.

How many people rely on Social Security for most of their income? • 90% of people 65 and older get Social Security • Nearly 2 in 3 (66%) get half or more of their income from Social Security • About 1 in 5 (22%) get all their income from Social Security

How Do you become eligible for Social Security? • Workers over 62 are eligible • If they have worked 10 years and paid payroll taxes during that time. • Benefits are based on a workers earnings history • Career average earnings are calculated as Average Indexed Monthly Earnings (AIME)

Two Calculations • Average Indexed Monthly Earnings (AIME) • Primary Insurance Amount (PIA)

Average Indexed Monthly Earnings (AIME) • Step One: Determine how much the worker earned every year through their working years • Step Two: Index those Earnings for Wage Inflation • Step Three: Pick the Highest 35 Years

Average Indexed Monthly Earnings (AIME), continued • Step Four: Add up those highest 35 years of earnings • Step Five: Divide by 35 • Step Six: Divide by 12 • Result is called Average Indexed Monthly Earnings (AIME) • AIME is then linked by formula to the basic retirement benefit • Result is called Primary Insurance Amount (PIA) • Paid at full retirement age

Primary Insurance Amount (PIA) 2013 • PIA = 90% of first $791 dollars • Plus 32% of the amount over $791 up to $4,768 • Plus 15% of anything over $4,768 • $791 and $4,768 are called bend points • Adjusted each year for inflation • Always pays higher benefits relative to earnings for lower paid.

Example: Average AIME of $6,000 • First Bend Point: 90% of $791 = $712 • Second Bend Point: 32% of $3,977 ($4,768-$791) = $1273 • Third Bend Point: 15% of earnings over $4,768 • ($6,000-$4,768) = $1,232 • 15% of $1,232 = $184 • Add the three: $712+$1,273+$184 = $2,119 in SS Benefits

How Benefits are calculated in a family Husband or wife gets 50% of worker’s Primary Insurance Amount (PIA) • Together, couple gets 150% Widow or widower gets 100% of worker’s PIA

Social Security Fiscal Health • Over the 70 years of SS’s existence, it has received income of about $14 trillion and paid out $11.5 trillion in benefits. • At the beginning of 2011 there was about $2.7 trillion in the OASI trust fund and $179 billion in the DI trust fund. • In 2011 Social Security earned $125 billion on its trust funds. • The trust fund is projected to reach $3.7 trillion by 2022 or 2023. • The Social Security surplus funds are used to buy United States Treasury bonds, ranging in maturities of 5 to 15 years. • These bonds are held by the Trust Fund until maturity.

Social Security Income NASI SS Brief #28

Why Is There a Problem? The Long-Run Decline • Since 2010 the surpluses added to the trust fund each year have started to shrink. • Without some changes, surpluses will continue to decline. • At some point, the trust fund will not grow and will start to shrink. • At some point the trust fund will be exhausted. • How long will this take? • That is the big question.

How Long Range Forecasting Answers the question: The Role of Actuaries

How actuaries estimate the future? • Review the past: birth rates, death rates, immigration, employment, wages, inflation, productivity, interest rates • Develop projections for the next 75 years • They develop three scenarios of how much Social Security will need to spend: Low cost; Intermediate (best estimate); High cost.

The bad News: Exhausting the Trust Fund • Currently actuaries project that by 2022 or 2023 benefits and expenses will exceed both payroll taxes and interest payments on the Trust Fund surplus. • At that point the program will have to start liquidating the Trust Fund • (When did Social Security’s problems begin?)

The Long-Range Forecast(Best estimate) • In 2033, the Trust Fund surplus is projected to be depleted. • It is projected that payroll taxes will cover only 75% of expenses and benefits from 2033 to 2085. • In other words, it will run big deficits. • If current payouts are to be maintained, benefits will have to be reduced, payroll taxes increased, retirement delayed or some other method will have to be employed.

Why will Social Security cost more in the future? The number of Americans over age 67 will grow faster than the number of workers. • Boomers are reaching age 67 • People are living longer after age 67 (average about 20 years) • Birth rates are projected to remain stable in the future. • People 67 and older will increase from 13% to 19% of all Americans